Search within this section

Select a section below and enter your search term, or to search all click PwC SEC volume

Favorited Content

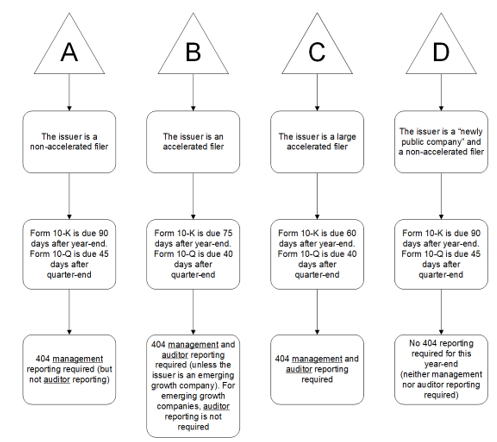

"This annual report does not include a report of management's assessment regarding internal control over financial reporting or an attestation report of the company's registered public accounting firm due to a transition period established by rules of the Securities and Exchange Commission for newly public companies."

|

"Because of the inter-relationship between Form S-3 eligibility and accelerated filer status, we believe that, to the extent a newly formed public company seeks to use and is deemed eligible to use Form S-3 on the basis of another entity's reporting history, that company would also be an accelerated filer and therefore required to comply with Items 308(a) and 308(b) of Regulation S-K in the first annual report that it files."

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click PwC SEC volume