Search within this section

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets

Favorited Content

Excerpt from ASC 860-50-25-1

An entity shall recognize a servicing asset or servicing liability each time it undertakes an obligation to service a financial asset by entering into a servicing contract in any of the following situations:

Excerpt from ASC 860-50-25-2

A servicer that transfers or securitizes financial assets in a transaction that does not meet the requirements for sale accounting and is accounted for as a secured borrowing with the underlying financial assets remaining on the transferor’s balance sheet shall not recognize a servicing asset or a servicing liability.

Excerpt from ASC 860-50-25-3

A servicer that recognizes a servicing asset or servicing liability shall account for the contract to service financial assets separately from those financial assets.

Excerpt from ASC 860-50-25-4

An entity that transfers its financial assets to an unconsolidated entity in a transfer that qualifies as a sale in which the transferor obtains the resulting securities and classifies them as debt securities held to maturity in accordance with Topic 320 may either separately recognize its servicing assets or servicing liabilities or report those servicing assets or servicing liabilities together with the asset being serviced.

Definitions from ASC Master Glossary

Benefits of Servicing: Revenues from contractually specified servicing fees, late charges, and other ancillary sources, including float.

Adequate Compensation: The amount of benefits of servicing that would fairly compensate a substitute servicer should one be required, which includes the profit that would be demanded in the marketplace. It is the amount demanded by the marketplace to perform the specific type of servicing. Adequate compensation is determined by the marketplace; it does not vary according to the specific servicing costs of the servicer.

Excerpt from ASC 860-50-35-1

An entity shall subsequently measure each class of servicing assets and servicing liabilities using either of the following methods:

Excerpt from ASC 860-50-35-1A

A servicing asset may become a servicing liability, or vice versa, if circumstances change.

Definition from ASC Master Glossary

Contractually Specified Servicing Fee: All amounts that, per contract, are due to the servicer in exchange for servicing the financial asset and would no longer be received by a servicer if the beneficial owners of the serviced assets (or their trustees or agents) were to exercise their actual or potential authority under the contract to shift the servicing to another servicer. Depending on the servicing contract, those fees may include some or all of the difference between the interest rate collectible on the financial asset being serviced and the rate to be paid to the beneficial owners of those financial assets.

Consideration |

Impact |

Current interest rates |

Lower interest rates provide borrowers incentive to refinance. |

Loan to value ratio |

Some homeowners may, despite low interest rates, be unable to refinance their loans because they have little or no equity in their homes due to declining property values. |

Regional demographics |

Certain areas of the country have historically experienced higher prepayment rates than others. This partly stems from local demographics. For instance, a particular area may be more transient than other parts of the country. |

Entity experience |

Actual experience of the entity compared to others in the same geographic and/or demographic area. |

Year |

Servicing asset carrying value |

Cumulative amortization percentage (A) = (D) / $290K |

Cumulative amortization expense (B) = (A) * $160K |

Current period amortization expense (C) = current year (B) – prior year (B) |

Net servicing income per year* |

Cumulative net servicing income* (D) |

Total estimated net servicing income* |

$160,000 |

— |

— |

— |

— |

— |

$290,000 |

|

1 |

147,200 |

8.00% |

$12,800 |

$12,800 |

$23,200 |

$23,200 |

|

2 |

134,800 |

15.75 |

25,200 |

12,400 |

22,475 |

45,675 |

|

3 |

122,800 |

23.25 |

37,200 |

12,000 |

21,750 |

67,425 |

|

4 |

111,200 |

30.50 |

48,800 |

11,600 |

21,025 |

88,450 |

|

5 |

100,000 |

37.50 |

60,000 |

11,200 |

20,300 |

108,750 |

View image

View image

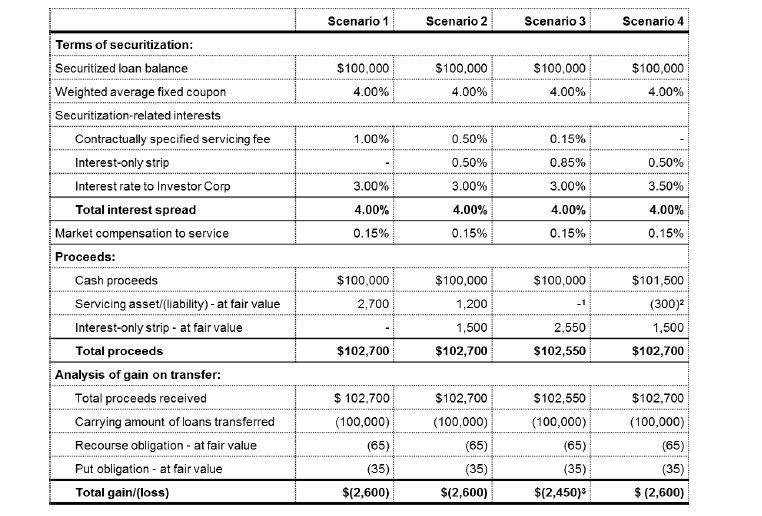

Dr. Cash

|

$100,000

|

|

Dr. Servicing asset

|

$2,700

|

|

Cr. Loans

|

$100,000

|

|

Cr. Recourse obligation

|

$65

|

|

Cr. Put option

|

$35

|

|

Cr. Gain on sale of loans

|

$2,600

|

Dr. Cash

|

$100,000

|

|

Dr. Servicing asset

|

$1,200

|

|

Dr. Interest only strip

|

$1,500

|

|

Cr. Loans

|

$100,000

|

|

Cr. Recourse obligation

|

$65

|

|

Cr. Put option

|

$35

|

|

Cr. Gain on sale of loans

|

$2,600

|

Dr. Cash

|

$100,000

|

|

Dr. Interest only strip

|

$2,550

|

|

Cr. Loans

|

$100,000

|

|

Cr. Recourse obligation

|

$65

|

|

Cr. Put option

|

$35

|

|

Cr. Gain on sale of loans

|

$2,450

|

Dr. Cash

|

$101,500

|

|

Dr. Interest only strip

|

$1,500

|

|

Cr. Loans

|

$100,000

|

|

Cr. Recourse obligation

|

$65

|

|

Cr. Put option

|

$35

|

|

Cr. Servicing liability

|

$300

|

|

Cr. Gain on sale of loans

|

$2,600

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets