Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

Excerpt from ASC 958-360-35-5

The future economic benefits or service potentials of individual items comprising collections (as that term is commonly used, not necessarily as defined within this Subtopic) and of buildings and other structures—including those designated as landmarks, monuments, cathedrals, or historical treasures—are used up not only by wear and tear in intended uses but also by the continuous destructive effects of pollutants, vibrations, and so forth. The cultural, aesthetic, or historical values of those assets can be preserved, if at all, only by periodic major efforts to protect, clean, and restore them, usually at significant cost.

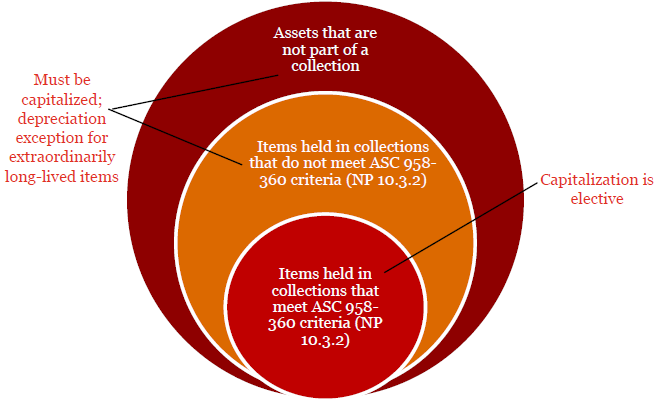

Consistent with the accepted practice for land used as a building site, depreciation need not be recognized on an individual work of art or historical treasure whose economic benefit or service potential is used up so slowly that its estimated useful life is extraordinarily long. A work of art or historical treasure shall be deemed to have that characteristic only if verifiable evidence exists demonstrating both of the following characteristics:

Excerpt from ASC Master Glossary

Collections: Collections generally are held by museums; botanical gardens; libraries; aquariums; arboretums; historic sites; planetariums; zoos; art galleries; nature, science, and technology centers; and similar educational, research, and public service organizations that have those divisions; however, the definition is not limited to those entities nor does it apply to all items held by those entities.

Original definition

|

As amended by ASU 2019-03

|

Collections: Works of art, historical treasures, or similar assets that meet all of the following criteria:

|

Collections: Works of art, historical treasures, or similar assets that meet all of the following criteria:

|

An NFP that holds works of art, historical treasures, and similar items that meet the definition of a collection has the following three alternative policies for reporting that collection:

Excerpt from ASC 958-360-45-3

If an NFP does not recognize and capitalize its collections or capitalizes its collections prospectively, a line item shall be shown on the face of the statement of financial position that refers to the disclosures about collections required by paragraph 958-360-50-6. That line item shall be dated if collections are capitalized prospectively, for example, collections acquired since January 1, 20X1 (Note X).

20X1

|

||

Collections (Note X)

|

$ —

|

An NFP that does not recognize and capitalize its collections shall report all of the following on the face of its statement of activities, separately from revenues, expenses, gains, and losses:

Without donor restrictions |

With donor restrictions |

Total |

||

Revenues and other support |

$ 100 |

$1,000 |

$1,100 |

|

Net assets released from restrictions |

600 |

(600) |

-- |

|

Expenses |

(750) |

-- |

(750) |

|

Change in net assets before changes related to collection items not capitalized |

50 |

400 |

450 |

|

Change in net assets related to collection items not capitalized: |

||||

Proceeds from sales of collection items |

25 |

60 |

85 |

|

Proceeds from insurance recoveries |

10 |

45 |

55 |

|

Collection items purchased |

(40) |

(150) |

(190) |

|

(5) |

(45) |

(50) |

||

Change in net assets |

$ 45 |

$ 355 |

$400 |

|

An NFP that does not recognize and capitalize its collections or that capitalizes collections prospectively shall describe its collections, including their relative significance, and its stewardship policies for collections. If collection items not capitalized are deaccessed during the period, it also shall describe the items given away, damaged, destroyed, lost, or otherwise deaccessed during the period or disclose their fair value.

Excerpt from AAG-NFP 7.29

Excerpt from ASC 958-360-45-3

If an NFP does not recognize and capitalize its collections or capitalizes its collections prospectively, a line item shall be shown on the face of the statement of financial position that refers to the disclosures about collections required by paragraph 958-360-50-6. That line item shall be dated if collections are capitalized prospectively, for example, collections acquired since January 1, 20X1 (Note X).

20X1

|

|

Collections acquired since January 1, 1995 (Note X)

|

$ XX,XXX,XXX

|

Excerpt from AAG-NFP 7.29

ASC 958-360-50-7 (as amended by ASU 2019-03)

Excerpt from ASC 958-805-25-23

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities