Search within this section

Select a section below and enter your search term, or to search all click Utilities and power companies

Favorited Content

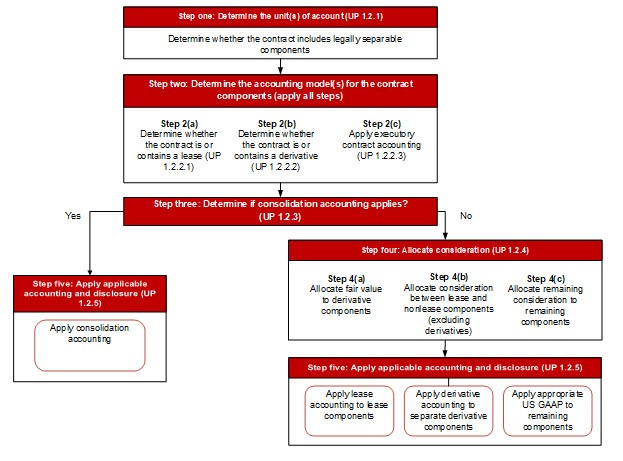

Excerpt from ASC 840-10-15-16

… separate contracts with the same entity or [its] related parties that are entered into at or near the same time . . . [should] be evaluated as a single arrangement in considering whether there are one or more units of accounting, including a lease.

Excerpt from ASC 815-10-25-6

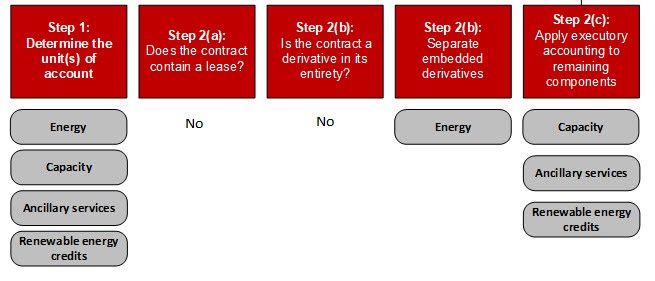

Component |

Allocation considerations |

4(a) Allocate fair value to derivative components

|

|

4(b) Allocate consideration between lease and nonlease components (excluding derivatives)

|

After the adoption of ASC 842:

Prior to the adoption of ASC 842:

|

4(c) Allocate to remaining components

|

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Utilities and power companies