ASC 410-30-25-7 indicates that given their nature, it may be difficult to estimate the total cost of environmental remediation liabilities. A variety of factors may raise uncertainty as to the total cost of remediation, especially early in the remediation process. Given these challenges, a reporting entity’s initial estimates may later require adjustment due to, but not limited to, the factors, which are outlined in

ASC 410-30-25-7.

Excerpt from ASC 410-30-25-7

The following are some of the factors that are integral to developing cost estimates:

a. The extent and types of hazardous substances at a site

b. The range of technologies that can be used for remediation

c. Evolving standards of what constitutes acceptable remediation

d. The number and financial condition of other potentially responsible parties and the extent of their responsibility for the remediation (that is, the extent and types of hazardous substances they contributed to the site).

Despite these complicating factors, a reporting entity should attempt to reasonably estimate the cost of environmental remediation when it has determined that an obligation is probable. As the base of knowledge throughout the business community continues to grow concerning environmental remediation costs, it is increasingly difficult for a reporting entity to support delayed recognition of an environmental remediation liability because of an inability to reasonably estimate it.

Given the nature of environmental obligations, a “point” estimate of the total cost for remediation is often difficult to determine.

ASC 410-30-25-9 and

ASC 410-30-25-10 include guidance for when there is a range of estimates.

ASC 410-30-25-9

An estimate of the range of an environmental liability typically is derived by combining estimates of various components of the liability (such as the costs of performing particular tasks, or amounts allocable to other potentially responsible parties but that will not be paid by those other potentially responsible parties), which are themselves likely to be ranges. For some of those component ranges, there may be amounts that appear to be better estimates than any other amount within the range; for other component ranges, there may be no such best estimates. Accordingly, the overall liability that is recorded may be based on amounts representing the lower end of a range of costs for some components of the liability and best estimates within ranges of costs of other components of the liability.

ASC 410-30-25-10

In the early stages of the remediation process, particular components of the overall liability may not be reasonably estimable. This fact should not preclude the recognition of a liability. Rather, the components of the liability that can be reasonably estimated should be viewed as a surrogate for the minimum in the range of the overall liability.

An environmental remediation liability is typically comprised of several components. For some of these components, the facts may indicate a best estimate within a range. For other components, there may be no best estimate within the range. For still others, there may be no reasonable estimate of the range. As such, the overall liability (i.e., the sum of all of the components) may be based on a combination of amounts representing the low ends for components for which there is a reasonable estimate of a range and, for other components, the best estimate within ranges. Even when the range is very wide, at a minimum, the lower end of the range should be accrued.

This requirement is akin to the recognition criteria of

ASC 450-20-30-1, which requires accrual of “the amount that appears to be a better estimate than any other estimate within the range, or accrual of the minimum amount in the range if no amount within the range is a better estimate than any other amount.”

It is the reporting entity's responsibility to undertake reasonable measures to comply with the requirements of

ASC 450 and

ASC 410-30. It is reasonable that the amount of a probable environmental liability would not be determinable immediately upon discovery of the situation and that a reasonable period of time would be required to gather sufficient data to estimate the amount. However, the credibility of "inestimability" as justification for not recording a probable environmental liability diminishes with the passage of time, particularly when applying the components concept prescribed by

ASC 410-30-25-9. Generally, some amount would be accrued when involvement in remediating a site is probable.

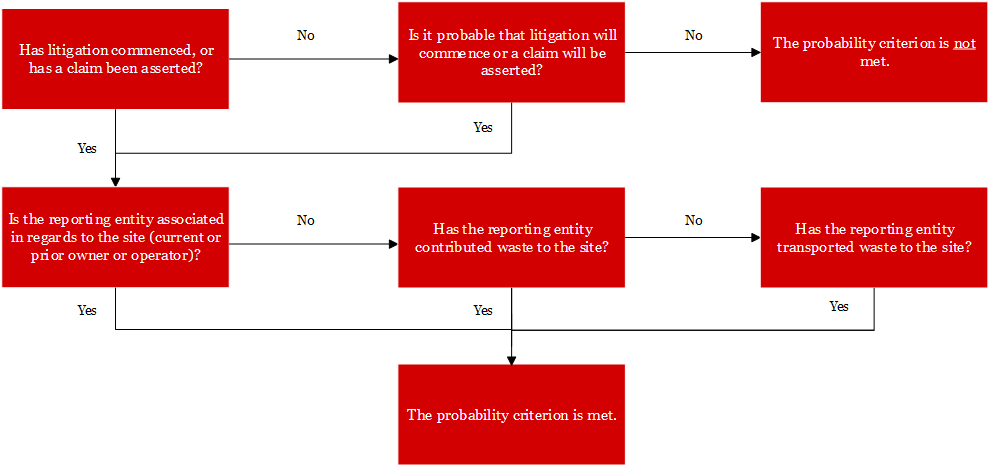

Question PPE 9-2 outlines considerations for a reporting entity upon notification by a governmental agency that it is one of multiple potentially responsible parties (PRPs) in regard to an environmental waste site.

Question PPE 9-2

A reporting entity has been notified by a governmental agency that it one of several PRPs with regard to an environmental waste site. The reporting entity believes it is not the biggest offender in terms of volume or severity of waste. No site study has been prepared. How should the reporting entity determine the possible effects on its financial statements?

PwC response

Once the reporting entity has confirmed it is associated with the site,

ASC 410-30 concludes that the "probable" criterion has been met. The reporting entity should discuss the site with the governmental agency involved to ascertain the total extent of waste, particularly given joint and several liability statutes, and to inquire as to other PRPs involved. The reporting entity should review site operating records or disposal records to determine what materials the reporting entity was likely to have disposed of and in what quantities. The reporting entity may have available past history from similar sites upon which to base estimates of cost. The reporting entity could also engage an environmental consulting firm to perform a preliminary review of the site. At a minimum, accrual of the estimated cost to perform the remediation study is required.

If the reporting entity is one of many PRPs, but not the "lead" PRP (or in the group of "primary" PRPs), the reporting entity may be subject to the timetable established by the regulatory agency and lead PRP. In such instances, information concerning work related to determining the extent and type of remedial actions, the remedial investigation and feasibility study, and remediation estimates may be available and such estimates would be a starting point for a reporting entity to make an estimate of its share.