Search within this section

Select a section below and enter your search term, or to search all click Utilities and power companies

Favorited Content

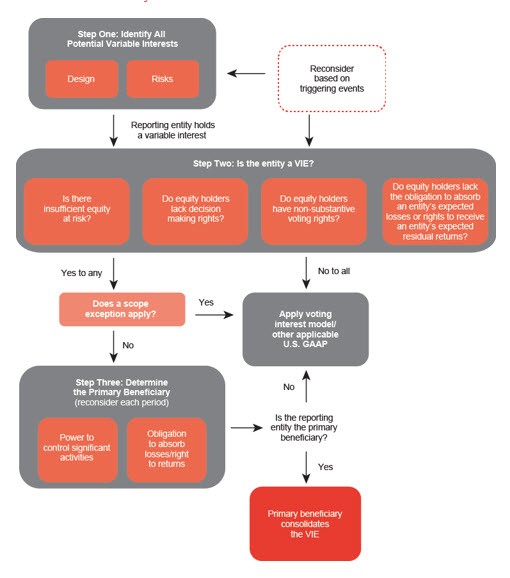

Focus on risks to identify variable interests

The first step in the VIE analysis is the identification of variable interests in accordance with the by-design model, which focuses on what risks the VIE is designed to create and pass along to its interest holders. Interests that absorb risk are variable interests, while those that create risk are not. See UP 10.2.

|

Consider whether an entity is a VIE

The evaluation of whether an entity is a VIE is based on specified criteria. If any of the criteria are met, the entity is a VIE. See UP 10.3.

|

Focus on powers to identify the primary beneficiary

The primary beneficiary is the variable interest holder with the power to direct the activities that most significantly impact the economic performance of the VIE. The primary beneficiary must also have the right to absorb losses and receive benefits that could potentially be significant to the VIE. Only one party can meet both of these criteria. See UP 10.4.

|

Determine the primary beneficiary based on current powers held

The determination of which activities will most significantly impact a VIE’s economic performance should consider all activities over the life cycle of the entity. However, the determination of which party has the power to direct these activities is generally made based on powers currently held by variable interest holders. Terms that may change the conclusion in the future should be disclosed. See UP 10.4.1.1.

|

Consider whether there is no primary beneficiary

There may be circumstances where no party consolidates, such as when the most significant powers are held by a party that does not have a variable interest or when power is shared. See UP 10.4.1.4.

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Utilities and power companies