A modification of a lease may result in a partial termination of the lease. Examples of events that result in a partial termination include terminating the right to use one or more underlying assets and decreasing the leased space. A decrease in lease term is not considered a partial termination event. A partial termination should be recorded by adjusting the lease liability and right-of-use asset. The right-of-use asset should be decreased on a basis proportionate to the partial termination of the existing lease. The difference between the decrease in the carrying amount of the lease liability resulting from the modification and the proportionate decrease in the carrying amount of the right-of-use asset should be recorded in the income statement.

There are two ways to determine the proportionate reduction in the right-of-use asset. It can be based on either the reduction to the right-of-use asset or on the reduction to the lease liability. For example, if a lessee decreases the amount of space it is leasing in an office building by 45% and as a result, the lease liability decreases by 50%, the right-of-use asset could be decreased by either 45% or 50%. See Example 18 beginning at

ASC 842-10-55-177 and Example LG 5-10 for examples of lessee accounting for partial lease terminations.

A lessee should treat its selected method as an accounting policy election by class of underlying asset. The policy should be applied consistently to all modifications that decrease the scope of a lease.

Example LG 5-10 illustrates a lessee’s accounting for modification of an operating lease without a change in lease classification.

EXAMPLE LG 5-10

Accounting for a modified operating lease with a partial termination - no change to lease classification

On January 1, 20X1, Lessee Corp enters into a contract with Lessor Corp to lease property to be used as a warehouse. The following table summarizes information about the lease and the leased property:

|

|

|

5 years with no renewal option

|

|

100,000 square feet of warehouse space

|

Remaining economic life of the leased property

|

|

|

|

|

Lessee Corp’s incremental borrowing rate

|

5%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

|

- Title to the leased property remains with Lessor Corp upon lease expiration

- Fair value of the leased property at commencement $2.5 million

- Lessee Corp incurs $10,000 initial direct costs

|

On January 1, 20X2, Lessee Corp and Lessor Corp amend the original lease contract to decrease the leased space from 100,000 square feet to 50,000 square feet, effective immediately. Commensurate with the reduction in leased space, the annual lease payment will be reduced from $100,000 a year to $50,000 a year. Lessee Corp is also required to pay Lessor Corp a one-time termination penalty of $30,000 along with its next lease payment.

The following table summarizes information pertinent to the lease modification.

|

|

|

|

Revised annual lease payments

|

|

|

Lessee Corp’s incremental borrowing rate on January 1, 20X2

|

6%

The rate Lessor Corp charges Lessee Corp in the lease is not readily determinable by Lessee Corp

|

Remaining economic life of the leased property

|

|

Fair value of the leased property at the modification date

|

|

Right-of-use asset immediately before the modification

|

|

Lease liability immediately before the modification

|

|

View table

Lessee Corp has historically accounted for the lease of 100,000 square feet as one lease component. Lessee Corp has previously made an accounting policy election to calculate the reduction in the right-of-use asset in proportion to the reduction to the right of use (i.e., decrease in leased space). Assume that any additional right of use, the original contract, and the modified contract meet the definition of a lease.

How would Lessee Corp account for the lease modification?

Analysis

Determine if the lease modification is a separate new contract

As the modification does not grant an additional right of use, Lessee Corp would determine that the modification is not a separate new contract. Since the modified contract meets the definition of a lease, Lessee Corp would account for one new modified lease as of January 1, 20X4.

Determine if the modification is a partial termination

Since Lessee Corp surrenders control of 50,000 square feet of space immediately the modification is a partial termination.

Reassess lease classification based on the terms of the modified lease

Based on the facts at lease commencement, Lessee Corp could reasonably conclude that the lease was an operating lease since none of the criteria for a finance lease were met. At the lease modification date, Lessee Corp could reasonably conclude that the lease continues to be an operating lease since none of the criteria for a finance lease are met (see

LG 3.3 for lease classification criteria).

Account for the modified lease

Lessee Corp would remeasure the lease as of the modification date as follows:

Balance sheet impact

Lessee Corp would remeasure the lease liability on the date of the modification by calculating the present value of the remaining four future lease payments, including the termination penalty, for the modified lease term using Lessee Corp’s current discount rate of 6%. The modified lease liability would be $213,651, as shown in the following table.

|

Year 2 |

Year 3 |

Year 4 |

Year 5 |

Total |

Lease payment |

$80,000 |

$50,000 |

$50,000 |

$50,000 |

$230,000 |

Discount |

0 |

2,830 |

5,500 |

8,019 |

16,349 |

Present value |

$80,000 |

$47,170 |

$44,500 |

$41,981 |

$213,651 |

To calculate the adjustment to the lease liability, Lessee Corp would compare the recalculated and original lease liability balances on the modification date.

Original lease liability |

$372,325 |

|

Revised lease liability |

213,651 |

|

|

The lessee has an accounting policy choice for remeasuring the right-of-use asset either (a) based on the change in lease liability; or (b) based on the remaining right of use. The remeasurement of the right-of-use asset under both these approaches is illustrated below.

(a) Remeasuring the right-of-use asset based on the change in lease liability

Under the policy election to remeasure the right-of-use asset in proportion to the change in lease liability, the post-modification right-of-use asset is $218,241 (pre-modification right-of-use asset of $380,325 multiplied by 42.6% reduction in lease liability ($158,674 divided by $372,325)). To calculate the adjustment to the right-of-use asset, Lessee Corp would compare the recalculated and original right-of-use asset balances on the modification date as follows.

Original right of use asset |

$380,325 |

|

Revised right of use asset |

218,241 |

|

|

Lessee Corp would record the following journal entry to adjust the lease liability and right-of-use asset, with the difference between the adjustment to the lease liability and right-of-use asset being recorded to the income statement.

Dr. Lease liability |

$158,674 |

|

|

|

Cr. Right of use asset |

|

$162,084 |

|

Income statement impact

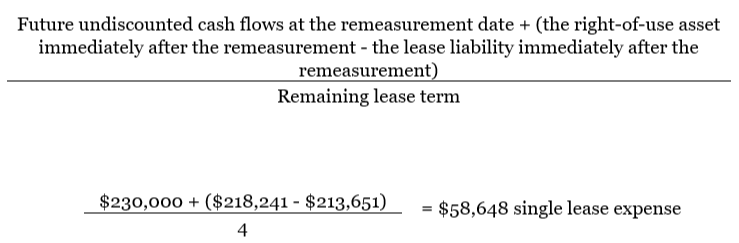

Lessee Corp would recalculate the single lease expense using the following formula.

Lessee Corp would recognize single annual lease expense of $58,648 for the remaining term of the lease.

(b) Remeasuring the right-of-use asset based on the remaining right of use

Under the accounting policy election to remeasure the right-of-use asset in proportion to the remaining right of use (i.e., decrease in leased space), the post-modification right-of-use asset is $190,163 (pre-modification right-of-use asset of $380,325 multiplied by the 50% reduction in leased space). To calculate the adjustment to the right-of-use asset, Lessee Corp would compare the recalculated and original right-of-use asset balances on the modification date as follows.

Original right of use asset |

$380,325 |

|

Revised right of use asset |

190,163 |

|

|

The adjustment to the lease liability is $186,162 (pre-modification lease liability of $372,325 multiplied by the 50% reduction in leased space).

Lessee Corp would record the following journal entry to adjust the lease liability and right-of-use asset, with the difference between the adjustment to the lease liability and right-of-use asset being recorded to the income statement.

Dr. Lease liability |

$186,162 |

|

|

|

Cr. Right of use asset |

|

$190,162 |

|

Next, Lessee Corp would adjust the lease liability to equal the present value of the remaining future lease payments (as calculated above). The adjustment would be calculated as follows:

Present value of remaining future lease payments |

$213,651 |

|

Lease liability balance (after adjustment from the journal entry above) |

186,163 |

|

|

Lessee Corp would record the following journal entry:

Dr. Right-of-use asset |

$27,488 |

|

|

Cr. Lease liability |

|

27,488 |

|

After this entry, the post-modification right-of-use asset would be $217,651 and the post-modification lease liability would be $213,651.

Income statement impact

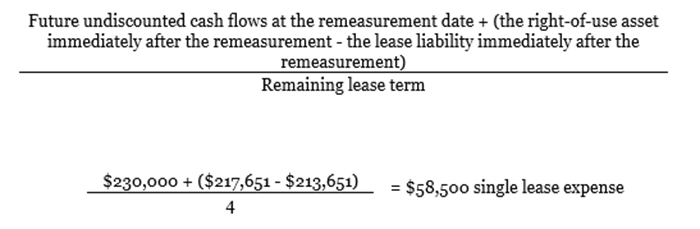

Lessee Corp would recalculate the single lease expense using the following formula.

Lessee Corp would recognize single annual lease expense of $58,500 for the remaining term of the lease.

A comparison of the income statement and balance sheet impact under the two alternative policy choices is below.

Remeasuring right-of-use asset based on |

Balance sheet |

Income statement* |

Revised lease liability |

Revised right-of-use asset |

Loss recorded at modification date |

Annual lease expense for remaining lease term |

Change in lease liability |

$213,651 |

$218,241 |

$3,410 |

$58,648 |

Remaining right of use |

$213,651 |

$217,651 |

$4,000 |

$58,500 |

View table

* Note the total income statement impact for either method should be the same over the entire lease term, the difference is timing over when the amounts are recognized. In this example, the total income statement impact for each method does not match exactly due to rounding.

When a lessee and lessor agree to early terminate a portion of the leased asset (e.g., a floor of a building or a portion of a warehouse) against payment of a termination penalty by the lessee to the lessor, the lessee should apply modification accounting to the remaining lease. That is, termination accounting should not be applied, and the lessee should allocate the termination penalty to the remaining lease. If there are multiple components in the remaining lease, the lessee should allocate the termination penalty to these components based on their relative standalone price at the contract modification date. The subsequent accounting will depend on the classification of the remaining lease components.

There may be a situation when a lessee and lessor have multiple lease contracts with each other and they agree that the lessee will early exit one lease in six months against payment of a termination penalty and simultaneously modify another lease. In this instance, the lessee should apply modification accounting to all the leases and allocate the termination penalty and the remaining contract consideration for all the leases to all the lease components based on their relative standalone price at the modification date. The subsequent accounting will depend on the classification of each of the lease components.

When a lessee and a lessor have multiple leases between them and agree to early terminate one lease with immediate exit by the lessee from the leased property against payment of a termination penalty without amending any of the other leases, the lessee should apply termination accounting to the early terminated lease. That is, the lessee should expense the entire termination penalty. However, if in addition to agreeing to early terminate one lease with immediate exit by the lessee from the leased property, the lessee and lessor also modify another lease, we believe the lessee should allocate the termination penalty and the remaining contract consideration for the leases that will continue to all the lease components, including the terminated lease, based on their relative standalone price at the modification date. The subsequent accounting for the remaining lease components will depend on their classification.

Example LG 5-11 illustrates recognition of a termination penalty by a lessee due to a lease modification when the lease term of one lease is extended and another lease with the same lessor is early terminated with immediate exit by the lessee from the property at the lease amendment date.

EXAMPLE LG 5-11

Accounting for a concurrent early lease termination of one lease and a lease extension of another lease between the same lessee and lessor - no change to lease classification

Lessee Corp is 2 years into a 7-year operating lease for an office building and 3 years into a 5-year operating lease for a warehouse with Lessor Corp. Lessor Corp and Lessee Corp agree to concurrently amend the two leases such that Lessee Corp will (a) extend the term of office building lease by three more years (i.e., a total remaining lease term of eight years), (b) vacate the warehouse immediately at the amendment date, and (c) pay Lessor Corp a termination penalty of $2 million at the lease amendment date. Lessee Corp will continue to classify the office building lease as an operating lease after the amendment.

The remaining rents under the warehouse lease are above market at the lease amendment date. The fair value of the amount that would need to be paid to someone to assume the warehouse lease is $2.5 million.

Assume that the present value of the remaining lease payments on the office building lease at the lessee’s discount rate on the lease amendment date is $10 million and the fair value of the comparable market rents is $9 million.

How should Lessee Corp account for the lease amendments?

Analysis

The leases standard does not address the scenario in this example. We believe in this fact pattern, $12 million ($2 million termination payment for the warehouse lease + $10 million present value of remaining rent on the office building lease) should be allocated to both the lease termination and the amendment. The amount allocated to the warehouse lease should be expensed at the amendment date and the amount allocated to the office building lease should be recognized as straight-line rent expense during the remaining eight-year lease term. The allocation is as follows:

(in million$) |

Fair value

(A) |

Relative %

(A/$11.50)

(B) |

Actual amount

(C) |

Allocated amount

(B × $12.0)

(D) |

Warehouse lease termination payment |

$2.5 |

21.7% |

$2.0 |

$2.6 |

Office building lease remaining lease payments |

9.0 |

78.3% |

$10.0 |

9.4 |

Total |

$11.50 |

100% |

$12.0 |

$12.0 |

Based on the above, Lessee Corp would expense $2.6 million as termination for the warehouse lease and recognize $9.4 million as straight-line rent expense during the remaining eight-year lease term for the office building lease.