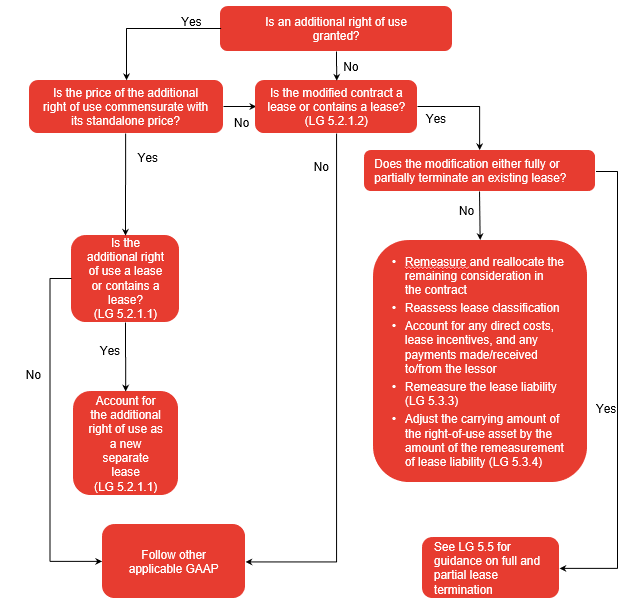

ASC 842-10-25-8 provides guidance on whether a lessee should account for a lease modification as a new contract (separate from the existing contract).

ASC 842-10-25-8

An entity shall account for a modification to a contract as a separate contract (that is, separate from the original contract) when both of the following conditions are present:

a. The modification grants the lessee an additional right of use not included in the original lease (for example, the right to use an additional asset).

b. The lease payments increase commensurate with the standalone price for the additional right of use, adjusted for the circumstances of the particular contract. For example, the standalone price for the lease of one floor of an office building in which the lessee already leases other floors in that building may be different from the standalone price of a similar floor in a different office building, because it was not necessary for a lessor to incur costs that it would have incurred for a new lessee.

An additional right of use is granted when the lease contract is modified to give the lessee a right to use an additional underlying asset that was not included in the original lease. For example, when the floor space under lease is increased or a lessee receives the right to use a new standalone asset. A modification to increase the lease term is not considered an additional right of use.

Accounting for the separate new contract

When a lessee concludes that a lease modification should be accounted for as a new contract that is separate and apart from the original lease, the new contract should be evaluated for whether it is a lease or contains an embedded lease (see

LG 2.3 for the definition of a lease). If the new contract is a lease or contains an embedded lease, the new lease should be accounted for as any other new lease (classified as finance or operating and measured accordingly). See

LG 3 for information on lease classification and

LG 4 for information on lease measurement.

The new lease is recorded on the commencement date of the new lease, which is the date the lessee has access to the leased asset. For example, if a lessee modifies a lease to use additional space in a building, the new lease should be recorded once that space is available for use. See

LG 3.2.1 for information on lease commencement.

Example LG 5-1 illustrates a lessee’s accounting for a modification as a separate new lease.

EXAMPLE LG 5-1

Modification that is a separate new lease

Lessee Corp enters into a 5-year lease for 2,000 square feet of warehouse space with Lessor Corp for $10,000 per month.

At the end of year one, Lessee Corp and Lessor Corp agree to amend their lease contract to include an additional 1,000 square feet of warehouse space in the same building for the remaining four years of the lease. Lessee Corp will pay an additional $6,000 per month for the additional space. The additional $6,000 is in line with the current market rate to lease 1,000 square feet of warehouse space in that particular building at the date that the modification is agreed to. Lessee Corp will make one monthly payment of $16,000 per month after the modification. There is no other change in the terms and conditions. The contract for the additional 1,000 square feet of space, and the combined 3,000 square feet of space meet the definition of a lease.

How should Lessee Corp account for this lease modification?

Analysis

Lessee Corp should account for the lease modification as a separate contract because the modification granted Lessee Corp an additional right of use at a price that is commensurate with the standalone price for the additional space. Based on the facts, since the new contract meets the definition of a lease, at the new lease’s commencement date, Lessee Corp would have two separate leases as follows:

- The original lease for 2,000 square feet for four remaining years

- A new lease for the additional 1,000 square feet for four years

The accounting for the original lease is not impacted by the modification. The new lease would be accounted for as any other new lease, i.e., classified as finance or operating and measured accordingly. See

LG 3 for information on lease classification and

LG 4 for information on lease measurement.