Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

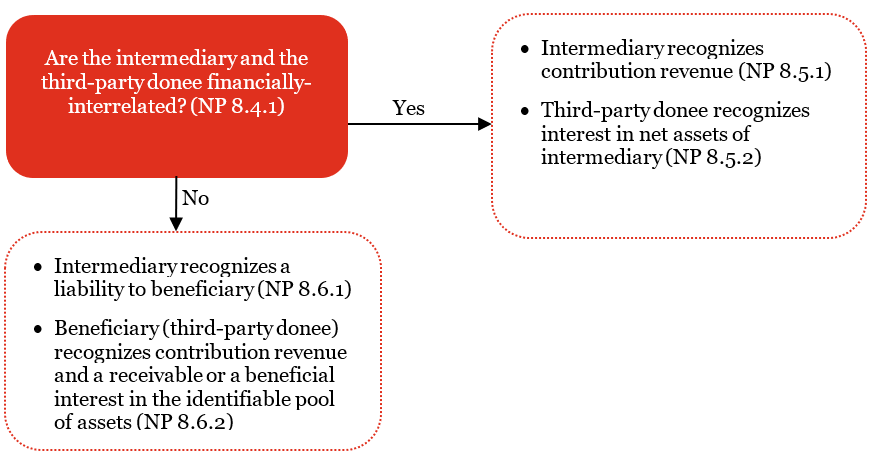

A specified beneficiary shall recognize its rights to the assets (financial or nonfinancial) held by a recipient entity as an asset unless the recipient entity is explicitly granted variance power (see paragraph 958-605-25-25). Those rights are any one of the following:

Excerpt from ASC 958-20-25-1

A foundation that exists to raise, hold, and invest assets for the specified beneficiary or for a group of affiliates of which the specified beneficiary is a member generally is financially interrelated with the not-for-profit entity or entities it supports.

Excerpt from ASC 958-20-15-2

A recipient entity and a specified beneficiary are financially interrelated entities if the relationship between them has both of the following characteristics:

Excerpt from ASC 958-20-15-2(a)

…the ability to influence the operating and financial decisions of the other [entity]…may be demonstrated in several ways, including the following:

ASC Master Glossary

Ongoing economic interest in the net assets of another: A residual right to another not-for-profit entity's (NFP's) net assets that results from an ongoing relationship. The value of those rights increases or decreases as a result of the investment, fundraising, operating, and other activities of the other entity.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities