Search within this section

Select a section below and enter your search term, or to search all click Insurance Contracts

Favorited Content

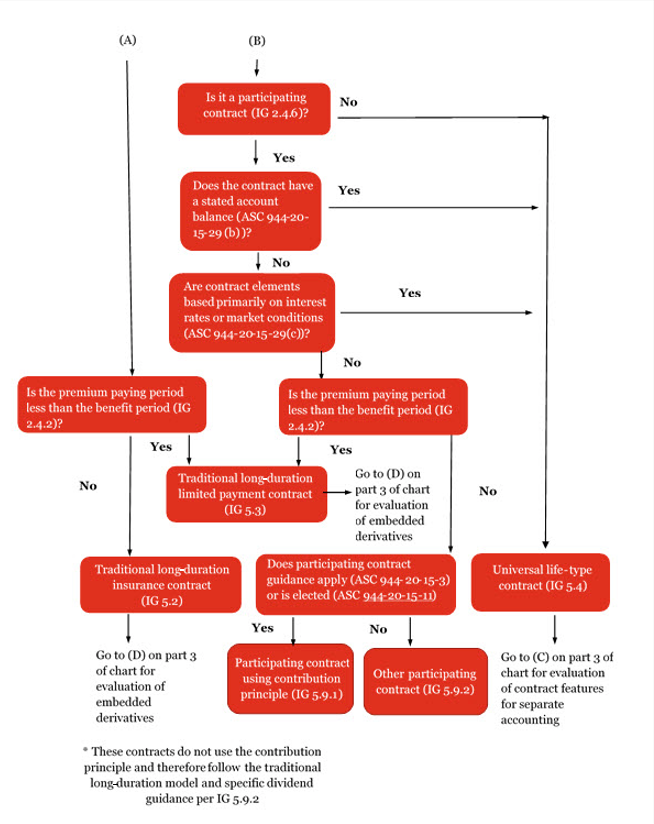

For purposes of the scope application of the Long-Duration Subsections of this Subtopic, universal life-type contracts include contracts that provide either death or annuity benefits and are characterized by any of the following features:

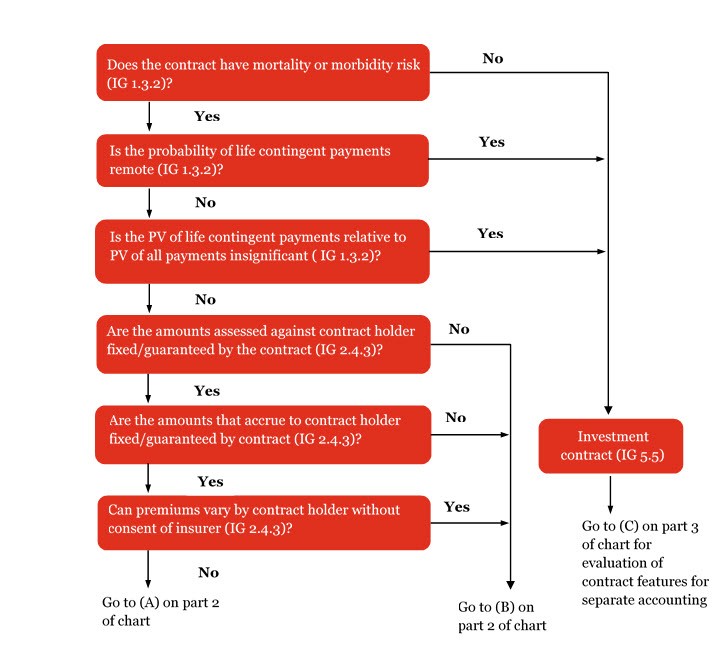

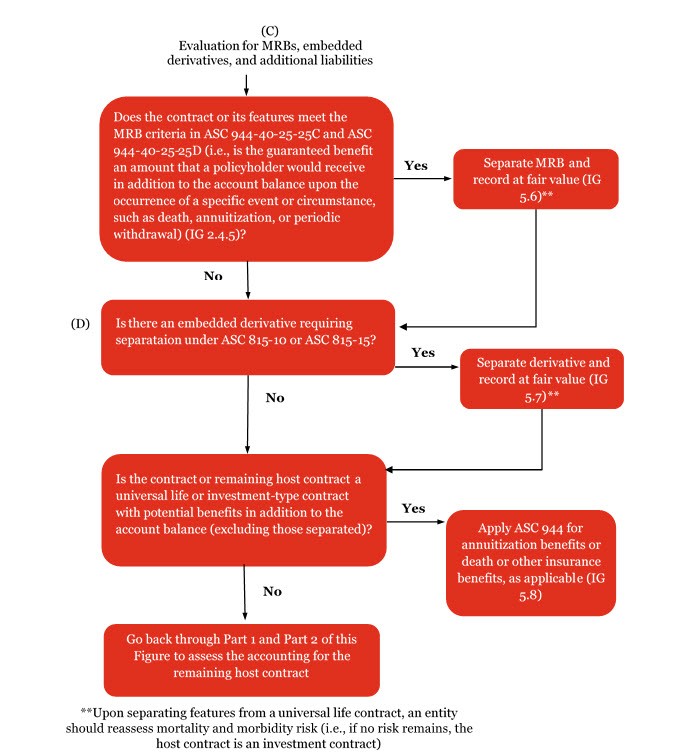

A contract or contract feature that both provides protection to the contract holder from other-than-nominal capital market risk and exposes the insurance entity to other-than-nominal capital market risk shall be recognized as a market risk benefit.

In evaluating whether a contract or contract feature meets the conditions in paragraph 944-40-25-25C, an insurance entity should consider that:

Base product |

Benefit feature |

Benefit feature previous accounting model |

Market risk benefit under ASC 944-40-25-25C and 25D? (if no, follow previous accounting model) |

|---|---|---|---|

Annuity contracts

|

|||

Fixed annuity

|

Interest crediting rate on the account balance at the discretion of the insurance entity that is often indirectly based on return on unspecified general account assets with a contractually-specified guaranteed minimum interest crediting rate

|

No. The interest crediting feature is not providing a potential benefit in addition to the account balance.

|

|

Fixed annuity-market value adjusted annuity

|

The contract provides for a return of principal plus a fixed rate of return if held to maturity, or alternatively, a market-adjusted value if the surrender option is exercised by the contract holder before maturity. The market-adjusted value is typically based on current interest crediting rates being offered for new market value annuity purchases.

|

No. The surrender feature is not providing a potential benefit in addition to the account balance. Amount received upon surrender is account balance adjusted for interest rate changes; contract holder is in effect absorbing capital market risk rather than being protected from it.

|

|

Fixed-indexed annuity (FIA)/ Equity-indexed annuity (EIA)

|

Interest crediting rate on the account balance is based on performance of an equity index (e.g., S&P 500) with a contractually-specified minimum interest crediting rate

|

The equity index crediting is part of the account balance and is an embedded derivative.

|

|

Variable-indexed annuity

|

Interest crediting rate on the account balance based on performance of an equity index (e.g., S&P 500). Interest crediting rate may be negative and may have a "buffer" in which the insurance entity absorbs certain downside risk (e.g., first 10% loss) with remaining risk with contract holder.

|

The equity index crediting is part of the account balance and is an embedded derivative.

|

|

Fixed-indexed annuity (FIA)/ Equity-indexed annuity (EIA)/ Variable-indexed annuity

|

GMXBs (i.e., GMDB, GMIB, GMAB, GMWB, GMWB for life)

|

ASC 944-40-25-25B, ASC 944-40-25-26 to ASC 944-40-25-27A or ASC 815-15 (varies based on specific feature)

|

Yes. These guarantee features are providing a potential benefit in addition to the account balance for difference between the guaranteed benefit and the account balance.

|

Deferred fixed annuity

|

Annuitization guarantee provides calculation of annuitization periodic payments based on guaranteed minimum interest rate as described in ASC 815-15-55-58.

|

Yes, if the risk is other-than-nominal at inception; expected utilization is not considered when making the assessment. The guarantee feature is providing a potential benefit in addition to the account balance for the difference between the guaranteed benefit (i.e., periodic payments promised by the annuitization guarantee) and the periodic payments using current interest rates.

|

|

Deferred variable annuity

|

Interest crediting rate on the account balance is equal to investment returns from designated investment funds.

|

No. The interest crediting feature is not providing a potential benefit in addition to the account balance.

|

|

Deferred variable annuity with GMXBs, reinsurance of GMXB features

|

GMXBs (i.e., GMDB, GMIB, GMAB, GMWB, GMWB for life)

|

ASC 944-40-25-25B, ASC 944-40-25-26 to ASC 944-40-25-27A or ASC 815-15 (varies based on specific feature)

|

Yes. These guarantee features are providing protection to the contract holder (or cedant) for the difference between the guaranteed benefit and the account balance.

|

Life insurance products

|

|||

Universal life

|

Interest crediting rate on the account balance at the discretion of the insurance entity, often indirectly based on return on unspecified general account assets. Contract may or may not provide guaranteed minimum interest crediting rate.

|

No. The interest crediting feature is not providing a potential benefit in addition to the account balance.

|

|

Universal life

|

A no lapse guarantee/universal life secondary guarantee, where the death benefit remains in force even if the account balance is insufficient to pay the cost of insurance assuming minimum funding requirements are met.

|

No. The death benefit component of a life insurance product is excluded from the scope of the MRB guidance.

|

|

Universal life

|

Interest crediting rate on the account balance is based on performance of an equity index (e.g., S&P 500).

|

It depends on the termination provisions of the contract. If the equity index crediting earned to date is available upon surrender at any time, the equity index crediting is part of the account balance and is an embedded derivative.

|

|

Universal life

|

Death benefit is based on the performance of an equity index.

|

No. The death benefit component of a life insurance product is excluded from the scope of the MRB guidance.

|

|

Universal life

|

An option to settle the contract upon surrender or death with an annuity determined using guaranteed fixed interest rates.

|

Yes. The annuitization option is providing protection for the difference between the guaranteed benefit and the account balance.

|

|

Variable universal life

|

Interest crediting rate on the account balance is equal to investment returns from designated investment funds.

Upon death, in one version of the product, the policyholder receives the greater of account balance and fixed death benefit; in another version, the policyholder receives the account balance plus the fixed death benefit.

|

No. The interest crediting component does not provide a potential benefit in addition to the account balance.

No. The death benefit component of a life insurance product is excluded from the scope of the MRB guidance.

|

|

Variable universal life

|

Benefits other than death benefits, for example, a GMAB or GMWB on the account balance component

|

ASC 944-40-25-25B, ASC 944-40-25-26 to ASC 944-40-25-27A or ASC 815-15 (varies based on specific feature)

|

Yes. The benefit is providing protection for the difference between the guaranteed benefit and the account balance.

|

Participating life insurance contracts denote those that have both of the following characteristics:

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Insurance Contracts