SSAP 97, Investments in Subsidiary, Controlled, and Affiliated Entities, addresses the accounting for SCAs. SCAs are reported using an equity method based on the reporting entity’s shares of the audited statutory equity of the SCAs financial statements (for insurance SCA entities), audited GAAP equity, or audited GAAP equity with specified adjustments depending on the type of SCA entity. The change in the carrying value between reporting periods must be recorded as an unrealized gain/loss through surplus.

The "equity pick up" of surplus of an insurance company investee is not necessarily the entire "capital and surplus" balance. Per SSAP 97, the carrying value of an insurance company after initial acquisition is the original acquisition cost adjusted for the insurer's share of changes in unassigned funds, "special surplus funds," and "other than special surplus funds." Surplus notes are excluded from the carrying value of the subsidiary in the parent company financial statements. When surplus notes are issued by a subsidiary and held by the parent insurer, these investments are accounted for by the parent as Schedule BA assets. When the surplus notes are issued to an entity other than the parent, the parent insurer cannot record any value for the surplus notes because it is not capital from the parent company's perspective (i.e., it is akin to a minority interest). In 2018, the NAIC issued guidance relating to the reverse situation (i.e., SCA entities owning surplus notes issued by the parent). SSAP 97 and SSAP 41 were amended to clarify that surplus notes should be eliminated in the parent insurer’s surplus if the SCA acquires any portion of outstanding surplus notes issued by the parent.

Another adjustment to the equity pickup is for non-controlling interests for entities valued using US GAAP equity. The component of GAAP equity that represents non-controlling interests should be excluded from the insurer's investment as it is not part of the insurer's "share of the audited GAAP basis" (paragraph 11 of SSAP 97).

The carrying value of certain SCAs (SSAP 97 paragraphs 8.b.ii and 8.b.iv entities) is adjusted audited GAAP equity. The required adjustments are listed in SSAP 97 paragraphs 9.a through SSAP 97 paragraph 9.g. Note that the adjustments for goodwill and deferred tax assets (SSAP 97 paragraphs 9.d and 9.e) are based on 10% of equity of the investee, not the parent insurance company investor. The schedule to adjust from audited US GAAP to adjusted audited GAAP is not included in the audited financial statements. The insurer prepares the schedule in connection with the preparation of the parent entity financial statements, as the adjusted equity represents the parent insurance company's carrying value in its SCA investment.

When an insurance company directly acquires another insurance company in a transaction that results in statutory goodwill (the difference between the historical statutory book value of the acquired entity and the purchase price), the goodwill is part of the carrying value of the acquired entity on the insurance company's balance sheet as an investment in common stock. Therefore, for investments in acquired insurance companies, there will be a difference between total capital and surplus per the investee's annual statement and audited statutory financial statements and the carrying value in the insurance company parent's financial statements, unless the purchase price for the acquired entity equaled its statutory book value at the acquisition date. The goodwill is limited to 10% of capital and surplus (adjusted to exclude admitted net positive goodwill, EDP equipment, and operating system software), and is amortized by the insurance company parent to unrealized gain/loss on investments. Also, note that goodwill cannot be pushed down to the books of the acquired insurance entity. In addition, when an acquired entity is subsequently merged into another entity, the goodwill is required to be written off immediately to surplus per SSAP 68, paragraph 13.

In 2018, the NAIC adopted a revision to SSAP 68 to clarify that “cancelling equity of an owned entity, without issuance of new equity, and incorporating the assets and liabilities of the owned entity directly within the reporting entity’s financial statements (e.g., dissolving the SCA entity and absorbing their assets and liabilities)” also qualifies as a statutory merger.

The carrying value of an investee can be less than $0 in two circumstances. Per SSAP 97 paragraph 13.e, the insurance company should provide for its share of losses after reducing its investment balance to $0 when the insurer has guaranteed obligations of the investee or is otherwise committed to provide further financial support. In addition, noninsurance entities valued in accordance with SSAP 97 paragraph 8.b.ii that hold only nonadmitted assets would also be valued at negative equity by the parent insurer if the value of the nonadmitted assets exceeds total equity. The other adjustments required to US GAAP for SSAP 97 paragraph 8.b.ii entities that are listed in SSAP paragraph 9 could also result in negative equity. This guidance is consistent with Question 7 in the SSAP 97 Implementation Q&A. An insurer is not permitted to forgo an audit and record a nonadmitted asset (i.e., with zero value) to avoid this treatment.

All basis differences between cost/purchase price and the underlying GAAP equity should be amortized, similar to goodwill. This includes minority owned (less than 10%) SSAP 48 entities that are not scoped into SSAP 97. SAP also requires the basis differences to be included with goodwill for purposes of determining the 10% goodwill limitation.

Insurance companies that purchase other insurance entities, either directly or through a non-insurance downstream holding company, are required to include any goodwill related to the purchase in their goodwill limitation calculation. In 2019, the NAIC clarified that goodwill resulting from the application of pushdown accounting by an insurer to a non-insurance SCA is required to be included in the 10% goodwill limitation calculation. However, when insurance companies own non-insurance entities valued using US GAAP equity and those non-insurance entities acquire other non-insurance companies, the insurance entity parent companies are not required to include the goodwill in their goodwill limitation calculation if the goodwill is pushed down to the acquired downstream GAAP entity. However, pushdown is not required if a downstream non-insurance holding company owned by the insurer purchases the non-insurance GAAP entity. The NAIC continues to review the accounting for goodwill held in various holding company structures, and additional discussion and guidance is expected in 2021, which could change this guidance.

Insurance entities are required to disclose a detail listing of directly owned SSAP 97 SCA entities. However, this excludes insurance SCA’s and all SSAP 48 entities, including those that are affiliates of the insurer (which is generally ownership of 10% or more of the SSAP 48 entity).

In practice, questions have arisen in terms of how a company or filer treats the goodwill from the acquisition of a holding company that owns insurance and non- insurance companies that were purchased by a downstream holding company subsidiary of an insurance company. There are two acceptable approaches for viewing this transaction under SSAP 97, both of which result in the same answer. One approach would be for the filer to account for the investment in an SCA, and that investment must include goodwill, whether it has been pushed down or not. Therefore, when the filer applies the provisions of SSAP 97, the downstream insurance company acquired will be valued at its statutory carrying amount, which would include goodwill (including applying the goodwill limitations).

The alternative approach is that the goodwill is pushed down to the SCA and, therefore, the filer must value the insurance company acquired, including goodwill at its statutory carrying amount, or the goodwill is at the holding company. If the filer believes that the goodwill is at the holding company, the filer must apply the provisions of SSAP 97 paragraph 21.e, which would require the other assets of the holding company to be accounted for in accordance with statutory accounting principles and, again, the goodwill limitations must be applied. The NAIC is discussing and expected to issue guidance in 2021 on goodwill in holding company structures, which could result in revisions to this guidance.

Example IG 13-1 and Example IG 13-2 illustrate the goodwill admissibility guidance under SSAP 97.

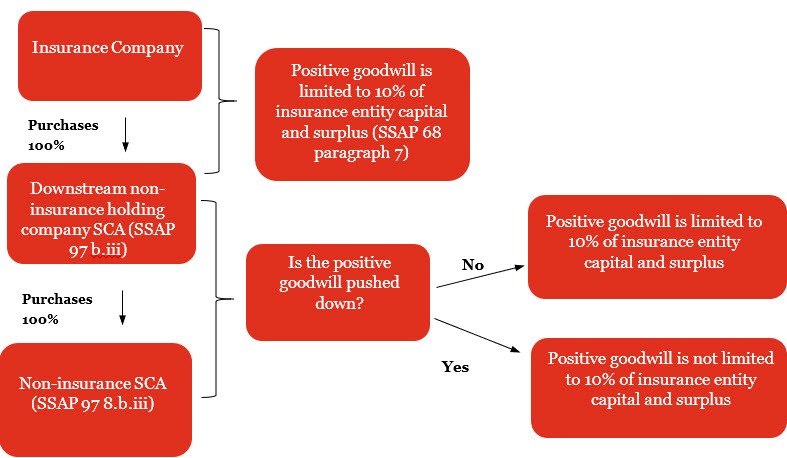

EXAMPLE IG 13-1

SSAP 97 goodwill admissibility – purchase of an SCA accounted for under SSAP 97 paragraph 8.b.iii

Insurance Company purchases a downstream non-insurance holding company SCA accounted for under SSAP 97 paragraph 8.b.iii. Subsequently the non-insurance holding company purchases a non-insurance SCA accounted for under SSAP 97 paragraph 8.b.iii.

How would goodwill be accounted for in both acquisitions?

Analysis

As depicted below, the goodwill from the acquisition of the non-insurance downstream holding company SCA accounted for under SSAP 97 paragraph 8.b.iii is limited to 10% of the insurance reporting entity's capital and surplus whether the goodwill is pushed down or not. However, when the non-insurance downstream holding company purchases a non-insurance SCA accounted for under SSAP 97 paragraph 8.b.iii, the goodwill is limited to 10% of Insurance Company’s capital and surplus only when it is not pushed down to the lower-tier non-insurance SCA. This is because SCAs accounted for under paragraph 8.b.iii are valued at audited GAAP equity without adjustment.

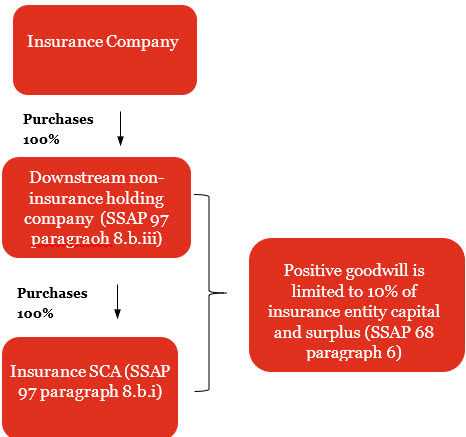

EXAMPLE IG 13-2

SSAP goodwill admissibility guidance - purchase of an SCA accounted for under SSAP 97 paragraph 8.b.i

Insurance Company purchases a downstream non-insurance holding company SCA accounted for under SSAP 97 paragraph 8.b.iii that subsequently purchases a US insurance SCA accounted for under paragraph 8.b.i.

How would goodwill be accounted for in the purchase of the US insurance SCA?

Analysis

As depicted below, since Insurance Company purchased a US insurance SCA under paragraph 8.b.i (either directly or indirectly through a downstream holding company), goodwill is limited to 10% of the insurance reporting entity’s capital and surplus. Pushdown of goodwill is not permitted for US insurance SCAs.