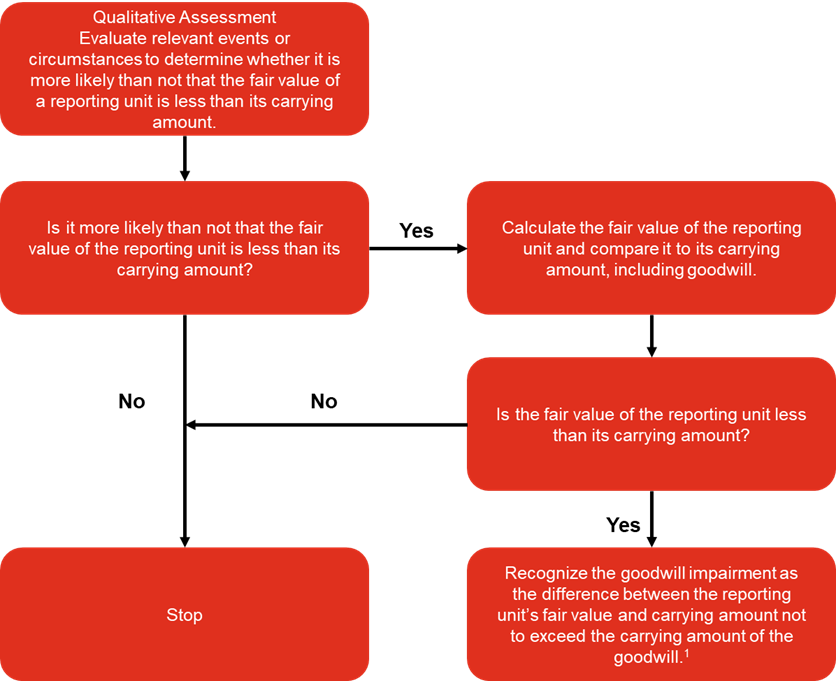

If an event occurs or circumstances change between annual tests that could more likely than not reduce the fair value of a reporting unit below its carrying amount (triggering events), the goodwill of that reporting unit should be tested for impairment using the process described in

BCG 9.8. The factors considered in a qualitative assessment of goodwill (outlined in

BCG 9.6) are also examples of interim triggering events that should be considered in determining whether goodwill should be tested for impairment during interim periods. Such factors include changes in macroeconomic conditions, cost increases, and share price, among others.

In accordance with

ASC 350-20-40-7, when a portion of goodwill is allocated to a business to be disposed of, the goodwill remaining in the portion of the reporting unit to be retained must also be tested for impairment. See

BCG 9.10 for further information.

Question BCG 9-3

Can the original transaction price be used as an indicator of fair value in the first post acquisition goodwill impairment test? What if the next highest bid was substantially lower?

PwC response

When assessing fair value in the first goodwill impairment test after an acquisition, an acquirer may consider the purchase price as one data point, among others, in determining fair value, unless there is contradictory evidence.

ASC 820-10-30-3A requires that a reporting entity consider factors specific to the transaction in determining whether the transaction price represents fair value. The fact that the next highest bid was substantially lower than an acquirer’s bid does not necessarily mean that the transaction price is not representative of fair value, but it could indicate that significant acquirer-specific synergies were included in the determination of the purchase price.

Question BCG 9-4 If none of the events and circumstances described in

ASC 350-20-35-3C are present, can an entity conclude that it does not have a requirement to perform an interim impairment test for goodwill?

PwC response

No. The indicators listed in

ASC 350-20-35-3C are examples, and do not comprise an exhaustive list.

ASC 350-20-35-3F indicates that an entity should consider other relevant events and circumstances that affect the fair value or carrying amount of a reporting unit.

Additional examples of events that may indicate that an interim impairment test is necessary include:

- Impairments of other assets or the establishment of valuation allowances on deferred tax assets

- Cash flow or operating losses at the reporting unit level (the greater the significance and duration of losses, the more likely it is that a triggering event has occurred)

- Negative current events or long-term outlooks for specific industries impacting the company as a whole or specific reporting units

- Not meeting analyst expectations or internal forecasts in consecutive periods, or downward adjustments to future forecasts

- Planned or announced plant closures, layoffs, or asset dispositions

- Market capitalization of the company below its book value

Therefore, only after considering all available evidence, can a company conclude that it does not have a requirement to perform an interim impairment test for goodwill.

Question BCG 9-5

Does the option to perform a qualitative impairment assessment change how an entity would determine whether it needs to perform an event-driven interim test?

PwC response

The option to perform a qualitative impairment assessment does not change when an entity should perform a goodwill impairment test. An interim test should be performed if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying amount.

For entities with publicly traded equity or debt securities, although the impairment test for goodwill occurs at the reporting unit level, a significant decline in the market value of such securities may indicate the need for an interim impairment test. It is important to remember that the goodwill test is not based on an “other than temporary” decline. When a substantial decline occurs, an entity should consider whether it is “more likely than not” that the fair value of any of the entity’s reporting units has declined below the reporting unit’s carrying amount. In these situations, an entity should examine the underlying reasons for the decline, the significance of the decline, and the length of time the market price has been depressed to determine if a triggering event has occurred. A decline that is severe, even if it is recent, as a result of an event that is expected to continue to affect the company will likely trigger the need for a test. Further, a decline that is of an extended duration will also likely trigger the need for a test. In contrast, a relatively short-term decline in the market price of the company’s stock may not be indicative of an actual decline in the company’s fair value when one considers all available evidence. Interim impairment triggers can also be present at the reporting unit level even when a public company’s market capitalization is equal to or greater than its book value. All available evidence should be considered when determining a reporting unit’s fair value.

Question BCG 9-6

In lieu of performing its goodwill impairment test, can a company, whose market capitalization is significantly below book value, write off its goodwill in its entirety?

PwC response

To recognize a goodwill impairment, the company will need to test each reporting unit to determine the amount of a goodwill impairment loss. If the fair value of a reporting unit is greater than its carrying amount in the quantitative goodwill impairment test, a company cannot record a goodwill impairment.

Question BCG 9-7

If a company experiences a decline in market capitalization that is consistent with declines experienced by others within its industry, is it reasonable for the company to assert that a triggering event has not occurred and that the decline is an indication of distressed transactions and not reflective of the underlying value of the company?

PwC response

There are times when a distressed transaction may be put aside. However, a distressed market cannot be ignored. A decline in a company’s market capitalization, consistent with declines experienced by others within its industry, may be reflective of the underlying value of the company in a distressed market and the impact of an economic downturn or changes in market multiples in the company’s industry, which is one of the factors described in

ASC 350-20-35-3C. Entities should distinguish between a distressed market, in which prices decline yet liquidity exists with sufficient volume, and a forced or distressed transaction. Transactions at depressed prices in a distressed market would not typically be distressed transactions.

Question BCG 9-8

If a company has not experienced a decline in its cash flows and expects that it will continue to meet its projected cash flows in the future, can the company assert that a triggering event has not occurred even though the decline in its market capitalization may be significant?

PwC response

While a company may not have experienced a decline in its cash flows and does not anticipate a future decline in projected cash flows, it is not appropriate to simply ignore market capitalization when evaluating the need for an interim impairment test. The market capitalization usually reflects the market’s expectations of the future cash flows of the company. A company may need to reconsider its projected cash flows due to heightened uncertainty about the amount and/or timing of cash flows, particularly for industries in which customer purchases are discretionary. Even if there is no change in a company’s cash flows, higher required rates of return demanded by investors in an economic downturn may decrease a company’s discounted cash flows. This, in turn, will decrease fair value.

Question BCG 9-9

If a company completed its annual goodwill impairment test during the fourth quarter and the company has not identified any significant changes in its business during the first quarter of the following year, is a continued depressed stock price or a further decline during the first quarter a triggering event for performing a goodwill impairment test?

PwC response

If a company’s stock price remains at a depressed level or continues to decline during the first quarter, it is important to ensure all available evidence has been evaluated to determine if a triggering event has occurred. The market capitalization generally reflects the market’s expectations of the future cash flows of the company. When the market capitalization drops, this may indicate that an event has occurred, or circumstances or perceptions have changed that would more likely than not reduce the fair value of a company’s reporting unit below its carrying amount. For example, the decline in the stock price may be an indicator that the company’s cash flow projections in future periods are too optimistic when considering the most recent macroeconomic forecasts.

A company should compare its actual results to date against budget and consider whether its projections appropriately reflect current expectations of the length and severity of recent economic conditions. Reviewing externally available information (e.g., analyst reports, industry publications, and information about peer companies) may provide further insight on the factors attributable to the decline and whether a reporting unit has had a triggering event. When evaluating external information, it is important to ensure it is comparable to the reporting unit under review and not solely to the consolidated company. Further, the amount by which the fair value of the reporting unit exceeded its carrying amount at the last goodwill impairment test date may also be a consideration in evaluating if it is more likely than not that the fair value of a reporting unit has dropped below its carrying amount.

Similar to other impairment charges, financial statement users, auditors, and regulators may scrutinize the timing of goodwill impairment losses. Entities that recognize a goodwill impairment loss should be prepared to address questions about (1) the timing of the impairment charge, (2) the events and circumstances that caused the reporting unit’s goodwill to become impaired, and (3) for public entities, the adequacy of the entity’s “early warning” disclosures (e.g., those described in SEC

FRM 9510.3), including relevant risks and business developments leading up to the charge, in its public reporting for prior periods.

View image

View image