Search within this section

Select a section below and enter your search term, or to search all click In the loop

Favorited Content

- Carbonfund.org

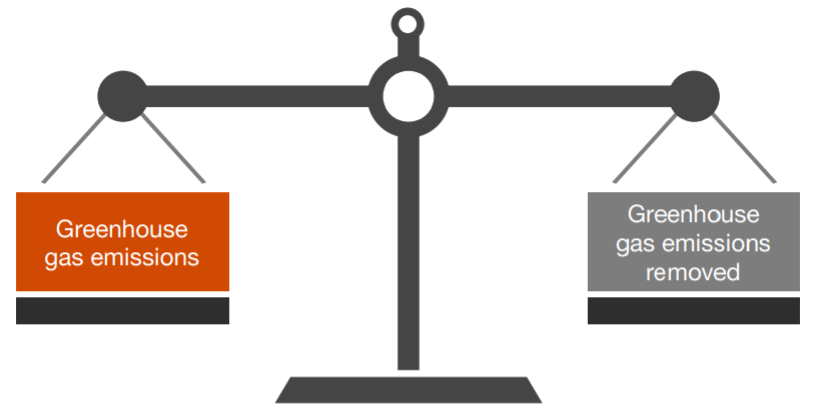

Net zero strategy

| Direct financial statement impacts

| |

|---|---|---|

| Technology

Technology that exists today will provide a partial solution to the net zero equation for some companies. Companies may undertake capital projects to improve the efficiency, cost, and effectiveness of their operations and reduce emissions. Examples include electrification (replacing technologies that run from fossil fuels such as natural gas with those that use electricity) or making changes to buildings and infrastructure (e.g., green certifying buildings or adding a solar roof to the building or parking lot).

Companies are also engaged in research to develop and improve technology to both reduce emissions or to absorb emissions that are not able to be reduced. For example, carbon capture and storage is a way of removing carbon emissions from the atmosphere by capturing the carbon dioxide produced by power generation or industrial activity, transporting it to a storage site, and then storing it deep underground.

|

|

| Renewable energy

Investment in renewable energy sources (e.g., wind, solar, hydro) is booming, and numerous non-traditional investors are entering this space. A renewable energy credit, or REC, is created for each megawatt hour of electricity that is generated from a renewable energy resource. A REC provides evidence that power has been generated by a qualifying renewable resource and is typically certified by a state or other agency, is separable from the underlying power, and may be purchased or sold.

While some companies may choose to directly invest in renewable projects and retain the RECs created by the project, others are obtaining RECs directly from power generators or moving to facilities with “greener” energy supplies. Typically, only the REC holder can “claim” the lower emissions resulting from using a renewable generating source, allowing them to offset power generated from other sources for purposes of any net zero commitments.

|

|

| Carbon offset programs

A carbon offset allows a company to invest in projects to offset or “reduce” the greenhouse gas emissions it produces. Companies typically purchase these to offset their emissions that cannot be eliminated. Carbon offsets are intended to represent an actual reduction of one ton of carbon dioxide or greenhouse gas (GHG). Carbon offsets can be generated from programs such as reforestation, farm management, methane abatement, and carbon capture.

There are numerous carbon offset programs and various forms of verification in the carbon offset market. Verification of offset programs is an evolving area and questions have been raised about whether the verification is truly substantive (e.g., are the offsets incremental to the emissions that would have been reduced absent the offset project). To avoid inadvertent greenwashing, companies that are considering investing in offset projects or purchasing carbon offsets should understand the underlying source of the carbon reduction, the likelihood of reduction absent the project (i.e., is it incremental to business as usual), and the criteria used to determine the amount of offsets generated. Also, it is important to ensure that the methods used to calculate the reduction in emissions are rigorous and accurate.

|

|

- Mark Carney, Special Envoy for Climate Action and Finance

Ask the National office

|

|---|

I have also heard about carbon credits and emissions allowances. What are those?

Carbon credits and emissions allowances are terms often used interchangeably. A carbon credit or emissions allowance gives an entity the legal right to emit one ton of carbon dioxide or GHG equivalent. They are generally used by companies such as power generators, utilities, and oil refineries that are subject to state regulations over their emissions. These companies are generally required to provide allowances equal to their emissions in a particular year. Companies subject to these requirements are typically allocated allowances based on certain targeted levels of emissions. If the company uses fewer emissions credits than it is allocated, it can trade, sell, or hold the excess credits. Alternatively, a company that emits carbon dioxide or GHG equivalents in excess of its cap would be required to purchase emissions credits from another company. Ultimately, the credits will be retired when used to meet a company’s compliance obligation.

How do these differ from carbon offsets?

While carbon offsets are intended to be actual reductions in carbon or GHG equivalents, carbon credits or emissions allowances represent the amount of emissions a company is allowed to produce (though there are some that use all of these terms interchangeably). Companies should look through the “form” of the program to understand its substance.

Do carbon credits or emissions allowances get considered in whether a company has met its net zero targets?

No. Because an emissions allowance or carbon credit does not represent an actual emissions reduction (i.e., a company has not taken steps to incrementally reduce the amount of emissions beyond what they are allowed to produce), it is not factored in a net zero commitment.

|

To have a deeper discussion, contact:

| ||

For more PwC accounting and reporting content, visit us at viewpoint.pwc.com.

| ||

Bio-energy with carbon capture and storage (BECCS) | Process of extracting bioenergy from biomass and capturing and storing the carbon, thereby removing it from the atmosphere |

Biomass energy | Energy found in plants |

Carbon capture / carbon sequestration | Process of extracting carbon and storing it, thus preventing it from being emitted in the atmosphere |

Carbon negative | Removing more carbon dioxide from the atmosphere than is emitted |

Carbon neutral | Achieving net zero carbon dioxide emissions by balancing carbon dioxide emissions with removal or elimination of carbon dioxide emissions altogether |

Carbon offset projects | Projects that allow companies to invest in environmental projects to make up for emissions of greenhouse gases [see also Verification] |

Carbon credit | Tradable instrument that conveys a right to emit a unit of pollution [See also Emission allowance] |

Carbon pricing | Captures the external costs of greenhouse gas emissions |

Carbon sink | A forest, ocean, or other natural environment that has the ability to absorb carbon dioxide from the atmosphere |

Carbon tax | Government-imposed fee on any company that burns fossil fuels (coal, oil, and natural gas) |

Certification | A Renewable Energy Credit is an instrument that certifies the bearer owns one megawatt-hour (MWh) of electricity generated from a renewable energy resource [See also Renewable Energy Credit] |

Decarbonization | Phasing out carbon dioxide emissions from the use of fossil fuels |

Deforestation | Clearing a wide area of trees |

Electrification | The process of replacing technologies that use fossil fuels with those that use electricity as a source of energy |

Emission allowance | Tradable instrument that conveys a right to emit a unit of pollution [See also Carbon credit] |

Greenhouse gas | Primarily water vapor, carbon dioxide, methane, nitrous oxide, and ozone, these gasses absorb and emit radiant energy within the thermal infrared range, causing warming of the atmosphere. |

Green power | Power derived from renewable energy sources and technologies that provide the highest environmental benefit—e.g., solar, wind, geothermal, biogas, biomass, and hydroelectric |

Green taxonomy | Classification system that identifies the activities or investments that deliver on environmental objectives, which can help investors identify opportunities for investments that comply with sustainability criteria |

Greenwashing | Creating the impression, sometimes inadvertently, that the company is doing more to protect the environment than it is |

Nuclear energy | Energy derived from nuclear reactions |

Renewable energy | Energy that is derived from a renewable resource - examples include hydro, wind, geothermal, solar, and biomass energy |

Renewable energy credit (REC) | One REC is equal to one megawatt hour of electricity generated from a renewable energy source [See also Certification] |

Scope 1 emissions | Direct emissions from the activities of an organization or activities under their control |

Scope 2 emissions | Indirect emissions from purchased electricity, steam, heating, and cooling consumed by an organization |

Scope 3 emissions | Emissions resulting from activities from assets not owned or controlled by an organization but occur within its value chain - includes all sources not within Scope 1 or Scope 2 |

Verification | The process of evaluating calculations of the actual amount of greenhouse gas emissions avoided or sequestered through implementation of a carbon offset project [see also Carbon offset programs] |

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click In the loop