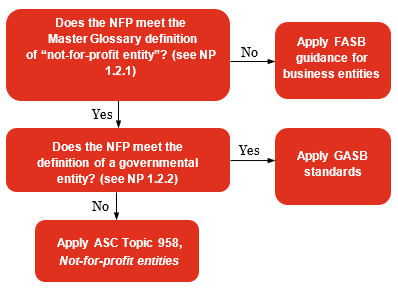

For accounting and financial reporting purposes, an NFP is an entity that possesses certain characteristics that distinguish it from a business enterprise. The

ASC Master Glossary defines a not-for-profit entity as follows:

Definition from ASC Master Glossary

Not-for-profit entity: An entity that possesses the following characteristics, in varying degrees, that distinguish it from a business entity:

- Contributions of significant amounts of resources from resource providers who do not expect commensurate or proportionate pecuniary return

- Operating purposes other than to provide goods or services at a profit

- Absence of ownership interests like those of business entities.

Entities that clearly fall outside this definition include the following:

- All investor-owned entities

- Entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants, such as mutual insurance entities, credit unions, farm and rural electric cooperatives, and employee benefit plans.

The absence of ownership interests is often the key factor in distinguishing an NFP from a business entity. While one NFP can legally control another NFP (see

NP 5), NFPs generally are not owned by individuals in the same way that stockholders own for-profit corporations. Thus, a general characteristic shared by nearly all NFPs is that they do not have defined ownership interests that can be sold, transferred, or redeemed, or that convey entitlement to a share of a residual distribution of resources in the event of liquidation of the organization.

Question NP 1-2 provides an example of an organization formed legally as a not-for-profit and granted tax-exempt status by the IRS that does not meet the GAAP definition of an NFP.

Question NP 1-2

Two hospitals (both IRS tax-exempt organizations) jointly form an LLC to operate urgent care clinics in their service area. The LLC is also granted tax-exempt status by the IRS. For accounting and financial reporting purposes, does the LLC meet the definition of a not-for-profit entity?

PwC response

For financial reporting purposes, the LLC is considered a business entity because each hospital has an ownership interest in the LLC, even though the purpose of the venture is to carry out a nonprofit activity. An NFP formed as a stock corporation, partnership, LP or LLC that provides its participants with ownership interests would not meet the

Master Glossary definition of a not-for-profit entity.

The

Master Glossary definition explicitly excludes “entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants.” Certain specific types of entities, such as mutual insurance companies, credit unions, and certain other cooperatives, typically operate on a cooperative basis for the benefit of their members and distribute net earnings on a patronage basis. While such organizations might be legally organized as not-for-profit corporations, they are regarded as business entities for accounting and reporting purposes.

Question NP 1-3 addresses the question as to whether a caption such as “members’ equity” precludes application of

ASC 958.

Question NP 1-3

A not-for-profit insurance entity was formed to provide coverage to not-for-profit member organizations. Its balance sheet displays a “members’ equity” section. Does the fact that entities record “members’ equity” preclude them from meeting the definition of an NFP?

PwC response

No, using the caption or recording amounts as members’ equity does not preclude an entity from meeting the definition of an NFP.

If the nonprofit insurer operates for the benefit of its membership in general, and members do not have ownership interests in the manner of a cooperative, it would likely meet the definition of a not-for-profit entity for accounting purposes and thus, would apply

ASC 958. In that situation, the “members’ equity” is simply the surplus, if any, after the organization’s obligations have been paid. Describing that amount as “members’ equity” might simply indicate that any surpluses are retained to keep the entity self-sustaining.

On the other hand, nonprofit insurers that are formed on a cooperative basis provide benefits to their members directly and proportionately to their membership interests and distribute net earnings on a patronage basis in a manner similar to dividends in a stock company. Typically, each member has a capital account that increases or decreases as a result of the entity’s operations. If the NFP insurance entity has these characteristics, it would not meet the

Master Glossary definition of a not-for-profit entity and, therefore, would not apply

ASC 958.

NFPs possess other characteristics noted in the

ASC Master Glossary definition to varying degrees. For example, while some NFPs derive most of their support from contributions, others obtain their financial resources from sales of goods and services, with little if any support from contributions. The latter group, in charging for goods or services they provide, have motivations that differ from those of commercial enterprises. The ultimate objective of sales by a commercial enterprise is to realize net profits for its owners; for an NFP, it is to generate resources to be self-sustaining in order to continue to fulfill its mission. The fact that NFPs do not seek to generate profit for purposes of distributing it to owners or investors does not mean that they cannot generate a profit. In order to be financially viable, an NFP must, over the long run, receive at least as much in resource inflows as is needed to both (1) provide goods and services and (2) replace capital assets.

Question NP 1-4 addresses whether tax-exempt status conferred by the IRS or other state regulations is a factor in accounting for an entity as an NFP.

Question NP 1-4To apply

ASC 958, does a not-for-profit entity need to qualify for IRS tax-exempt status?

PwC response

No. An entity’s tax status is not part of the definition of a not-for-profit entity in the

ASC Master Glossary, and, thus, is not a factor in determining the applicable reporting framework.