A vendor providing a CCA to customers will need to assess whether the arrangement includes a license (i.e., whether the software is transferred to the customer) to determine which guidance to apply to the related software development costs. The guidance in

ASC 350-40-15-4A (see

SW 1.5) is used to make this assessment for both vendors and customers in a CCA.

- CCA is solely a service: As the software is solely used by the vendor to provide a service to customers, the related software development costs should be accounted for under the internal-use software guidance (see SW 3).

- CCA includes a software license: The software development costs incurred by the vendor for software being licensed to customers should be accounted for under the externally marketed software guidance (see SW 2).

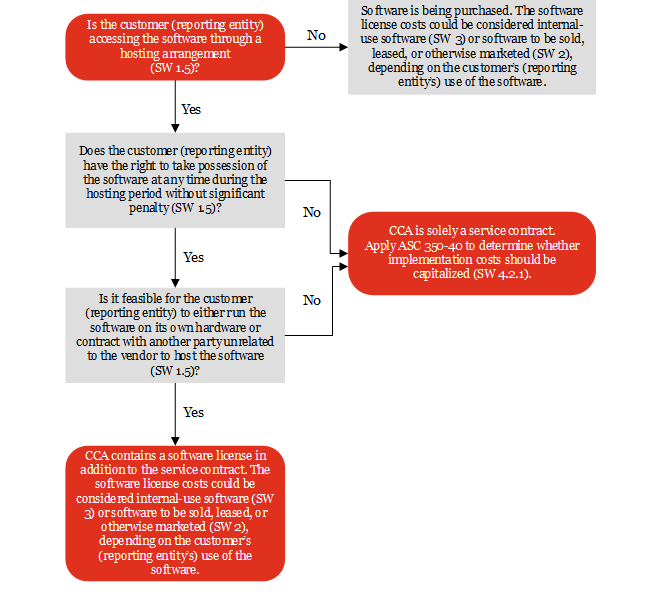

Refer to Figure SW 1-1 for a decision tree for determining the relevant guidance for costs incurred by vendors to obtain or develop software, including software a customer accesses through a hosting arrangement.

Question SW 1-2

Which guidance applies to software development costs related to software that a reporting entity uses to provide a service to some customers in a hosting arrangement, but licenses it to other customers (as on-premises software)?

PwC response

Generally, if a reporting entity has substantive sales of on-premises software, the guidance for externally marketed software in

ASC 985-20 should be applied to the related software development costs. This is the case even if the reporting entity is also using the same software to provide a service to customers in a hosting arrangement. If the reporting entity incurs costs that relate solely to the platform used for hosting the software or only the hosted version of the software (and not the licensed on-premises software), the guidance for internal-use software in

ASC 350-40 may apply to those costs. Assessing which costs, if any, are subject to the internal-use software guidance in this situation may require judgment.

Question SW 1-3What are the accounting implications if a reporting entity has capitalized costs under

ASC 350-40 related to software it uses to provide a service (as a SaaS arrangement), but subsequently agrees to license the same software to a customer that wants to host the software itself?

PwC response

If an entity decides to sell software that was capitalized under

ASC 350-40 based on an assumption that the software would be used only for internal use, the proceeds from the sale are applied against the carrying amount of that software in accordance with the guidance in

ASC 350-40-35-7. Refer to

SW 3.9 for further discussion of the accounting implications in these circumstances. The reporting entity should also consider whether future development costs (e.g., product enhancements or new software products) should be accounted for under

ASC 985-20. As discussed in

SW 1.4,

ASC 350‑40‑15‑2C indicates that a pattern of selling software to a third party that was originally developed to use internally creates a rebuttable presumption that any software developed by that reporting entity is intended for sale, lease, or other external marketing.

Question SW 1-4What are the accounting implications if a reporting entity has capitalized costs under

ASC 985-20 related to software that it both (a) licenses to customers (as on-premises software) and (b) uses to provide a service (a SaaS arrangement), but subsequently discontinues licensing the software to customers?

PwC response

Many reporting entities are transitioning from licensing on-premises software to providing SaaS offerings to customers. The accounting guidance does not specifically address the transition from externally marketed software to internal-use software. However, a reporting entity may conclude that it no longer intends to market software externally even though it has a history of licensing software to customers. As a result, development costs for new software products or enhancements to existing products (unless licensed for on-premises use by customers) may be in the scope of

ASC 350-40. This determination could require significant judgment. If the reporting entity is transitioning to SaaS offerings, but expects to continue to have substantive licenses of on-premises software,

ASC 985-20 should continue to be applied.

Question SW 1-5

Which guidance applies to development costs related to software that will be hosted by a third-party service provider (i.e., a party other than the reporting entity or customer) in arrangements with customers?

PwC response

It depends on whether the third party is hosting the software on behalf of the reporting entity (the vendor) or the customer. If the reporting entity contracts with a third party to host software developed by the reporting entity (to be accessed by customers), the accounting for the related software development costs is no different than the reporting entity hosting the software on its own servers. The reporting entity should apply the guidance in

ASC 350-40-15-4A (see

SW 1.5) to assess whether the arrangement with the customer includes a license, which will determine which software cost guidance applies (see Figure SW 1-1).

If the customer purchasing the software chooses to utilize a third-party hosting service instead of hosting the software on its own servers, the reporting entity could conclude it has transferred the software to the customer. Thus, the related development costs would be accounted for under

ASC 985-20.

Question SW 1-6

Which guidance applies to costs incurred by a reporting entity (a vendor) to implement a software product or a CCA for a specific customer?

PwC response

Costs incurred to implement a software product or CCA for a specific customer are generally costs to fulfill a revenue contract and would be subject to the guidance in

ASC 340-40,

Other Assets and Deferred Costs—

Contracts with Customers. In contrast, if the reporting entity incurs costs to make modifications to the software that benefit multiple customers, the reporting entity should consider the guidance in internal-use software or externally marketed software, as applicable.