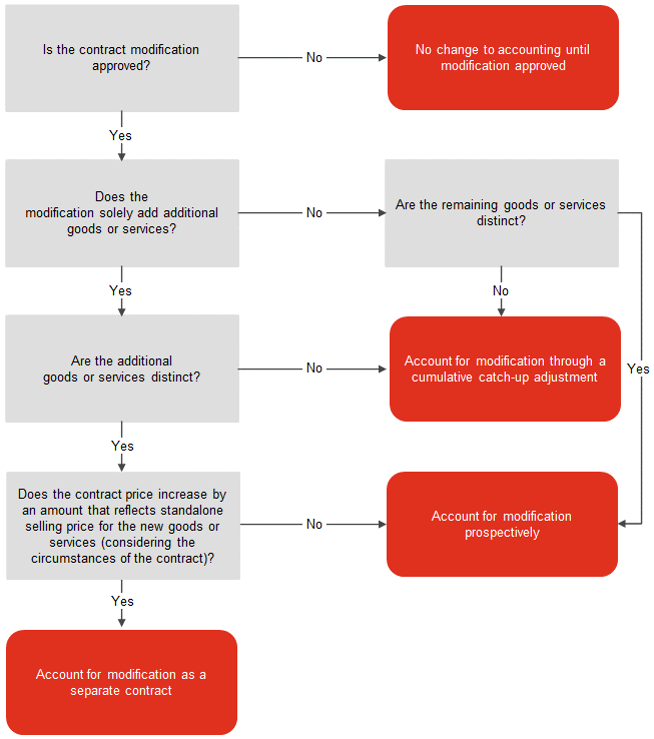

A reporting entity should account for a modification prospectively if the modification is not a separate contract (as described in

RR 2.9.2), but the remaining goods or services are distinct from the goods or services transferred before the modification. This type of contract modification is effectively treated as the termination of the original contract and the creation of a new contract. The contract consideration is allocated to the remaining performance obligations after the modification, including any unsatisfied performance obligations from the original contract. The amount of allocated consideration is the sum of any unrecognized consideration initially included in the transaction price of the contract before the modification and any additional consideration promised as part of the modification. Allocation to the remaining performance obligations should be based on current standalone selling prices since the modification is treated as the creation of a new contract.

A reporting entity will also account for a contract modification prospectively if the contract contains a single performance obligation that comprises a series of distinct goods or services, such as a monthly cleaning service (refer to

RR 3.3.2). In other words, the modification will only affect the accounting for the remaining distinct goods and services to be provided in the future, even if the series of distinct goods or services is accounted for as a single performance obligation.

Example RR 2-17 and Example RR 2-18 illustrate contract modifications accounted for prospectively. This concept is also illustrated in Example 7 of the revenue standard (

ASC 606-10-55-125 through

ASC 606-10-55-128).

EXAMPLE RR 2-17

Contract modifications – series of distinct services

ServeCo enters into a three-year noncancellable service contract with Customer for $450,000 ($150,000 per year). The standalone selling price for one year of service at inception of the contract is $150,000 per year. ServeCo accounts for the contract as a series of distinct services (refer to

RR 3.3.2).

At the end of the second year, the parties agree to modify the contract as follows: (1) the fee for the third year is reduced to $120,000; and (2) Customer agrees to extend the contract for another three years for $300,000 ($100,000 per year). The standalone selling price for one year of service at the time of modification is $120,000.

How should ServeCo account for the modification?

Analysis

The modification would be accounted for as if the existing arrangement was terminated and a new contract created (that is, on a prospective basis) because the remaining services to be provided are distinct. The modification should not be accounted for as a separate contract, even though the remaining services to be provided are distinct, because the price of the contract did not increase by an amount of consideration that reflects the standalone selling price of the additional services.

ServeCo should reallocate the remaining consideration to all of the remaining services to be provided (that is, the obligations remaining from the original contract and the new obligations). ServeCo will recognize a total of $420,000 ($120,000 + $300,000) over the remaining four-year service period (one year remaining under the original contract plus three additional years), or $105,000 per year.

EXAMPLE RR 2-18

Contract modifications — modification accounted for on a prospective basis

Supplier enters into a noncancellable contract with Retailer to supply 100,000 goods on an annual basis for $3 per unit for three years. At the beginning of the third year, Supplier and Retailer agree to renegotiate the contract because the market price for the goods has declined. Under the modified agreement, the parties agree to (1) extend the contract for an additional year (same fixed annual quantity) and (2) reduce the price per unit to $2 for the remaining 200,000 units to be delivered. Supplier also agrees as part of the modification to make a one-time payment of $10,000 to Retailer. There is no dispute between the parties regarding prior performance, and both parties have performed according to the terms of the contract.

Supplier concludes the remaining goods are distinct from those previously delivered and concludes the additional consideration does not reflect standalone selling price.

How should Supplier account for the modification?

Analysis

Supplier should account for the modification on a prospective basis. The transaction price of $390,000 ($2 per unit x 200,000 remaining goods less $10,000 payment to Retailer) should be allocated to the remaining performance obligations, resulting in revenue of $1.95 per unit ($390,000 / 200,000 goods). The $10,000 payment to Retailer is a reduction of the transaction price allocated to the remaining goods in this fact pattern because the payment was made in conjunction with the renegotiation of the contract and there is no indication that the payment relates to prior performance.

In contrast, if there was evidence of a dispute or failure to perform according to the contract terms related to the previously delivered goods, this might indicate that Supplier agreed to make a concession that reduces the transaction price for the previously delivered goods. In that case, the amount that represents a concession would be recorded immediately. Determining when a portion of a modification is in substance a price concession could require significant judgment. This concept is illustrated in Example 5, Case B of the revenue standard (

ASC 606-10-55-114 through

ASC 606-10-55-116).

Question RR 2-6

Should an existing contract asset be written off as a reduction of revenue when a modification is accounted for as the termination of the original contract and creation of a new contract?

PwC response

Generally, no. Although the original contract is considered “terminated,” modifications of this type should be accounted for on a prospective basis. That is, the contract asset would typically relate to a right to consideration for goods and services that have already been transferred. Management should consider, however, whether the facts and circumstances of the modification result in an impairment of the contract asset. Refer to US Revenue

TRG Memo No. 51 and the related meeting minutes in Revenue

TRG Memo No. 55 for further discussion of this topic.