Search within this section

Select a section below and enter your search term, or to search all click Loans and investments

Favorited Content

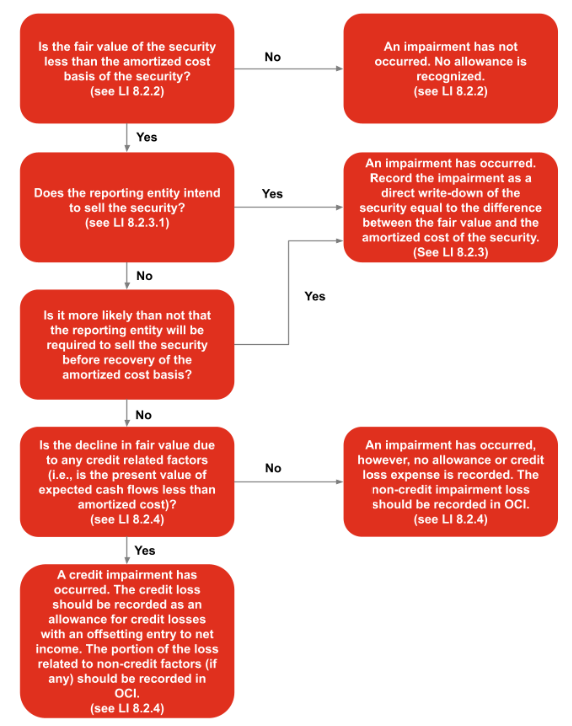

An investment is impaired if the fair value of the investment is less than its amortized cost basis.

An entity shall not consider a basis adjustment related to an existing portfolio layer method hedge designated in accordance with paragraph 815-20-25-12A when measuring impairment of the individual investments or individual beneficial interest included in a closed portfolio hedged using the portfolio layer method

Impairment shall be assessed at the individual security level (referred to as an investment). The impairment assessment of the individual securities or individual beneficial interest in a closed portfolio hedged using the portfolio layer method shall not consider the basis adjustment related to an existing portfolio layer method hedge. Individual security level means the level and method of aggregation used by the reporting entity to measure realized and unrealized gains and losses on its debt securities. (For example, debt securities bearing the same Committee on Uniform Security Identification Procedures [CUSIP] number that were purchased in separate trade lots may be aggregated by a reporting entity on an average cost basis if that corresponds to the basis used to measure realized and unrealized gains and losses for the debt securities.) Providing a general allowance for an unidentified impairment in a portfolio of debt securities is not appropriate.

An entity shall not combine separate contracts (a debt security and a guarantee or other credit enhancement) for purposes of determining whether a debt security is impaired or can contractually be prepaid or otherwise settled in such a way that the entity would not recover substantially all of its cost.

Definition from ASC Master Glossary

An entity shall not combine separate contracts (a debt security and a guarantee or other credit enhancement) for purposes of determining whether a debt security is impaired or can contractually be prepaid or otherwise settled in such a way that the entity would not recover substantially all of its cost.

If an entity intends to sell the debt security (that is, it has decided to sell the security), or more likely than not will be required to sell the security before recovery of its amortized cost basis, any allowance for credit losses shall be written off and the amortized cost basis shall be written down to the debt security’s fair value at the reporting date with any incremental impairment reported in earnings. If an entity does not intend to sell the debt security, the entity shall consider available evidence to assess whether it more likely than not will be required to sell the security before the recovery of its amortized cost basis (for example, whether its cash or working capital requirements or contractual or regulatory obligations indicate that the security will be required to be sold before the forecasted recovery occurs). In assessing whether the entity more likely than not will be required to sell the security before recovery of its amortized cost basis, the entity shall consider the factors in paragraphs 326-30-55-1 through 55-2.

Excerpt from ASC 326-30-35-10

If an entity does not intend to sell the debt security, the entity shall consider available evidence to assess whether it more likely than not will be required to sell the security before the recovery of its amortized cost basis (for example, whether its cash or working capital requirements or contractual or regulatory obligations indicate that the security will be required to be sold before the forecasted recovery occurs).

In determining whether a credit loss exists, an entity shall consider the factors in paragraphs 326-30-55-1 through 55-4 and use its best estimate of the present value of cash flows expected to be collected from the debt security. One way of estimating that amount would be to consider the methodology described in paragraphs 326-30-35-8 through 35-10. Briefly, the entity would discount the expected cash flows at the effective interest rate implicit in the security at the date of acquisition.

In determining whether a credit loss exists, an entity shall consider the factors in paragraphs 326-30-55-1 through 55-4 and use its best estimate of the present value of cash flows expected to be collected from the debt security. One way of estimating that amount would be to consider the methodology described in paragraphs 326-30-35-8 through 35-10. Briefly, the entity would discount the expected cash flows at the effective interest rate implicit in the security at the date of acquisition.

As an accounting policy election for each major security type of debt securities classified as available-for-sale securities, an entity may adjust the effective interest rate used to discount expected cash flows to consider the timing (and changes in the timing) of expected cash flows resulting from expected prepayments.

If the security’s contractual interest rate varies based on subsequent changes in an independent factor, such as an index or rate, for example, the prime rate, the London Interbank Offered Rate (LIBOR), or the U.S. Treasury bill weekly average, that security’s effective interest rate (used to discount expected cash flows as described in paragraph 326-30-35-7) may be calculated based on the factor as it changes over the life of the security or is projected to change over the life of the security, or may be fixed at the rate in effect at the date an entity determines that the security has a credit loss as determined in accordance with paragraphs 326-30-35-1 through 35-2. The entity’s choice shall be applied consistently for all securities whose contractual interest rate varies based on subsequent changes in an independent factor. An entity is not required to project changes in the factor for purposes of estimating expected future cash flows. If the entity projects changes in the factor for the purposes of estimating expected future cash flows, it shall use the same projections in determining the effective interest rate used to discount those cash flows. In addition, if the entity projects changes in the factor for the purposes of estimating expected future cash flows, it shall adjust the effective interest rate used to discount expected cash flows to consider the timing (and changes in the timing) of expected cash flows resulting from expected prepayments in accordance with paragraph 326-30-35-7A. Subtopic 310-20 on receivables—nonrefundable fees and other costs provides guidance on the calculation of interest income for variable rate instruments.

Par amount |

$1,000 paid at maturity |

Coupon rate |

4.5% paid annually |

Maturity date |

December 31, 20X4 |

Year |

Contractual cash flows |

Cash flows expected at 12/31/X0 |

Decrease in expected cash flows |

20X1 |

45 |

45 |

— |

20X2 |

45 |

45 |

— |

20X3 |

45 |

45 |

— |

20X4 |

$1,045 |

$905 |

$140 |

Total cash flows |

$1,180 |

$1,040 |

$140 |

Present value of cash flows |

$1,000 |

$883 |

$117 |

Amortized cost basis on December 31, 20X0 |

$1,000 |

Allowance for credit losses |

(117) |

Net value on December 31, 20X0 |

883 |

Unrealized loss |

(183) |

Fair value on December 31, 20X0 |

$700 |

Dr. Provision expense |

$117 |

|

Dr. OCI – AFS unrealized loss |

$183 |

|

Cr. Allowance for credit losses |

$117 |

|

Cr. AFS security fair value |

$183 |

Par amount |

$1,000 paid at maturity |

Coupon rate |

4.5% paid annually |

Maturity date |

December 31, 20X4 |

Year |

Contractual cash flows |

Cash flows expected at 12/31/X1 |

Decrease in expected cash flows |

20X2 |

45 |

45 |

— |

20X3 |

45 |

45 |

— |

20X4 |

$1,045 |

$935 |

$110 |

Total cash flows |

$1,135 |

$1,025 |

$110 |

Present value of cash flows |

$1,000 |

$904 |

$96 |

Amortized cost basis on December 31, 20X1 |

$1,000 |

Allowance for credit losses at January 1, 20X1 |

(117) |

Adjustment to allowance |

21 |

Net value on December 31, 20X1 |

$904 |

Unrealized loss in OCI at January 1, 20X1 |

(183) |

Adjustment to OCI |

(21) |

Fair value on December 31, 20X1 |

$700 |

Dr. Allowance for credit losses |

$21 |

|

Dr. OCI – AFS unrealized loss |

$21 |

|

Cr. Provision expense |

$21 |

|

Cr. AFS security fair value |

$21 |

Par amount |

$1,000 paid at maturity |

Coupon rate |

4.5% paid annually |

Maturity date |

December 31, 20X4 |

Dr. Allowance for credit losses |

$96 |

|

Dr. Provision expense |

$904 |

|

Dr. AFS security – unrealized loss |

$204 |

|

Cr. OCI |

$204 |

|

Cr. AFS security – Amortized cost basis |

$1,000 |

Dr. Cash |

$500 |

|

Cr. Provision expense |

$500 |

The amortized cost basis is the amount at which a financing receivable or investment is originated or acquired, adjusted for applicable accrued interest, accretion, or amortization of premium, discount, and net deferred fees or costs, collection of cash, writeoffs, foreign exchange, and fair value hedge accounting adjustments.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Loans and investments