This paper has been prepared for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS.

Purpose

1. Some stakeholders informed the staff that there are different interpretations of the guidance in Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, and IFRS 15, Revenue from Contracts with Customers (collectively referred to as the “new revenue standard”), for determining whether a customer option to acquire additional goods and services gives rise to a material right. This paper summarizes the potential implementation issue that was reported to the staff. The staff will seek input from members of the FASB-IASB Joint Transition Resource Group for Revenue Recognition on this potential implementation issue.

Background

2. Entities regularly grant options for additional goods and services to customers in the ordinary course of business. Some options are given as part of an entity's marketing efforts (that is, efforts to obtain future contracts with customers

) while others are purchased by customers (often implicitly) as part of a present contract and give customers a right to acquire additional goods and services at a discount. Those options come in many forms, including sales incentives, customer award (loyalty) credits (or points), contract renewal options, or other discounts on future goods or services. The following are some examples of options that exist in practice:

(a) A loyalty program that allows an entity's customers to accumulate points for every dollar spent. Those points may then be used to obtain free goods or services when enough points have been earned through future purchases.

(b) A voucher for a discount on future purchases made within a specified time period. The voucher is received only after a customer makes an initial purchase.

(c) A renewal option that allows an entity's customers to renew a contract at the end of the contract term by paying a renewal amount that is less than what the entity would charge its new customers for similar services.

(d) A contract that requires an entity's customers to pay a nonrefundable upfront fee (that does not relate to a promised good or service), but also includes an option that allows customers to renew the contract without paying an additional fee. The renewal rate may be fixed at contract inception or agreed upon at a later date.

Accounting Guidance

3. The core principle of the new revenue standard is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

4. The new standard includes five steps that are applied to achieve its core principle. Step 2 requires an entity to identify at contract inception all performance obligations in a contract with a customer, regardless of whether the entity views those performance obligations as perfunctory or inconsequential.

5. Paragraph 606-10-10-4 [4]

states that the new revenue standard specifies the accounting for an individual contract with a customer. However, as a practical expedient, an entity may apply the guidance to a portfolio of contracts with similar characteristics if the entity reasonably expects that the effects on the financial statements of applying the new standard to the portfolio would not differ materially from applying it to the individual contracts within the portfolio.

6. Paragraph 606-10-25-18 identifies customer options that provide a customer with a material right as an example of a promised good or service. Paragraphs 606-10-55-41 through 55-45 [B39–B43] include specific guidance on the determination of whether customer options for additional goods or services give rise to a material right and, thus, a performance obligation. A summary of some of that guidance is included below.

7. Additionally, paragraphs 606-10-55-335 through 55-360 [IE249–IE274] include examples to illustrate the guidance discussed in paragraphs 606-10-55-41 through 55-45 [B39–B43]. Those examples are included for reference in Appendix A of this paper.

8. Paragraph 606-10-55-42 [B40] states that the option to acquire additional goods or services gives rise to a performance obligation in a contract only if the option provides a material right to the customer that it would not receive without entering into that contract (for example, a discount that is incremental to the range of discounts typically given for those goods or services to that class of customer in that geographical area or market). If the option provides a material right to the customer, the customer in effect pays the entity in advance for future goods or services, and the entity recognizes revenue when those future goods or services are transferred or when the option expires.

9. Paragraph 606-10-55-43 [B41] explains that if a customer has the option to acquire an additional good or service at a price that would reflect the standalone selling price for that good or service, that option does not provide the customer with a material right even if the option can be exercised only by entering into a previous contract.

10. If an entity determines that a customer option provides a customer with a material right and, therefore, gives rise to a performance obligation, paragraph 606-10-55-44 [B42] requires an entity to allocate the transaction price to performance obligations on a relative standalone selling price basis. If the standalone selling price for a customer's option is not directly observable, an entity is required to estimate it.

11. The standalone selling price of a customer option would reflect factors such as the average purchase price of additional products provided by the option, any incremental discount provided by the option as compared with discounts obtained by customers who have not been provided with the option, and the likelihood that the option will be exercised.

12. In addition to the guidance provided in paragraphs 606-10-55-41 through 55-45 [B39–B43], paragraph BC387 clarifies that the notions of "significant" and "incremental" form the basis for the principle of a material right. The principle is, in part, derived from current revenue recognition guidance in Generally Accepted Accounting Principles (GAAP), which originally was developed for the software industry but is applied broadly across all industries. That existing guidance presumes that an offer of a discount on future purchases of goods or services is a separate option in a contract if that discount is (a) significant and (b) incremental to both the range of discounts reflected in the pricing of other elements in the contract and the range of discounts typically given in comparable transactions. However, the Boards acknowledged that, unlike current GAAP, under the new revenue standard even if (for example) a discount is not incremental to the range of discounts reflected in the pricing of other elements in the contract, it could give rise to a material right to the customer.

13. The determination of whether an option provides a material right also affects the timing of revenue recognition for a nonrefundable upfront fee. Paragraph 606-10-55-51 [B49] states that an entity that charges its customers a nonrefundable upfront fee at or near contract inception must first assess whether the fee relates to the transfer of a promised good or service. A nonrefundable upfront fee that does not relate to a promised good or service is considered an advance payment for future goods and services. The period over which the fee is recognized may extend beyond the initial contractual period if the entity grants the customer the option to renew the contract and that option provides the customer with a material right as described in paragraph 606-10-55-42 [B40].

Implementation Issues

14. An entity will need to apply judgement based on its own facts and circumstances to determine whether a contract with a customer includes a material right. This section of the paper includes analyses of two questions regarding the type of information that an entity should evaluate when determining whether a contract with a customer includes a material right. Within each analysis, the staff included examples to facilitate a discussion among members of the FASB-IASB Joint Transition Resource Group for Revenue Recognition.

Issue 1: Should the evaluation of whether an option provides a material right be performed in the context of only the current transaction with a customer or should the evaluation also consider past and expected future transactions with the customer?

15. Because paragraph 606-10-10-4 [4] (among others) indicates that the new revenue standard applies to individual contracts with a customer, some have questioned the accounting for certain types of transactions that provide customers with rights in a current transaction that may only become material when combined with rights that have been accumulated in past transactions and/or will be accumulated in future transactions.

16. The staff is aware of the following two views:

(a) View A—The evaluation of whether an option provides a material right should be performed only in the context of the current transaction with the customer.

(b) View B—The evaluation of whether an option provides a material right should consider all relevant transactions with the customer (that is, current, past, and future transactions).

17. Proponents of View A noted that the guidance in paragraph 606-10-10-4 [4] (as well as other references to accounting for an individual contract) suggests that the evaluation of whether a customer option gives rise to a material right should be performed based only on the factors present in the current transaction with a customer. That is, proponents of View A asserted that the evaluation should be performed as of a point in time on a standalone basis and should not be influenced by factors outside of the individual contract with the customer (such as the ability of the rights accumulated in the current transaction to be combined with other rights previously accumulated or expected to be accumulated in future transactions).

18. Proponents of View B stated that all facts and circumstances, including those that exist outside of the current transaction with a customer, should be considered when evaluating whether a customer option gives rise to a material right. That is, proponents of View Bnoted that forward-looking factors, such as how a right accumulates over time, should be considered when evaluating whether an existing option gives rise to a material right. Proponents of View B also observed that paragraph 606-10-55-42 [B40] indicates that when evaluating a discount in a contract, consideration should be given to "discounts typically given for those goods or services to that class of customer in that geographical area or market," which they state further supports considering facts and circumstances beyond the current transaction with the customer.

19. To illustrate the two views, consider the examples below. The estimated standalone selling prices used in all examples in this paper have been created for illustrative purposes only and are not meant to demonstrate actual standalone selling prices. However, it should be assumed that the standalone selling prices were calculated consistent with the methodologies in the new revenue standard, which are outlined in certain of the examples included in Appendix A.

Example 1—Loyalty Program

20. Entity A has a loyalty program in which its customers accumulate one point for every dollar spent. Points may be exchanged for free products when the customer accumulates enough points. Based on its historical data, Entity A determines that it is likely that its customers will accumulate enough loyalty points to receive a free product.

21. In the current transaction, Customer Y purchases a product from Entity A for $50 and receives 50 loyalty points. Entity A concludes that each loyalty point has a standalone selling price of $0.01.

View A

22. Entity A would evaluate whether the estimated standalone selling price of the loyalty points (that is, $0.50) earned from the current transactions is a material right in relation to the current transaction. Entity A would not consider whether the customer previously accumulated points from prior transactions or whether there is a reasonable expectation that the customer will continue to accumulate points in future transactions.

View B

23. Entity A would consider whether the loyalty points earned from the current transaction are expected to contribute to a material right that the customer has (or will) accumulate. The evaluation would consider that an element of the right granted to Customer Y in the current transaction is the customer's ability to accumulate loyalty points that will entitle the customer to a free product.

Example 2—"Buy three and get one free" program

24. Entity A offers a program in which customers who have purchased three products over a given period of time may receive a fourth product free. Based on its historical data, Entity A determines that it is likely that its customers will receive a free product.

25. After a customer purchases the first of the three products, the customer has obtained an option (that is, an escalating right) that allows the customer to receive a free product if the customer chooses to purchase two additional products. Similarly, after the customer purchases the second of the three products, it receives an option that allows the customer to receive a free product if the customer chooses to purchase one additional product. After completion of the third product purchase, the customer has an option to obtain a free product. As a result, the standalone selling price of each option may be different.

26. Assume that in the current transaction, which is the customer's first of the three required purchases, Customer Y purchases a product from Entity A at its observable standalone selling price of $6. Entity A concludes that the standalone selling price of the customer option in this transaction is $0.30.

View A

27. Entity A would evaluate whether the estimated standalone selling price of the option (that is, $0.30) in the current transaction is a material right in relation to the current transaction. Entity A would not consider whether there is a reasonable expectation that the customer will purchase two additional products and receive a free product.

View B

28. Entity A would consider that Customer Y has in-substance earned one-third of a free product in the current transaction (or in other words, has earned the right to receive one free product if the customer purchases two additional products). Entity A also would consider whether Customer Y is likely to purchase two additional products that will entitle it to a free product.

Issue 2: Is the evaluation of whether an option provides a material right solely a quantitative evaluation or should the evaluation

also

consider qualitative factors?

29. The staff is aware of the following two views:

(a) View A—The evaluation of whether an option provides a material right is a quantitative evaluation that considers only the standalone selling price of the option.

(b) View B—The evaluation of whether an option provides a material right should consider both quantitative and qualitative factors.

30. View A is largely based on the fact that the basis for conclusions (specifically, BC387) states that the notions of "significant" and "incremental" in existing GAAP formed "the basis for the principle of a material right" Some view the guidance that currently exists in GAAP as being principally quantitative in nature. That guidance requires an entity to consider whether a discount is quantitatively incremental to the range of discounts typically given in comparable transactions and whether the discount is "significant" BC387 makes clear that the Boards did not consider the third criterion in the existing GAAP guidance (that is, whether the discount is incremental to the range of discounts reflected in the pricing of other elements in the arrangement) pertinent to the material right analysis.

31. Under View B, quantitative and qualitative factors are considered when determining whether a material right exists. Supporters of View B noted that considering qualitative factors is more consistent with the notion that identifying promised goods or services should consider valid expectations of the customer (BC87). A customer's perspective on what constitutes a "material right" may consider any number of qualitative factors that would be known to the entity.

Example 3—Discount voucher

32. Entity A provides its customers who purchase goods on a particular day with a voucher for 25 percent off their next purchase (of any size). The voucher may be applied against the purchase of any product and expires after 60 days. Based on its historical data for similar offerings, Entity A determines that customers typically use the voucher to make an additional purchase that is, on average, more expensive than what a customer would typically purchase without a voucher. Entity A does not offer its customers any other discounts throughout the year.

33. On the day that Entity A offers its customers vouchers, Customer Y purchases a product for $200 and Customer Z purchases a product for $10.

View A

34. Entity A would evaluate whether each customer received a material right based on the standalone selling price of the voucher in relation to the transaction with the customer. Entity A might conclude that (a) one customer received a material right and the other did not or (b) both customers did or did not receive a material right using a quantitative evaluation, which would be based on the standalone selling price of the voucher.

View B

35. Entity A would consider the quantitative nature of the rights received by each customer as described in View A. However, Entity A also would consider that the voucher has given both Customers Y and Z the opportunity to receive a 25 percent discount on a future purchase, including purchases for products that may have an observable standalone selling price that is significantly higher than the selling prices of the products purchased by Customers Y and Z in the current transactions.

Example 4—Nonrefundable upfront fee

36. Entity A and Customer Y enter into a 12-month service contract for $60 per month. All customers are required to agree to a 12-month contract. In addition to the monthly fee, Customer Y also must pay a $120 nonrefundable fee at contract inception. The upfront fee is not considered to transfer a promised good or service. Customer Y will only pay the $120 fee once as long as it continuously remains a customer of Entity A. Entity A's customers have multiple service providers available to them in their geographic area. While monthly service fees are similar throughout the geographic area, some of those service providers do not charge customers upfront fees to initiate services for customers who are existing customers of a competitor.

37. The contract also contains a renewal option that allows Customer Y to renew the contract on a month-to-month basis. The contract does not stipulate the renewal price, but Entity A does not operate in a volatile industry and service rates have historically remained relatively stable (that is, the monthly fee is not expected to significantly increase or decrease). As a practical alternative to estimating the standalone selling price of the renewal option, Entity A evaluates the renewal option by reference to the services provided (in accordance with paragraph 606-10-55-45 [B43]).

View A

38. Entity A would evaluate whether Customer Y received a material right based on an evaluation of whether its customers receive a material right with respect to renewal of the services because they do not have to pay an additional $120 upfront fee at the beginning of the renewal period. In this case, Entity A would consider whether the renewal price that Customer Y will pay (that is, $60/month) compared with the allocated price that a new customer would pay for the same services ($120/12 = $10 + $60/month fee = $70) provides the customer with a material right.

View B

39. Entity A would consider the quantitative factors evaluated in View A, but would also consider qualitative factors such as the availability and pricing of service alternatives. For example, Entity A might consider the fact that after the one-year fixed term, Customer Y could get substantially similar services from one of Entity A's competitors at the same price as it would receive those services from Entity A (that is, $60/month). This might call into question whether the option to renew Entity A's services at $60/month provides Customer Y with a material right that it would not have received without entering into the initial services contract with Entity A.

Questions for the TRG Members

How would you apply the guidance about whether a customer option to acquire additional goods or services gives rise to a material right to the examples in this paper?

Are there any related potential interpretation issues that are not included in this paper?

Appendix A

> > Customer Options for Additional Goods or Services

606-10-55-335 [IE249] Examples 49–52 illustrate the guidance in paragraphs 606-10-55-41 through 55-45 [B39–B43] on customer options for additional goods or services. Example 50 illustrates the guidance in paragraphs 606-10-25-19 through 25-21 [27–29] on identifying performance obligations. Example 52 illustrates a customer loyalty program. That Example may not apply to all customer loyalty arrangements because the terms and conditions may differ. In particular, when there are more than two parties to the arrangement, an entity should consider all facts and circumstances to determine the customer in the transaction that gives rise to the award credits.

> > > Example 49—Option That Provides the Customer with a Material Right (Discount Voucher)

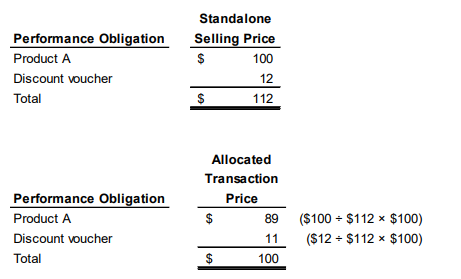

606-10-55-336 [IE250] An entity enters into a contract for the sale of Product A for $100. As part of the contract, the entity gives the customer a 40 percent discount voucher for any future purchases up to $100 in the next 30 days. The entity intends to offer a 10 percent discount on all sales during the next 30 days as part of a seasonal promotion. The 10 percent discount cannot be used in addition to the 40 percent discount voucher.

606-10-55-337 [IE251] Because all customers will receive a 10 percent discount on purchases during the next 30 days, the only discount that provides the customer with a material right is the discount that is incremental to that 10 percent (that is, the additional 30 percent discount). The entity accounts for the promise to provide the incremental discount as a performance obligation in the contract for the sale of Product A.

606-10-55-338 [IE252] To estimate the standalone selling price of the discount voucher in accordance with paragraph 606-10-55-44 [B42], the entity estimates an 80 percent likelihood that a customer will redeem the voucher and that a customer will, on average, purchase $50 of additional products. Consequently, the entity's estimated standalone selling price of the discount voucher is $12 ($50 average purchase price of additional products × 30 percent incremental discount × 80 percent likelihood of exercising the option). The standalone selling prices of Product A and the discount voucher and the resulting allocation of the $100 transaction price are as follows:

606-10-55-339[IE253] The entity allocates $89 to Product A and recognizes revenue for Product A when control transfers. The entity allocates $11 to the discount voucher and recognizes revenue for the voucher when the customer redeems it for goods or services or when it expires.

> > > Example 50—Option That Does Not Provide the Customer with a Material Right (Additional Goods or Services)

606-10-55-340[IE254] An entity in the telecommunications industry enters into a contract with a customer to provide a handset and monthly network service for two years. The network service includes up to 1,000 call minutes and 1,500 text messages each month for a fixed monthly fee. The contract specifies the price for any additional call minutes or texts that the customer may choose to purchase in any month. The prices for those services are equal to their standalone selling prices.

606-10-55-341 [IE255] The entity determines that the promises to provide the handset and network service are each separate performance obligations. This is because the customer can benefit from the handset and network service either on their own or together with other resources that are readily available to the customer in accordance with the criterion in paragraph 606-10-25-19(a) [27(a)]. In addition, the handset and network service are separately identifiable in accordance with the criterion in paragraph 606-10-25-19(b) [27(b)] (on the basis of the factors in paragraph 606-10-25-21 [29]). 606-10-55-342 [IE256] The entity determines that the option to purchase the additional call minutes and texts does not provide a material right that the customer would not receive without entering into the contract (see paragraph 606-10-55-43 [B41]). This is because the prices of the additional call minutes and texts reflect the standalone selling prices for those services. Because the option for additional call minutes and texts does not grant the customer a material right, the entity concludes it is not a performance obligation in the contract. Consequently, the entity does not allocate any of the transaction price to the option for additional call minutes or texts. The entity will recognize revenue for the additional call minutes or texts if and when the entity provides those services.

> > > Example 51—Option That Provides the Customer with a Material Right (Renewal Option)

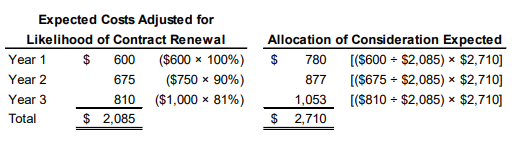

606-10-55-343 [IE257] An entity enters into 100 separate contracts with customers to provide 1 year of maintenance services for $1,000 per contract. The terms of the contracts specify that at the end of the year, each customer has the option to renew the maintenance contract for a second year by paying an additional $1,000. Customers who renew for a second year also are granted the option to renew for a third year for $1,000. The entity charges significantly higher prices for maintenance services to customers that do not sign up for the maintenance services initially (that is, when the products are new). That is, the entity charges $3,000 in Year 2 and $5,000 in Year 3 for annual maintenance services if a customer does not initially purchase the service or allows the service to lapse.

606-10-55-344 [IE258]The entity concludes that the renewal option provides a material right to the customer that it would not receive without entering into the contract because the price for maintenance services are significantly higher if the customer elects to purchase the services only in Year 2 or 3. Part of each customer's payment of $1,000 in the first year is, in effect, a nonrefundable prepayment of the services to be provided in a subsequent year. Consequently, the entity concludes that the promise to provide the option is a performance obligation.

606-10-55-345 [IE259] The renewal option is for a continuation of maintenance services, and those services are provided in accordance with the terms of the existing contract. Instead of determining the standalone selling prices for the renewal options directly, the entity allocates the transaction price by determining the consideration that it expects to receive in exchange for all the services that it expects to provide in accordance with paragraph 606-10-55-45 [B43].

606-10-55-346 [IE260] The entity expects 90 customers to renew at the end of Year 1 (90 percent of contracts sold) and 81 customers to renew at the end of Year 2 (90 percent of the 90 customers that renewed at the end of Year 1 will also renew at the end of Year 2, that is 81 percent of contracts sold).

606-10-55-347 [IE261] At contract inception, the entity determines the expected consideration for each contract is $2,710 [$1,000 + (90 percent × $1,000) + (81 percent × $1,000)]. The entity also determines that recognizing revenue on the basis of costs incurred relative to the total expected costs depicts the transfer of services to the customer. Estimated costs for a three-year contract are as follows:

Year 1 $ 600

Year 2 $ 750

Year 3 $ 1,000

606-10-55-348 [IE262] Accordingly, the pattern of revenue recognition expected at contract inception for each contract is as follows:

606-10-55-349 [IE263] Consequently, at contract inception, the entity allocates to the option to renew at the end of Year 1 $22,000 of the consideration received to date [cash of $100,000 – revenue to be recognized in Year 1 of $78,000 ($780 × 100)].

606-10-55-350 [IE264] Assuming there is no change in the entity's expectations and the 90 customers renew as expected, at the end of the first year, the entity has collected cash of $190,000 [(100 × $1,000) + (90 × $1,000)], has recognized revenue of $78,000 ($780 × 100), and has recognized a contract liability of $112,000.

606-10-55-351 [IE265] Consequently, upon renewal at the end of the first year, the entity allocates $24,300 to the option to renew at the end of Year 2 [cumulative cash of $190,000 – cumulative revenue recognized in Year 1 and to be recognized in Year 2 of $165,700 ($78,000 + $877 × 100)].

606-10-55-352 [IE266] If the actual number of contract renewals was different than what the entity expected, the entity would update the transaction price and the revenue recognized accordingly.

> > > Example 52—Customer Loyalty Program

606-10-55-353 [IE267] An entity has a customer loyalty program that rewards a customer with 1 customer loyalty point for every $10 of purchases. Each point is redeemable for a $1 discount on any future purchases of the entity's products. During a reporting period, customers purchase products for $100,000 and earn 10,000 points that are redeemable for future purchases. The consideration is fixed, and the standalone selling price of the purchased products is $100,000. The entity expects 9,500 points to be redeemed. The entity estimates a standalone selling price of $0.95 per point (totalling $9,500) on the basis of the likelihood of redemption in accordance with paragraph 606-10-55-44 [B42].

606-10-55-354 [IE268] The points provide a material right to customers that they would not receive without entering into a contract. Consequently, the entity concludes that the promise to provide points to the customer is a performance obligation. The entity allocates the transaction price ($100,000) to the product and the points on a relative standalone selling price basis as follows:

606-10-55-355 [IE269] At the end of the first reporting period, 4,500 points have been redeemed, and the entity continues to expect 9,500 points to be redeemed in total. The entity recognizes revenue for the loyalty points of $4,110 [(4,500 points ÷ 9,500 points) × $8,676] and recognizes a contract liability of $4,566 ($8,676 – $ 4,110) for the unredeemed points at the end of the first reporting period.

606-10-55-356 [IE270] At the end of the second reporting period, 8,500 points have been redeemed cumulatively. The entity updates its estimate of the points that will be redeemed and now expects that 9,700 points will be redeemed. The entity recognizes revenue for the loyalty points of $3,493 {[(8,500 total points redeemed ÷ 9,700 total points expected to be redeemed) × $8,676 initial allocation] – $4,110 recognized in the first reporting period}. The contract liability balance is $1,073 ($8,676 initial allocation – $7,603 of cumulative revenue recognized).

> > Nonrefundable Upfront Fees

606-10-55-357 [IE271] Example 53 illustrates the guidance in paragraphs 606-10-55-50 through 55-53 [B48-B51] on nonrefundable upfront fees.

> > > Example 53—Nonrefundable Upfront Fee

606-10-55-358 [IE272] An entity enters into a contract with a customer for one year of transaction processing services. The entity's contracts have standard terms that are the same for all customers. The contract requires the customer to pay an upfront fee to set up the customer on the entity's systems and processes. The fee is a nominal amount and is nonrefundable. The customer can renew the contract each year without paying an additional fee.

606-10-55-359 [IE273] The entity's setup activities do not transfer a good or service to the customer and, therefore, do not give rise to a performance obligation.

606-10-55-360 [IE274] The entity concludes that the renewal option does not provide a material right to the customer that it would not receive without entering into that contract (see paragraph 606-10-55-42 [B40]). The upfront fee is, in effect, an advance payment for the future transaction processing services. Consequently, the entity determines the transaction price, which includes the nonrefundable upfront fee, and recognizes revenue for the transaction processing services as those services are provided in accordance with paragraph 606-10-55-51 [B49].

___________ The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org

1 Marketing and promotional offers are not included in the scope of this issue. The new revenue standard states that those options exist independently of a present contract with a customer and, therefore, do not constitute performance obligations in that contract.

2 IFRS 15 references are included in "[XX]" throughout this paper.

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.