Search within this section

Select a section below and enter your search term, or to search all click Insurance Contracts

Favorited Content

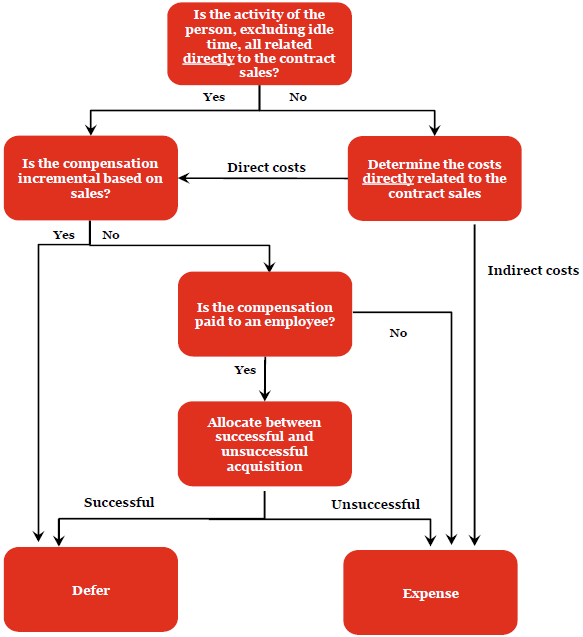

An insurance entity shall capitalize only the following as acquisition costs related directly to the successful acquisition of new or renewal insurance contracts:

The costs of direct-response advertising shall be capitalized if both of the following conditions are met:

Payroll-related fringe benefits include any costs incurred for employees as part of the total compensation and benefits program. Examples of such benefits include all of the following:

The portion of the total compensation of executive employees that relates directly to the time spent approving successful contracts may be deferred as acquisition costs. For example, the amount of compensation allocable to time spent on policies actually issued after approval by a contract approval committee is a component of acquisition costs.

Variable compensation

|

$200,000

|

|

Fixed compensation

|

$50,000

|

|

Total compensation

|

$250,000

|

The successful-efforts accounting notion utilized at an entity-wide level may result in a standard costing system that does not accurately reflect the amount of costs that may be deferred and amortized under this Subtopic. Successful acquisition efforts can be determined as a percentage of each function (for example, application, underwriting, and medical and inspection) and may be based on the percentage, adjusted for idle time and time spent on activities for which the related costs cannot be deferred, of successful and unsuccessful efforts determined for each function.

Examples of other costs related directly to the insurer’s acquisition activities in paragraph 944-30-25-1A(b) that would not have been incurred by the insurance entity had the acquisition contract transaction(s) not occurred include all of the following:

Advertising is the promotion of an industry, an entity, a brand, a product name, or specific products or services so as to create or stimulate a positive entity image or to create or stimulate a desire to buy the entity's products or services. Advertising generally uses a form of media—such as mail, television, radio, telephone, facsimile machine, newspaper, magazine, coupon, or billboard—to communicate with potential customers.

Excerpt from ASC 944-30-25-1D

The probable future benefits of direct-response advertising activities are probable future revenues arising from that advertising in excess of future costs to be incurred in realizing those revenues.

Time attributed to successful contract acquisition efforts |

Fixed salary |

|

|---|---|---|

Agent 1

|

55%

|

$100,000

|

Agent 2

|

85%

|

$100,000

|

Agent 3

|

75%

|

$100,000

|

Agent 1 |

Agent 2 |

Agent 3 |

|

|---|---|---|---|

Fixed salary

|

$100,000

|

$100,000

|

$100,000

|

Time attributed to successful efforts

|

55%

|

85%

|

75%

|

Compensation cost attributable to successful efforts (deferrable)

|

$55,000

|

$85,000

|

$75,000

|

Time attributed to successful contract acquisition efforts |

Fixed salary |

Variable commission amount |

|

|---|---|---|---|

Agent 1

|

55%

|

$100,000

|

$80,000

|

Agent 2

|

85%

|

$100,000

|

$150,000

|

Agent 3

|

75%

|

$100,000

|

$120,000

|

Agent 1 |

Agent 2 |

Agent 3 |

|

|---|---|---|---|

Fixed salary (1)

|

$100,000

|

$100,000

|

$100,000

|

Time attributed to successful efforts

|

55%

|

85%

|

75%

|

Fixed compensation cost attributable to successful efforts (2)

|

$55,000

|

$85,000

|

$75,000

|

Variable commission (25% of premiums)

|

$80,000

|

$150,000

|

$120,000

|

Incremental direct compensation - amount of variable commission in excess of fixed salary (3)

|

N/A

|

$50,000

|

$20,000

|

Deferrable compensation costs [(2)+(3)]

|

$55,000

|

$135,000

|

$95,000

|

All other contract acquisition-related costs, including costs related to activities performed by the insurer for soliciting potential customers (except direct-response advertising capitalized in accordance with paragraph 944-30-25-1AA), market research, training, and administration, should be charged to expense as incurred. Employees’ compensation and fringe benefits related to those activities, unsuccessful contract acquisition efforts, and idle time should be charged to expense as incurred. Administrative costs, rent, depreciation, and all other occupancy and equipment costs are considered indirect costs and should be charged to expense as incurred.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Insurance Contracts