SSAP 25 provides guidance related to affiliated and related party transactions.

The key concepts to consider when assessing related party transactions include the following:

- Determining whether the transaction is economic or non-economic. An economic transaction is defined as an arms-length transaction that results in the transfer of risks and rewards of ownership. In some cases, a transaction may be economic to one party and non-economic to the other.

- When related-party transactions result in a “mere inflation of surplus” at a parent insurance company level, any gain or loss resulting from the transaction must be deferred by recording a deferred gain and an unrealized loss.

Example IG 13-3 and Example IG 13-4 illustrate common related-party transactions.

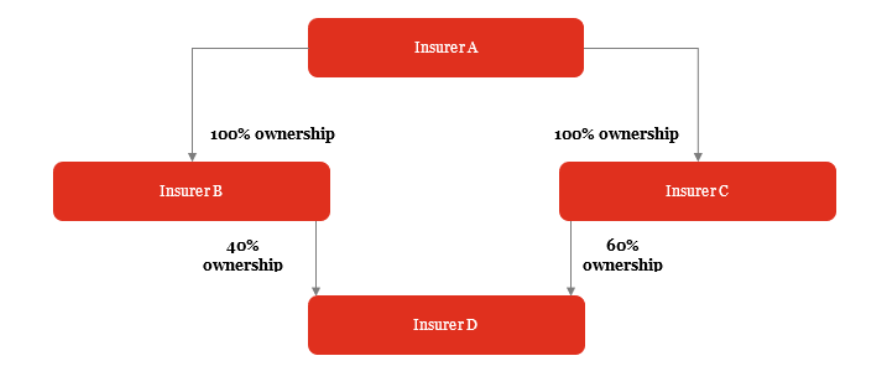

EXAMPLE IG 13-3

Intercompany sale of assets

Insurer A owns 100% each of Insurer B and Insurer C. Insurer C owns 60% of Insurer D, while Insurer B owns the remaining 40%.

Insurer D sells Insurer B a bond in a $100 million unrealized gain position. Is the transaction economic to Insurer B and Insurer D?

Analysis

The transaction is economic to Insurer D, but not to Insurer B.

Insurer D has transferred the risks and rewards to Insurer B and may therefore record the realized gain on sale; however, Insurer B now owns directly what it previously owned indirectly through its SSAP 97 investment in Insurer D (40% of the bond in addition to purchasing the other 60% it had not previously indirectly owned). If Insurer D is a life, health, or fraternal insurer, it will need to record IMR or AVR on the realized gain on a bond (depending on whether the gain is interest or credit related).

Insurer B should defer $40 million of the gain recognized on the sale by Insurer D as it is related to the portion previously indirectly owned by Insurer B, and therefore would lead to a mere inflation of surplus in Insurer B. Although Insurer A is the ultimate parent company, no separate deferral of this portion of the gain would be required by Insurer A, as the deferral would be recognized through its recognition of the equity earnings of Insurer B.

Insurer A should, however, separately defer the remaining $60 million gain. While Insurer C owns 60% of Insurer D, it was not a party to the transaction, and the affiliate that Insurer D transacted with (Insurer B) is not owned by C. The obligation to defer the remaining $60 million occurs at the common parent level, which is Insurer A.

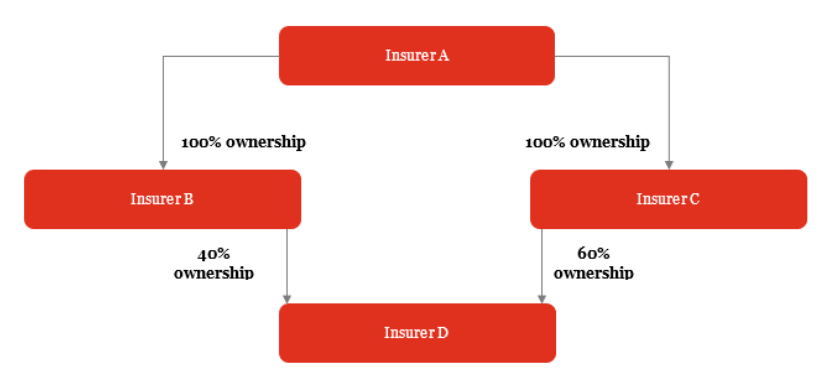

EXAMPLE IG 13-4

Capital contribution from parent to subsidiary

Insurer A owns 100% each of Insurer B and Insurer C. Insurer C owns 60% of Insurer D, while Insurer B owns the remaining 40%.

Insurer A contributes capital in the form of appreciated bonds to Insurer C, with an amortized cost of $70 million and a fair value of $100 million. Is the transaction economic to Insurer A and Insurer C?

Analysis

This transaction is economic to Insurer C, and therefore, Insurer C would recognize the capital contribution at the fair value of $100 million. However, the transaction is non-economic to Insurer A because it still owns the bonds indirectly through its investment in Insurer C.

Therefore, the sale of bonds would be recorded at $70 million in Insurer A’s financial statements, representing the lower of cost or fair value.

When recording its equity earnings in Insurer C, Insurer A would reduce the carrying value of its investment in Insurer C by $30 million, representing the amount that the fair value exceeded the cost of the transferred assets. This results in a transaction that is surplus neutral in Insurer A’s financial statements.