Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

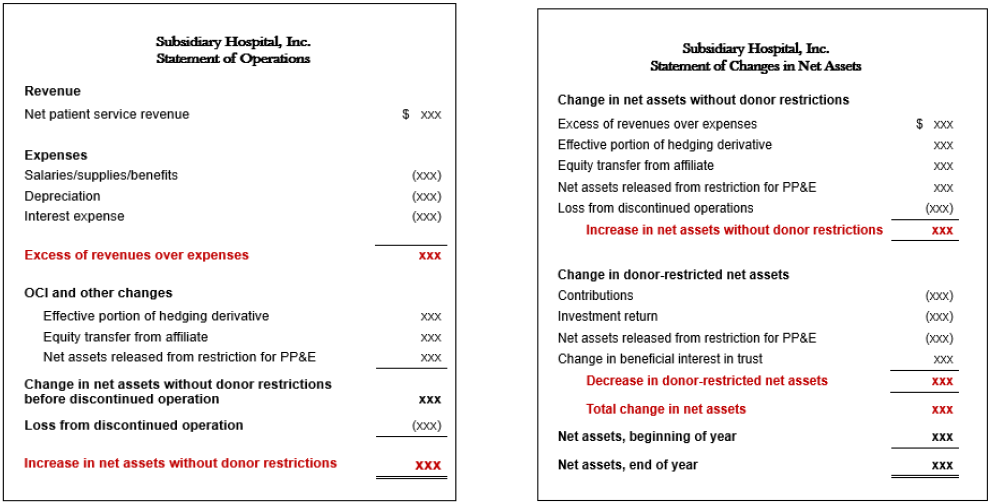

The basic financial statements of health care entities consist of a balance sheet, a statement of operations, a statement of changes in equity (or net assets), a statement of cash flows, and notes to the financial statements.

View image

View image

For not-for-profit, business-oriented health care entities, the statement of operations may be combined with the statement of changes in equity (net assets).

The statement of operations for not-for-profit, business-oriented health care entities shall include a performance indicator. Because of the importance of the performance indicator, it shall be clearly labeled with a descriptive term such as revenues over expenses, revenues and gains over expenses and losses, recognized income, or performance earnings. Not-for-profit, business-oriented health care entities shall report the performance indicator in a statement that also presents the total changes in net assets without donor restrictions. Other changes in net assets may be presented separately or in the same statement.

Definition from ASC Master Glossary

Performance indicator: A performance indicator reports results of operations. A performance indicator and the income from continuing operations reported by for-profit health care entities generally are consistent, except for transactions that clearly are not applicable to one kind of entity (for example, for-profit health care entities typically would not receive contributions, and not-for-profit health care entities would not award stock compensation). That is, a performance indicator is analogous to income from continuing operations of a for-profit entity.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities