Search within this section

Select a section below and enter your search term, or to search all click Leases

Favorited Content

Contract modification: Lease contract is modified in such a way that the combined contract is accounted for as one lease (LG 5.2) |

● |

● |

● |

● |

● |

Change in lease term: An event occurs that gives the lessee a significant economic incentive to exercise, or not exercise, a renewal option (LG 5.3.1) or an event written in the contract occurs that obligates the lessee to exercise or not exercise an extension or termination option |

● |

● |

● |

● |

|

Change in purchase option assessment: An event occurs that gives the lessee a significant economic incentive to exercise, or not exercise, a purchase option (LG 5.3.1) |

● |

● |

● |

● |

|

Contingency resolution: A contingency on which variable payments are based is met such that the variable payments become fixed (LG 5.3.1) |

● |

● |

|||

Excerpt from ASC 842-10-35-4

Lease commencement date |

January 1, 20X1 |

Initial lease term |

5 years |

Renewal option |

3 years |

Remaining economic life of the leased property |

35 years |

Purchase option |

None |

Annual lease payments for the initial term |

$100,000 |

Annual lease payments for the renewal option |

$114,400 |

Lease increase based on changes in the Consumer Price Index (CPI) |

|

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Remeasured lease term |

5 years; 2 years remaining in the initial term plus 3 years in the renewal period |

Lessee Corp’s incremental borrowing rate on the remeasurement date |

6%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased property |

32 years |

Fair value of the leased property at remeasurement date |

$3.8 million |

CPI on the remeasurement date |

125 |

Right-of-use asset immediately before the remeasurement |

$199,238 |

Lease liability immediately before the remeasurement |

$195,238 |

Year 4 |

Year 5 |

Year 6 |

Year 7 |

Year 8 |

Total |

|

Lease payment |

$104,000 |

$104,000 |

$114,400 |

$114,400 |

$114,400 |

$551,200 |

Discount |

0 |

5,887 |

12,584 |

18,348 |

23,784 |

60,603 |

Present value |

$104,000 |

$98,113 |

$101,816 |

$96,052 |

$90,616 |

$490,597 |

Revised lease liability |

$490,597 |

||||

Original lease liability |

195,238 |

||||

$295,359 |

Dr. Right-of-use asset |

$295,359 |

||

Cr. Lease liability |

$295,359 |

Lease commencement date |

January 1, 20X1 |

Lease term |

5 years with no renewal option |

Remaining economic life of the equipment |

6 years |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Purchase option |

Lessee Corp can purchase the equipment from Lessor Corp at the end of the lease term for $30,000; this is not considered a bargain purchase option |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Remeasurement date |

January 1, 20X3 |

Lessee Corp’s incremental borrowing rate on January 1, 20X3 |

3%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased equipment |

4 years |

Fair value of the leased equipment at remeasurement date |

$300,000 |

Right-of-use asset immediately before the remeasurement |

$272,757 |

Lease liability immediately before the remeasurement |

$285,941 |

Year 3 lease payment |

Year 4 lease payment |

Year 5 lease payment |

Purchase option payment |

Total |

|

Lease payment |

$100,000 |

$100,000 |

$100,000 |

$30,000 |

$330,000 |

Discount |

0 |

2,913 |

5,740 |

2,546 |

11,199 |

Present value |

$100,000 |

$97,087 |

$94,260 |

$27,454 |

$318,801 |

Revised lease liability |

$318,801 |

|||

Original lease liability |

285,941 |

|||

$32,860 |

Dr. Right-of-use asset |

$32,860 |

||

Cr. Lease liability |

$32,860 |

Year |

Remaining cash payments |

Annual lease payment |

Liability balance after annual payment |

Interest expense |

3 |

$330,000 |

$100,000 |

$218,801 |

$6,564 |

4 |

$230,000 |

$100,000 |

$125,365 |

$3,760 |

5 |

$130,000 |

$100,000 |

$29,126 |

$874 |

Right-of-use asset immediately before the remeasurement |

$272,757 |

||

Adjustment to the right-of-use asset |

32,860 |

||

Adjusted right-of-use asset balance |

$305,617 |

||

Remaining economic life at the remeasurement date* |

4 years |

||

Recalculated annual right-of-use asset amortization |

$76,404 |

Lease commencement date |

January 1, 20X1 |

Lease term |

5 years with no renewal option |

Remaining economic life of the equipment |

6 years |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Remeasurement date |

January 1, 20X3 |

Remaining economic life of the leased equipment |

4 years |

Fair value of the leased equipment at remeasurement date |

$200,000 |

Right-of-use asset immediately before the remeasurement |

$272,757 |

Lease liability immediately before the remeasurement |

$285,941 |

Year 3 lease payment |

Year 4 lease payment |

Year 5 lease payment |

Residual value guarantee payment |

Total |

|

Lease payment |

$100,000 |

$100,000 |

$100,000 |

$10,000 |

$310,000 |

Discount |

0 |

4,762 |

9,297 |

1,362 |

15,421 |

Present value |

$100,000 |

$95,238 |

$90,703 |

$8,638 |

$294,579 |

Revised lease liability |

$294,579 |

||

Original lease liability |

285,941 |

||

$8,638 |

Dr. Right-of-use asset |

$8,638 |

||

Cr. Lease liability |

$8,638 |

Year |

Remaining cash payments |

Annual lease payment |

Liability balance |

Interest expense |

3 |

$310,000 |

$100,000 |

$194,579 |

$9,729 |

4 |

$210,000 |

$100,000 |

$104,308 |

$5,215 |

5 |

$110,000 |

$100,000 |

$9,524 |

$476 |

Right-of-use asset immediately before the remeasurement |

$272,757 |

|

Adjustment to the right-of-use asset |

8,638 |

|

Adjusted right-of-use asset balance |

$281,395 |

|

Remaining lease term at the remeasurement date |

3 years |

|

Recalculated annual right-of-use asset amortization |

$93,798 |

Lease commencement date |

January 1, 20X1 |

Lease term |

5 years with no renewal option |

Remaining economic life of the leased property |

35 years |

Purchase option |

None |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Modification date |

January 1, 20X4 |

Modified annual lease payments |

$110,000 |

Lessee Corp’s incremental borrowing rate on January 1, 20X4 |

6%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased property |

32 years |

Fair value of the property at the modification date |

$3.8 million |

Right-of-use asset immediately before the modification |

$199,238 |

Lease liability immediately before the modification |

$195,238 |

Year 4 |

Year 5 |

Year 6 |

Year 7 |

Year 8 |

Total |

|

Lease payment |

$110,000 |

$110,000 |

$110,000 |

$110,000 |

$110,000 |

$550,000 |

Discount |

0 |

6,226 |

12,100 |

17,642 |

22,870 |

58,838 |

Present value |

$110,000 |

$103,774 |

$97,900 |

$92,358 |

$87,130 |

$491,162 |

Revised lease liability |

$491,162 |

|

Original lease liability |

195,238 |

|

$295,924 |

Dr. Right-of-use asset |

$295,924 |

||

Cr. Lease liability |

$295,924 |

Lease commencement date |

January 1, 20X1 |

Lease term |

5 years with no renewal option |

Remaining economic life of the leased property |

35 years |

Purchase option |

None |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Modification date |

January 1, 20X2 |

Revised remaining lease term |

2 years |

Modified annual lease payments |

$110,000 |

Lessee Corp’s incremental borrowing rate on January 1, 20X2 |

6%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased property |

34 years |

Fair value of the property at the modification date |

$4 million |

Right-of-use asset immediately before the modification |

$380,325 |

Lease liability immediately before the modification |

$372,325 |

Year 2 |

Year 3 |

Total |

|

Lease payment |

$110,000 |

$110,000 |

$220,000 |

Discount |

0 |

6.226 |

6,226 |

Present value |

$110,000 |

$103,774 |

$213,774 |

Original lease liability |

$372,325 |

|

Revised lease liability |

213,774 |

|

$158,551 |

Dr. Lease liability |

$158,551 |

||

Cr. Right-of-use asset |

$158,551 |

Lease commencement date |

January 1, 20X1 |

Initial lease term |

5 years (includes a termination option available after year 3 with a termination penalty which is not reasonably certain of exercise at commencement date) |

Remaining economic life of the leased property |

35 years |

Purchase option |

None |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Modification date |

January 1, 20X4 |

Modified annual lease payments |

$90,000 |

Lessee Corp’s incremental borrowing rate on January 1, 20X4 |

4%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased property |

32 years |

Fair value of the leased property at the modification date |

$3.7 million |

Right-of-use asset immediately before the modification |

$199,238 |

Lease liability immediately before the modification |

$195,238 |

Year 4 |

Year 5 |

Total |

|

Lease payment |

$90,000 |

$90,000 |

$180,000 |

Discount |

0 |

3,462 |

3,462 |

Present value |

$90,000 |

$86,538 |

$176,538 |

Revised lease liability |

$176,538 |

|

Original lease liability |

195,238 |

|

($18,700) |

Dr. Lease liability |

$18,700 |

||

Cr. Right-of-use asset |

$18,700 |

Lease commencement date |

January 1, 20X1 |

Lease term |

10 years with no renewal option |

Remaining economic life of the leased equipment |

12 years |

Purchase option |

None |

Annual lease payments |

$100,000 |

Payment date |

Annually on January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Other |

|

Modification date |

January 1, 20x4 |

Remeasured remaining lease term |

4 years |

Modified annual lease payments |

$110,000 |

Lessee Corp’s incremental borrowing rate on the remeasurement date |

6%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased equipment |

9 years |

Fair value of the leased equipment at the modification date |

$900,000 |

Right-of-use asset immediately before the remeasurement |

$574,548 |

Lease liability immediately before the remeasurement |

$607,569 |

Year 4 |

Year 5 |

Year 6 |

Year 7 |

Total |

|

Lease payment |

$110,000 |

$110,000 |

$110,000 |

$110,000 |

$440,000 |

Discount |

0 |

6,226 |

12,100 |

17,462 |

35,969 |

Present value |

$110,000 |

$103,774 |

$97,900 |

$92,358 |

$404,031 |

Revised lease liability |

$404,031 |

|

Original lease liability |

607,569 |

|

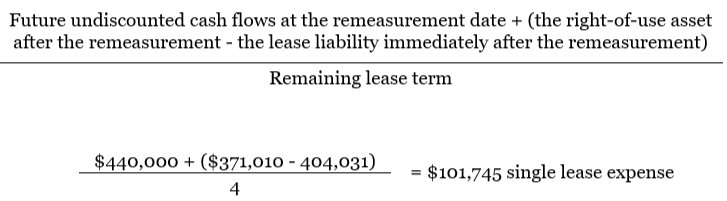

($203,538) |

Dr. Lease liability |

$203,538 |

||

Cr. Right-of-use asset |

$203,538 |

Lease commencement date |

January 1, 20X1 |

Lease term |

5 years with no renewal option |

Remaining economic life of the leased property |

30 years |

Purchase option |

None |

Annual lease payments |

$1,000,000 |

Payment date |

January 1 |

Lessee Corp’s incremental borrowing rate |

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Lease incentive |

Lessor Corp agrees to reimburse Lessee Corp up to $300,000 for leasehold improvements completed within the first two years of the lease |

Other |

|

Remaining lease term |

4 years |

Right-of-use asset immediately before leasehold improvements completion date |

$3,497,534 |

Lease liability immediately before leasehold improvements completion date |

$3,437,534 |

1/1/X1 |

1/1/X2 |

12/31/X2 |

1/1/X3 |

1/1/X4 |

1/1/X5 |

Total |

|

Lease payment |

$1,000,000 |

$1,000,000 |

(300,000) |

$1,000,000 |

$1,000,000 |

$1,000,000 |

$4,700,000 |

Discount |

0 |

(47,619) |

27,891 |

(92,971) |

(136,162) |

(177,298) |

(426,158) |

Present value |

$1,000,000 |

$952,381 |

(272,109) |

$907,029 |

$863,838 |

$822,702 |

$4,273,842 |

1/1/X2 |

1/1/X3 |

1/1/X4 |

1/1/X5 |

Total |

|

Lease payment |

$1,000,000 |

$1,000,000 |

$1,000,000 |

$1,000,000 |

$4,000,000 |

Discount |

0 |

47,619 |

92,971 |

136,162 |

276,752 |

Present value |

$1,000,000 |

$952,381 |

$907,029 |

$863,838 |

$3,723,248 |

Revised lease liability |

$3,723,248 |

|

Original lease liability |

3,437,534 |

|

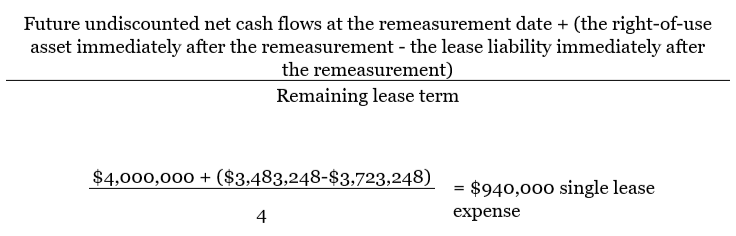

($285,714) |

Dr. Cash (for lease incentive received) |

$300,000 |

||

Cr. Right-of-use asset |

$14,286 |

||

Cr. Lease liability |

$285,714 |

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Leases