Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

Definitions from ASC Master Glossary

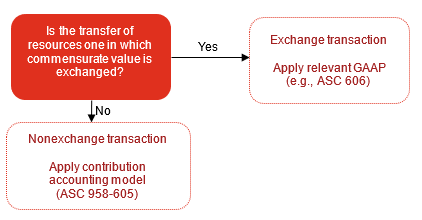

Exchange: An exchange (or exchange transaction) is a reciprocal transfer between two entities that results in one of the entities acquiring assets or services or satisfying liabilities by surrendering other assets or services or incurring other obligations

Contribution (excerpt): An unconditional transfer of cash or other assets, as well as unconditional promises to give, to an entity or a reduction, settlement, or cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner…

Excerpt from ASC 958-605-55-5

A resource provider may sponsor research and development activities at a research university and retain proprietary rights or other privileges, such as patents, copyrights, or advance and exclusive knowledge of the research outcomes. The research outcomes may be intangible, uncertain, or difficult to measure, and may be perceived by the university as a sacrifice of little or no value; however, their value often is commensurate with the value that a resource provider expects in exchange.

Indicative of an exchange

|

Indicative of nonexchange

|

|---|---|

|

|

|

|

|

|

Rationale used to support treatment as exchange transaction

|

ASU 2018-08’s clarifications

|

|---|---|

The federal government does not make “donations;” thus, the use of contribution accounting for federal grants is not appropriate.

|

Automatically defaulting to “exchange” treatment for federal grants is not appropriate. The type of resource provider should not override the substance of an arrangement with nonreciprocal characteristics.

As used in GAAP, the term “contribution” refers to nonexchange or nonreciprocal transactions. It is not focused narrowly on charitable donations.

|

A government agency can carry out its mission through outsourcing certain activities to subcontractors. The value received in exchange is the discharge of the agency’s own responsibilities.

|

In an exchange transaction, the resource provider benefits directly. If the general public receives the primary benefit from the activities, any benefits received by the resource provider would be indirect or incidental.

Neither the intangible benefits arising from having its mission furthered nor the positive sentiments arising from acting as a donor would constitute commensurate value received by a resource provider.

|

Grant-funded activities that benefit the public at large are reciprocal, because “general public” is synonymous with “government.” Benefits received by the public at large are tantamount to benefits received by the government itself.

|

The public and the government cannot be viewed as the same party for revenue recognition purposes.

|

Excerpt from ASC 958-605-15-6

The guidance in the Contributions Received Subsections does not apply to the following transactions and activities:

…

e. Transfers of assets (typically from a government entity) that are part of an existing exchange transaction between a recipient and an identified customer. Some examples include payments under Medicare and Medicaid programs, provisions of health care or education services by a government for its employees, and Pell Grants or similar state or local government tuition assistance programs. In those instances, an entity shall apply the applicable guidance (for example, Topic 606 on revenue from contracts with customers) to the underlying transaction with the customer, and the payments from the third parties would be payments on behalf of those customers.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities