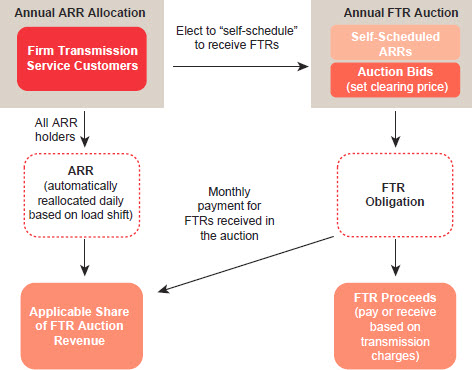

In determining the initial accounting for ARRs, a reporting entity should first consider the accounting for the ARR itself and then consider the accounting for the receipt of the ARR proceeds. As summarized in Figure 4-8, during the period after the ARR allocation and before the FTR Auction, we believe that an ARR generally meets the definition of a derivative.

Figure 4-8

Does an ARR meet the definition of a derivative?

|

Notional amount and underlying

|

|

• Notional (quantity of megawatts) and underlying (settlement is based on locational price differences between the Source and the Sink) are specified.

• If load shifts are significant, the reporting entity may initially conclude that a notional amount cannot be determined.

|

No initial net investment

|

|

• No initial net investment is required.

|

|

|

• Contractual ARRs are settled in cash; therefore, ARRs meet the net settlement criterion in ASC 815-10-15-83(c)(1). |

The ARR specifies a notional amount (a specific megawatt amount) and is settled based on locational price differences. The ARR settlement amount is determined based on the auction price and the notional amount of the ARR. The settlement proceeds are received in cash. Therefore, we generally conclude that the ARR meets the definition of a derivative. See further discussion in the responses to the following questions.

Question 4-1

Is there an acceptable alternative view that an ARR is not a derivative?

PwC response

Some believe that ARRs do not meet the definition of a derivative based on the conclusion that an ARR does not have an underlying. The price of an ARR is determined through the auction process, with market participants determining the value by bidding on various paths. As such, the settlement amount is not based on the interaction between the underlying and the notional. Thus, supporters of this view believe that this criterion is not met. Instead, they believe ARRs represent a receivable at the point of initial allocation.

We believe that ARRs should be accounted for as derivatives. However, from a practical perspective, the ARRs are allocated in May and the annual FTR Auctions are completed (and the ARR value is established) before the end of June. As a result, by the end of the second quarter (for calendar year-end companies), the ARR value is fixed and the ARR asset represents a receivable for the proceeds to be received on a monthly basis from the annual FTR Auction. Therefore, for most reporting entities, the question of whether an ARR is a derivative is applicable only for internal reporting purposes. By June 30 of each year, the value of an ARR is established and should be accounted for as a receivable. See

UP 4.4.2.2 for discussion of the subsequent accounting.

Question 4-2

Does an ARR qualify for the scope exception available for certain contracts that are not traded on an exchange?

PwC response

No.

ASC 815-10-15-59 provides guidance on certain contracts that are not traded on an exchange as follows:

Excerpt from ASC 815-10-15-59

Contracts that are not exchange-traded are not subject to the requirements of this Subtopic if the underlying on which the settlement is based is any one of the following: . . . (b) The price or value of a nonfinancial asset of one of the parties to the contract provided that the asset is not readily convertible to cash. This scope exception applies only if both of the following are true:

1. The nonfinancial assets are unique.

2. The nonfinancial asset related to the underlying is owned by the party that would not benefit under the contract from an increase in the price or value of the nonfinancial asset.

In accordance with this exception, a contract is not a derivative if it is based on the fair value of a nonfinancial asset of one of the parties to the contract. In certain cases, the ARR holder may have contractual transmission service on a line where it receives ARRs. The value of the ARR is based on the difference in price between the Source and the Sink as determined in the FTR Auction. Therefore, a question arises as to whether the settlement of the ARR is based on the value of a nonfinancial asset of one of the parties to the contract (i.e., the value of the underlying transmission).

However, the transmission revenue (to be received by the transmission holder) and the congestion revenue (to be received by the holder of the FTR) represent two separate payment streams. The value of the transmission contract is the tariff value of the transmission and does not incorporate the separate congestion cash flows. The ARR holder is generally the Load Serving Entity and will receive proceeds from the ARR that are based on the expected value of congestion costs (bid amounts for the FTRs).

As such, we do not believe that the value of the ARR is linked to the value of transmission contracts or underlying transmission owned by the ARR holder. Therefore, the scope exception is not applicable.

Question 4-3

Do ARR reallocations (load shift) change the conclusion that an ARR is a derivative?

PwC response

It depends. ARR holders are entitled to self-schedule FTRs equal to the allocated quantity of ARRs in the first round of the annual FTR auction. The notional amount for this right is fixed in the initially allocated ARR. However, the notional amount of the ARR may subsequently change prior to receipt of the cash as a result of load shifts.

ASC 815-10-55-5 through 55-7 provides relevant guidance in addressing notional amounts that may change over the life of a contract in the context of requirements contracts. Although ARRs are not requirements contracts, the overall guidance is helpful in evaluating the impact of potential notional changes.

Excerpt from ASC 815-10-55-7(a)

The determination of a requirements contract’s notional amount must be performed over the life of the contract and could result in the fluctuation of the notional amount if, for instance, the default provisions reference a rolling cumulative average of historical usage. If the notional amount is not determinable, making the quantification of such an amount highly subjective and relatively unreliable . . . such contracts are considered not to contain a notional amount as that term is used in this Subtopic.

In accordance with this guidance, a potential future change in notional amount does not impact the conclusion that the contract has a notional. However, there would be no notional if the determination of the amount is highly subjective and unreliable.

In evaluating an ARR, the notional amount of the contract may change any time from the point it is initially allocated until the reporting entity receives the final cash proceeds. If load shift is minimal, the determination of the notional amount is reliable and, as a result, the contract has a notional. However, if the load shift is significant, the initial determination of the quantity would be unreliable and there would be no notional amount. Reporting entities should evaluate this consideration and make a determination based on their historical experience and future load expectations.

Question 4-4

Does determination of the ARR value based on the results of the auction change the conclusion that the ARR has an underlying and a notional amount?

PwC response

No. The ultimate value of the ARR is determined based on the difference between the locational marginal price at the ARR Sink and the ARR Source as determined in each round of the annual FTR Auction. Although the value is developed through an auction rather than through another mechanism, we believe this represents an interaction between an underlying and a notional amount.

The ARR settlement amount is determined based on the interaction between the prices (as determined through the auction) and the notional amount of the ARR. The incorporation of the auction results does not change the fact that the amount of the payout is determined by the terms of the contract and the interaction of the underlying and notional amount. Therefore, the auction does not impact the conclusion that the contract has an underlying and a notional amount.

Question 4-5

Is an ARR a derivative even though the settlement proceeds may change?

PwC response

Yes. There may be some adjustments to and differences in the actual proceeds due to the PJM allocation process. This may cause some to question whether the settlement truly reflects the interaction between an underlying and a notional amount. However, these adjustments are expected to primarily relate to credit or other shortfalls that occur in the payment process. Any contract may not be fully paid due to issues in settlement. Therefore, the potential settlement adjustments do not impact the conclusion that the contract has an underlying and notional amount.

Question 4-6

Is an ARR a derivative even though the FTR Auction proceeds are received over a 12- month period, instead of immediately?

PwC response

Yes. The value of an ARR is determined through the annual FTR auctions and the proceeds are distributed to the ARR holders over the Planning Period (the following 12 months). Whether this constitutes net settlement in accordance with

ASC 815-10-15-83(c)(1) should be determined by reference to the guidance in

ASC 815-10-15-104 through 15-106, which address settlement through a structured payment.

Excerpt from ASC 815-10-15-104

A contract that provides for such a structured payout of the gain (or loss) resulting from that contract meets the characteristic of net settlement in paragraphs 815-10-15-100 through 15-109 if the fair value of the cash flows to be received (or paid) by the holder under the structured payout are approximately equal to the amount that would have been received (or paid) if the contract had provided for an immediate payout related to settlement of the gain (or loss) under the contract.

In this case, the payments are received over 12 months and there is no interest component. Therefore, the holder of the ARR does not receive the benefit of reinvestment of the proceeds. However, the bidder is also paying for the FTR over a 12-month period; therefore, the bid price presumably incorporates a time-value element.

Furthermore, given the relatively short duration of the payout (less than one year), we conclude that any time value of money would have an inconsequential impact on the fair value of the cash flows to be received over the duration of the payout as compared with those that would be received upon immediate payment. As such, the contract meets the net settlement criterion.