September 2022

What you need to know

- Companies need to evaluate whether current economic conditions have affected their ability to continue as a going concern.

- Management should develop a plan to mitigate the impact of the conditions and events that put the company’s liquidity at risk.

- Depending on the circumstances, specific disclosures may be required in annual and interim financial statements, even if the company will remain liquid for more than a year

- Based on management’s disclosures and the auditor’s assessment, an explanatory paragraph may be added to the audit opinion.

A confluence of macroeconomic and geopolitical events — from inflation and rising interest rates to supply chain issues and Russia’s invasion of Ukraine — has resulted in substantial economic uncertainty. As a result, some companies are facing challenging operational and financial reporting considerations.

Because of this uncertainty, maintaining market confidence in a company’s financial statements and disclosures is more important than ever. For a user of the financial statements, one of the more important matters is having the information necessary to understand a company’s specific risks and uncertainties, liquidity, and ability to continue as a going concern.

Adequately identifying and responding to liquidity risks and other related impacts is foundational to a company’s ability to assess its business continuity. Given the significant judgments and estimates that may be required to properly evaluate the range of potential impacts of recent macroeconomic and geopolitical events, management must remain especially vigilant to ensure this area remains a high priority. This includes embracing an attitude of “don’t delay what you should do today.” Executive-level support and attention, coupled with diligent execution under a thoughtful framework, will help facilitate the effective performance of critical processes and controls to ensure that financial reporting and disclosure obligations are appropriately addressed.

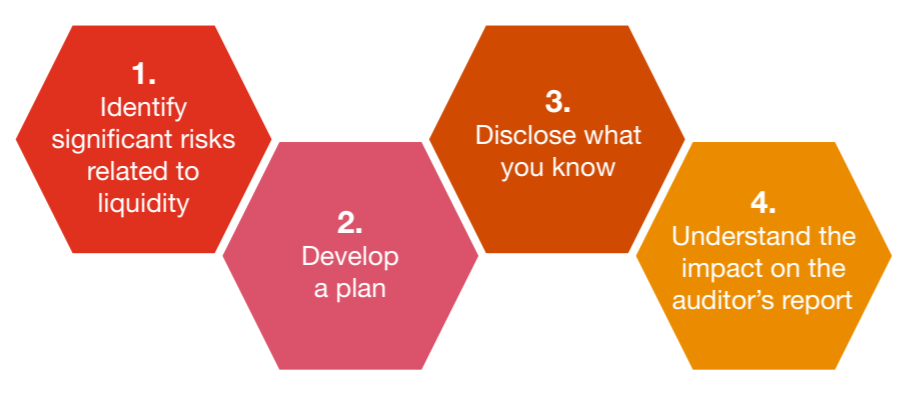

A management framework for evaluating going concern

1. Identify significant risks related to liquidity

At each annual and interim reporting period, US GAAP requires management to evaluate whether there are conditions or events that raise substantial doubt about the company’s ability to continue as a going concern within one year after the date that the financial statements are issued (or available to be issued when applicable). Management is required to consider conditions that are “known and reasonably knowable” at the date the financial statements are issued. In other words, the assessment should consider the most current information available before the financial statements are issued.

As defined in US GAAP, substantial doubt about a company’s ability to continue as a going concern exists when relevant conditions and events, considered in the aggregate, indicate that it is probable that the company will be unable to meet its obligations as they become due within one year after the date that the financial statements are issued.

Given the varying and discrete effects of these events on different companies and industries, management may be required to assess several risk indicators and multiple scenarios to adequately assess the range of potential impacts on their liquidity, ability to continue as a going concern, and adequacy of disclosures. Because of the continuing economic uncertainty, this assessment may need to evolve as circumstances change. The applicable processes and internal controls will need to address both interim and annual reporting periods—and current information available through the issuance date. Considerations will vary by company but may include:

- Changes in management’s forecasted operating results and/or cash flow projections due to:

- A reduction in revenues and impact on costs due to a decline in customer demand

- Disruption to the supply chain that could impact product costs, cause delays/inability to source product, or result in increased product liability risks or costs

- Impacts on costs due to increased inflation

- Provisions in critical customer or supply agreements that could trigger penalties or the loss of significant customers

- Increased interest expense due to higher debt levels or incremental borrowings at higher interest rates

- Longer collection cycles due to customer cash retention programs or inability of customers to pay

- Significant workforce disruptions and related implications

- Charges or costs resulting from accounting for impairments, including those arising from changes in long term growth or discount rate assumptions used in discounted cash flow modeling

- Charges or costs resulting from reserves, restructuring plans, or other impacts

- Changes in management’s assessment of its short- and medium-term liquidity or the company’s ability to access capital or obtain funding, considering:

- The ability to fund operations for at least twelve months from the date the financial statements are issued, considering current cash on hand, current and projected net cash flows from operations, maturities of debt and other commitments, and available sources of funding

- The likelihood of non-compliance with financial and/or nonfinancial debt covenants that could result in an acceleration of debt, increased borrowing costs, or restrictions on future borrowings

- Increasing interest rates on variable rate debt and the potential impact on liquidity or financial covenants

- Any reductions in asset-backed lending capacity due to reductions in the company’s borrowing base

- Potential or known credit downgrades that could result from reduced company profitability

- Tightening of credit within the financial markets, which could impact the company’s ability to refinance debt or otherwise result in reduced borrowing availability

- Stock market volatility, including overall declines in market capitalization, which could impact the ability or cost of issuing securities

- The inability to meet margin calls from financing counterparties, which could result in an event of default

- The impact of external conditions, such as measures taken by governments and banks to provide relief to affected entities or other matters, such as work stoppages or other labor difficulties, substantial dependence on the success of a particular project, uneconomic long-term commitments, or a need to significantly revise operations

Identifying and assessing these risks will require an informed and objective review of relevant underlying forecasts, with the appropriate involvement of operational and financial personnel who have a sufficient understanding of the company’s business and cash flows. They will need to be able to assess and evaluate the appropriateness of the inputs into the forecast and be able to objectively and effectively stress test key assumptions, including assessing whether changes to prior forecasts are necessary. Risk identification and assessment will also likely require involvement by knowledgeable treasury and finance specialists who can (1) validate the company’s ability to access debt or equity financing; (2) review key provisions in critical debt, vendor, or customer documents; and (3) accurately calculate current debt covenant compliance, and projected compliance based on updated forecasts, in accordance with the stated terms of the underlying agreements.

2. Develop a plan

When management identifies conditions or events that raise substantial doubt about a company’s ability to continue as a going concern, management should consider whether its plans that are intended to mitigate those relevant conditions or events will alleviate the substantial doubt. The mitigating effect of management’s plans should be considered only to the extent that (1) it is probable that the plans will be effectively implemented and, if so, (2) it is probable that the plans will mitigate the conditions or events that raise substantial doubt about the company’s ability to continue as a going concern within one year after the date that the financial statements are issued.

Senior management should develop plans to mitigate the impact of the conditions and events that put the company’s liquidity at risk. The actions in management’s plan should consider the current environment and may include plans for new borrowings or raising of additional capital, expected cost cutting, or liquidations of non-essential assets.

Management should understand its responsibilities for financial reporting and the related processes and internal controls—and the responsibilities of the auditor under the auditing standards as it relates to management’s plans. In general, auditors will focus on the underlying reasons for the conditions and events that caused substantial doubt about the company’s ability to continue as a going concern. They will then evaluate management’s plan with regard to whether it is probable that the plan (1) can be effectively implemented and (2) would mitigate the underlying conditions or events for a reasonable period of time. To do so, they objectively assess the probability of success of management’s plans (e.g., whether obtaining external financing is probable in light of the company’s current condition and the overall economic environment).

Auditor procedures, when applicable, may include assessing the reasonableness of management’s cash flow forecasts and underlying assumptions, reviewing debt agreements with a focus on financial and nonfinancial covenants, testing covenant calculations against the terms of the agreement (including forecasted covenant calculations), obtaining evidence of any amendments to financial covenants and management’s assessment of their ability to meet revised covenants, and reviewing other evidence provided by management to support their assessment that the plan is probable of being implemented and probable of mitigating the substantial doubt.

This is an area where timely and transparent discussions between management, those charged with governance, and the auditors can be especially valuable, both during annual audits and interim reviews.

3. Disclose what you know

If conditions or events raise substantial doubt about a company’s ability to continue as a going concern the company should disclose information that enables users of the financial statements to understand (a) the principal conditions or events that raised substantial doubt about the company’s ability to continue as a going concern (before consideration of management’s mitigation plans), (b) management’s evaluation of the significance of those conditions or events in relation to the company’s ability to meet its obligations, and (c) management’s plans that alleviated/are intended to mitigate the conditions or events that raise substantial doubt about the company’s ability to continue as a going concern. If substantial doubt is not alleviated after consideration of management’s plans, management must also include a statement that there is substantial doubt about the company’s ability to continue as a going concern within one year after the date that the financial statements are issued (or available to be issued).

Management is expected to determine whether disclosure of the impact of recent macroeconomic and geopolitical events is merited, depending on severity. Timely, company-specific disclosure is essential, even though it may be difficult to assess or predict the effects of current economic conditions with precision. In addition, companies should disclose in the footnotes any risks and uncertainties that could significantly affect financial statement amounts in the near term. Disclosures about the risks, including how the company is responding to them, are expected to be specific to a company’s situation as seen through the eyes of management. While judgment is required, there are resources companies can use when evaluating the need for certain disclosures (for example, the SEC’s “Dear CFO” letter on disclosures pertaining to the war in Ukraine and related supply chain issues).

Company-specific disclosure within the financial statements, risk factors, MD&A, and/or liquidity may include:

|

Detailed discussion of the company’s ability to generate sufficient cash to fund operations

|

|

Expected courses of action that bear on the company’s financial flexibility, including planned cost reductions

|

|

The impact on capital and financial resources, including overall liquidity position and outlook, such as:

- If a material liquidity deficiency was identified, what course of action the company has taken or proposes to take to address the deficiency

- Material uncertainties about the ongoing ability to meet debt covenants and the existence and nature of subjective acceleration clauses

- Whether the cost of, or access to, capital and funding sources, such as revolving credit facilities, has changed or is reasonably likely to change

- New borrowings or new capital

- Whether current or anticipated sources or uses of cash will be materially impacted

|

|

Impairments that have had or are reasonably likely to have a material impact on the company’s financial statements

|

It is important to note that management first determines the nature and extent of its disclosures. Auditors then have a professional responsibility to assess whether the annual and interim financial statement disclosures are adequate. Accordingly, this is another area where timely, ongoing, and transparent communications between management, those charged with governance, and the auditor is important.

4. Understand the impact on the auditor’s report

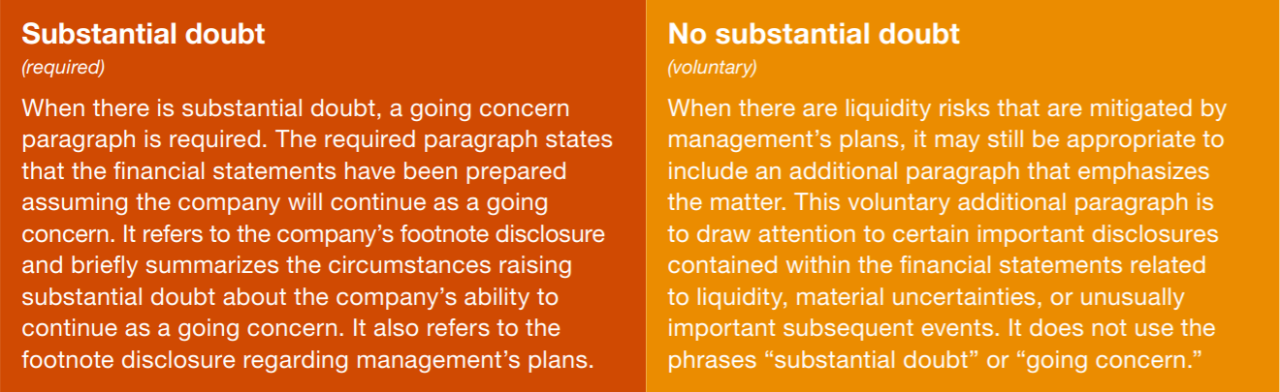

Similar to the impact on management’s disclosures, there may be implications on the auditor’s report. Specifically, there may be circumstances when the auditor concludes that an additional paragraph will be included in its report, such as:

- A required additional paragraph as a result of the conclusion that there is substantial doubt about the company’s ability to continue as a going concern

- A voluntary paragraph regarding liquidity/uncertainty despite concluding that there is not substantial doubt, or for unusually significant subsequent events

Simply put - an auditor may be required to include an additional paragraph, or they may voluntarily include one when they conclude it is important to highlight certain disclosures in the financial statements for the users’ attention.

As defined by the auditing standards, neither a required nor voluntary additional paragraph results in a qualified opinion. However, such paragraphs may be defined differently within a company’s debt agreements, and there could be an implication to debt covenants.

The differences between a required substantial doubt and a voluntary paragraph to highlight certain disclosures are as follows:

View image

View image

Keeping current and reissuance of audit reports

Management should also be aware of whether there are events and circumstances after the original issuance of the annual audited financial statements that could cause an auditor to reassess its originally issued report. In connection with capital raíses, debt offerings, and various other filing or regulatory requirements, the auditor may be asked to issue a consent, reissue its report, or otherwise be associated with a transaction or filing. In these situations, the auditor will likely be required to perform “keeping current procedures,” which might include performing an assessment of management’s ability to continue as a going concern both (1) one year from the date of the original issuance of the financial statements and (2) one year from the date of the keeping current procedures, as well as an evaluation of whether disclosures need to be updated.

If subsequent events have occurred, including those related to a company’s liquidity and ability to continue as a going concern, a reissuance of the financial statements and the auditor’s report may be required or otherwise deemed appropriate.

Accordingly, it is important for management to keep the auditor informed of any potential transactions that may require keeping current procedures to be performed.

Conclusion

Ongoing and timely communication among management, the audit committee (or those charged with governance), and the auditor should focus on the impact of current economic volatility on critical judgments, assumptions, and uncertainties, including those that may impact liquidity or going concern. This is especially important given the continually evolving landscape.

Ultimately, management needs to ensure that the financial statements and other elements of its financial reporting and public disclosures provide transparent information to stakeholders about the impact of this economic uncertainty on the company, any concerns about the company’s short- and long-term liquidity, and if so, how management intends to address them.

To have a deeper discussion, contact:

|