When a gain is expected from a curtailment resulting from employee terminations, it should not be recognized until those employees terminate. In some situations, employees may be terminated over a period of time pursuant to a single overall restructuring program, and those aggregate terminations may be sufficient to result in a curtailment.

Employers can elect to recognize the curtailment gains in this situation in one of two ways:

a) measure and record the curtailment gain based on the cumulative terminations at the end of each interim reporting period, even if the terminations up to that date would not by themselves meet the significance threshold for a curtailment event, or

b) postpone any curtailment gain recognition until the aggregate terminations result in a sufficient reduction in expected years of future service to meet the significance threshold.

Whichever approach is selected would constitute an accounting policy election and should be followed consistently for future termination events.

Example PEB 4-1 addresses the timing of recognition of curtailment gains and losses related to a plan amendment when the full impact of the curtailment may not be known until a later period.

EXAMPLE PEB 4-1

Recognition of curtailment gains and losses when the impact of the curtailment is not yet known

On October 31, 20X1, PEB Corporation's board of directors approved freezing PEB Corporation’s defined benefit plan effective immediately. In conjunction with freezing the plan, affected employees will need to make certain one-time irrevocable elections regarding matters such as early retirement, joint and survivor annuities, and the treatment of a companion profit sharing defined contribution account that the reporting entity allows to be annuitized through the pension plan. The participants of the plan are to be provided with detailed information about their elections during a specified time period in early 20X2 and will need to make their final elections by June 30, 20X2. PEB Corporation's action to freeze the pension plan eliminates the accrual of defined benefits for future years of service and, thus, results in a curtailment of the plan.

When should PEB Corporation record the curtailment?

The curtailment gain or loss should be calculated in the fourth quarter of 20X1 using management's best estimate about how the PBO will be affected by the plan changes and employee elections. If the final impact of the employee elections in June 20X2 is different from their original estimates, these differences should be treated as an actuarial gain or loss at the next measurement date and accounted for in accordance with PEB Corporation’s policy (i.e., amortization or immediate recognition).

PEB Corporation should not wait until the employee elections are finalized in June 20x2 to record the curtailment gain or loss, nor should the amount of curtailment gain or loss recognized in 20x1 be adjusted when the final elections are known in 20X2. The rationale for this approach is that the effects of the curtailment should be recognized when the amendment is effective. Even though the exact measurement of the ultimate effect will depend on the employee elections, the need to estimate those elections is no different than many of the actuarial assumptions developed during the normal measurement of the plan.

Example PEB 4-2 illustrates the accounting for a net curtailment gain in one plan and a net curtailment loss in another plan as a result of the same restructuring event.

EXAMPLE PEB 4-2

Restructuring event causes a net curtailment gain in one plan and a net curtailment loss in another plan

On December 31, 20X1, PEB Corporation decided to restructure its operations, resulting in the layoff of 10,000 employees. The employees that will be affected by the layoff are covered by two separate pension plans, one for hourly workers (Hourly Plan) and one for salaried workers (Salaried Plan). At the time PEB Corporation determined that the layoff was probable, management evaluated the two plans for curtailment. Upon doing so, they determined that the curtailment in the Hourly Plan would result in a net loss, while the curtailment in the Salaried Plan would result in a net gain. The employees will be terminated during 20X2.

Can PEB Corporation record the effects of both plan curtailments in 20X1?

Analysis

No.

ASC 715-30-35-69 requires pension accounting to be applied at the individual plan level (i.e., the determination of whether a curtailment has occurred is a plan-by-plan assessment). Thus, the curtailment of the Hourly Plan is a separate accounting event from the curtailment of the Salaried Plan. In addition,

ASC 715-30-35-94 indicates that a net curtailment loss "shall be recognized in earnings when it is probable that a curtailment will occur and the effects described are reasonably estimable." It further states that a net curtailment gain "shall be recognized in earnings when the related employees terminate.” Because the net result of the curtailment of the Hourly Plan is a loss, PEB Corporation should record the loss when it is probable and reasonably estimable (i.e., on December 31, 20X1). On the other hand, because the net result of the curtailment of the Salaried Plan is a gain, PEB Corporation should record the gain when the salaried employees are terminated in 20X2.

Example PEB 4-3 illustrates the recognition of a curtailment from a phased restructuring event.

EXAMPLE PEB 4-3

Recognition of a curtailment from a phased restructuring event

On January 1, 20X1, PEB Corporation decided to restructure its operations, resulting in a layoff of employees. The layoffs will occur in phases as each phase is determined by management, but are clearly part of a single restructuring plan. The employees that will be affected by the layoff are covered by a single pension plan. The plan of restructuring represents a curtailment event because it will significantly reduce the expected years of future service of present employees in the pension plan.

During the first quarter of 20X1, PEB Corporation determined that the layoffs as a result of Phase 1 were probable and the number and demographic characteristics of the affected employees were estimable. In turn, management determined that Phase 1 would result in a curtailment loss of $100 million, which was recorded in the first quarter of 20X1. In the third quarter of 20X1, PEB Corporation finalized Phase 2 of the employee terminations, the amount and nature of which were not identified (i.e., not reasonably estimable) prior to that point. The employees from Phase 2 will not be terminated until 20X2. Management determined that the Phase 2 layoffs would result in a curtailment gain of $60 million.

When should PEB Corporation account for the curtailment gain resulting from Phase 2?

Analysis

The curtailment gain from Phase 2 should be recorded in the third quarter when it becomes probable and estimable, as it reduces the overall curtailment loss on the single restructuring action. Normally, a curtailment gain would not be recorded until the related employees are actually terminated. However, in this example, the employees affected by Phase 1 and Phase 2 participate in the same pension plan and the curtailment arises as a result of a single overall restructuring plan.

ASC 715-30-55-172 indicates that when there are individually insignificant reductions of expected future years of service of employees covered by a pension plan that are caused by one event (such as related to a single plan of reorganization), and those reductions accumulate to a significant reduction, the fact that the reductions occur over a period of time does not affect the determination that an event giving rise to a curtailment has occurred. This literature suggests that if there are multiple phases of employee reductions that relate to a single event, the phases should be aggregated to determine whether a curtailment has occurred.

Had PEB Corporation been able to determine that Phase 2 was probable and been able to estimate its impact when PEB Corporation recorded the initial curtailment loss from Phase 1, the amount PEB Corporation would have recorded would have been the combined curtailment loss of $40 million.

Example PEB 4-4 addresses the timing of recognition of curtailment gains for phased terminations.

EXAMPLE PEB 4-4

Timing of recognition of curtailment gains for phased terminations

On December 15, 20X1, PEB Corporation, a calendar year end reporting entity with an OPEB plan, announced a plant closing. As a result, 200 employees will be terminated on or before January 31, 20X2. An additional 200 will be terminated on or before April 15, 20X2 and an additional 200 will be terminated on or before August 1, 20X2. In accordance with

ASC 715-30-55-172, PEB Corporation aggregates the terminations that will occur in January, April, and August to determine whether the plant closing results in a curtailment (i.e., whether the combined effect of all three tranches of terminations as part of a single plant closing constitute a significant reduction in future years of service). Based on PEB Corporation’s policy for determining significance, it has concluded that the terminations expected to occur as a result of the plant closing will result in a curtailment and that the curtailment will result in a gain. However, the termination of the first 200 employees on January 31 will not constitute a significant reduction; a significant reduction will occur only when the termination of an additional 200 employees occurs on April 15 for an aggregate termination of 400 employees at that date.

When should PEB Corporation measure and record the curtailment gain?

Analysis

In accordance with

ASC 715-30-35-94, a curtailment gain should be recognized in earnings when the related employees terminate, not when the plant closing is announced. Since the employees will be terminated on three separate dates, PEB Corporation may recognize a portion of the gain in the first quarter (for January 31 terminations), in the second quarter (for April 15 terminations), and in the third quarter (for August 1 terminations). A full remeasurement of the obligation and plan assets should be performed immediately prior to determining the gain to be recognized in each quarter.

Alternatively, PEB Corporation can choose to recognize the gain when the number of employees that have been terminated constitutes a significant reduction of future years of expected service and therefore meets the definition of a curtailment. In that case, PEB Corporation would recognize no effect of the curtailment in the first quarter. Then, in the second quarter, the portion of the gain for the 400 employees that are terminated in both the January and April timeframes would be recognized. In the third quarter, the gain associated with the August terminations would be recognized. This treatment is consistent with the guidance in

ASC 715-30-55-167 and

ASC 715-30-55-168 in which a settlement gain or loss is recognized once the individual settlement amounts are expected to exceed the threshold amount of service and interest and cost for the year. A full remeasurement of the obligation and plan assets should be performed immediately prior to determining the gain to be recognized in the second and third quarters.

Once either method is selected, it would constitute an accounting policy that would need to be applied to similar events in the future.

Importantly, if the effect on the plan from the employee terminations was a curtailment loss, PEB Corporation would have no choice other than to recognize the full amount of the loss in December 20X1, when the curtailment event would have been deemed probable and estimable.

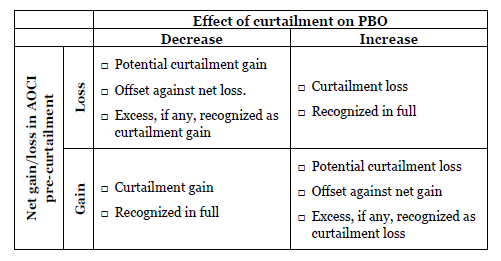

View image

View image

View image

View image