Search within this section

Select a section below and enter your search term, or to search all click Utilities and power companies

Favorited Content

Guidance |

Evaluation |

Comments |

|---|---|---|

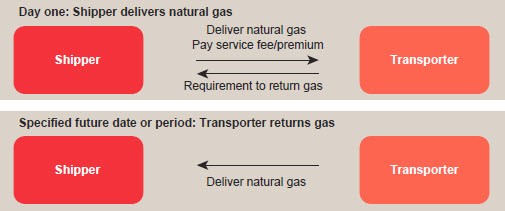

Notional amount and underlying

|

Met

|

|

No initial net investment

|

Not met

|

|

Net settlement

|

Met

|

|

Excerpt from ASC 815-10-15-95

Guidance |

Evaluation |

Comments |

|---|---|---|

Economic characteristics of the embedded are not clearly and closely related to the host

|

Met

|

|

Hybrid instrument is not remeasured at fair value under otherwise applicable U.S. GAAP

|

Met

|

|

A separate instrument with the same terms as the embedded derivative would be a derivative instrument subject to ASC 815

|

Met

|

|

Date |

Spot |

Forward |

|---|---|---|

May 1, 20X1

|

$4.00

|

$5.00

|

June 30, 20X1

|

3.00

|

4.50

|

September 30, 20X1

|

3.50

|

5.50

|

December 1, 20X1

|

6.00

|

—

|

Date |

Journal entries |

Cash |

Receivable |

Fuel inventory |

Derivative |

Income statement |

|---|---|---|---|---|---|---|

05/01

|

Initial purchase of natural gas (10,000 × $4.00)

|

($40)

|

$40

|

|||

05/01

|

Delivery of natural gas

|

$40

|

(40)

|

|||

05/01

|

Virtual storage fee paid

(see note 1)

|

(10)

|

10

|

|||

06/30

|

Record change in value of derivative (10,000 × ($5.00 – 4.50))

(see note 2)

|

($5)

|

$5

|

|||

06/30

|

Amortize virtual storage fee

Accrete receivable

(see note 3)

|

(3)

3

|

3

(3)

|

|||

09/30

|

Record change in value of derivative (10,000 × ($4.50 – 5.50))

|

10

|

(10)

|

|||

09/30

|

Amortize virtual storage fee

Accrete receivable

(see note 3)

|

(4)

4

|

4

(4)

|

|||

12/01

|

Record change in value of derivative (10,000 × ($5.50 – $6.00))

|

5

|

(5)

|

|||

12/01

|

Amortize virtual storage fee

Accrete receivable

(see note 3)

|

(3)

3

|

3

(3)

|

|||

12/01

|

Record receipt of natural gas from GGC and effectively “settle” embedded derivative

|

(50)

|

60

|

(10)

|

||

TOTAL

|

($50)

|

$ —

|

$60

|

$ —

|

($10)

|

Date |

Spot |

Forward |

|---|---|---|

May 1, 20X1

|

$4.00

|

$5.00

|

June 30, 20X1

|

3.00

|

4.50

|

September 30, 20X1

|

3.50

|

5.50

|

December 1, 20X1

|

6.00

|

—

|

Date |

Journal entries |

Cash |

Fuel inventory |

Fuel Liability |

Contract Liability |

Derivative |

Income statement |

|---|---|---|---|---|---|---|---|

05/01

|

Initial receipt of natural

gas (10,000 × $4.00) (see note 1) |

$40

|

($40)

|

||||

05/01

|

Sell natural gas inventory received

|

$40

|

(40)

|

$0

|

|||

05/01

|

Virtual storage fee

received (see note 1) |

10

|

(10)

|

||||

06/30

|

Record change in value of

derivative (10,000 × ($4.50 – 5.00)) (see note 2) |

$5

|

(5)

|

||||

06/30

|

Recognize revenue

(storage fee) (see note 3) Accrete fuel liability

(see note 4)

|

(3)

|

3

|

(3)

3

|

|||

09/30

|

Record change in value of

derivative (10,000 × ($5.50 – $4.50)) |

(10)

|

10

|

||||

09/30

|

Recognize revenue (storage

fee) (see note 3) Accrete fuel liability

(see note 4)

|

(4)

|

4

|

(4)

4

|

|||

12/01

|

Record change in value of

derivative (10,000 × ($6.00 – 5.50)) |

(5)

|

5

|

||||

12/01

|

Recognize revenue (storage

fee) (see note 3) Accrete fuel liability

(see note 4)

|

(3)

|

3

|

(3)

3

|

|||

12/01

|

Purchase natural gas

from spot market |

(60)

|

60

|

||||

12/01

|

Record delivery of

natural gas to REG (10,000 × $6.00) and effective “settlement” of embedded derivative |

(60)

|

50

|

10

|

0

|

||

TOTAL

|

($10)

|

$ —

|

$ —

|

$ —

|

$ —

|

$10

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Utilities and power companies