Search within this section

Select a section below and enter your search term, or to search all click Utilities and power companies

Favorited Content

Excerpt from ASC 842-10-15-3

Excerpt from ASC 842-10-15-16

A capacity portion of an asset is an identified asset if it is physically distinct (for example, a floor of a building or a segment of a pipeline that connects a single customer to the larger pipeline). A capacity or other portion of an asset that is not physically distinct (for example, a capacity portion of a fiber optic cable) is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset.

Guidance |

Evaluation |

Comments |

|---|---|---|

Notional amount

and underlying |

Met

|

|

No initial net

investment |

Met

|

|

Net settlement

|

Generally not met

|

|

Net settlement. The contract can be settled net by any of the following means:

Date |

Spot |

Forward |

|---|---|---|

May 1, 20X1

|

$4.00

|

$5.00

|

June 1, 20X1

|

4.00

|

4.75

|

June 30, 20X1

|

3.00

|

4.50

|

September 30, 20X1

|

3.50

|

5.50

|

December 1, 20X1

|

6.00

|

—

|

Date |

Journal entries |

Cash |

Fuel inventory |

Fuel revenue |

Fuel expense |

|---|---|---|---|---|---|

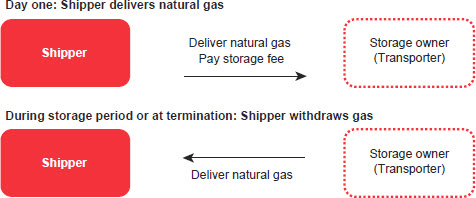

04/01

|

Record initial storage fee at contract inception

|

($2)

|

$2

|

||

05/01

|

Initial purchase of inventory (10,000 × $4.00/MMBtu)

|

($40)

|

$40

|

||

Monthly

|

To record storage fees

($2,000 per month x 7months) |

($14)

|

$14

|

||

12/01

|

To record the sale of natural gas inventory (10,000 × $6.00 spot)

|

$60

|

($40)

|

($60)

|

$40

|

Total

|

$4 |

$- |

($60) |

56 |

Date |

Spot |

Forward |

|---|---|---|

May 1, 20X1

|

$4.00

|

$5.00

|

June 1, 20X1

|

4.00

|

4.75

|

June 30, 20X1

|

3.00

|

4.50

|

September 30, 20X1

|

3.50

|

5.50

|

December 1, 20X1

|

6.00

|

—

|

Category |

Description |

Classification |

|---|---|---|

Working gas

|

|

Inventory

|

Base or cushion gas

|

|

Generally classified as part of property, plant, and equipment; represents a permanent investment necessary to use a storage facility and maintain reliability

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Utilities and power companies