Search within this section

Select a section below and enter your search term, or to search all click Financial statement presentation

Favorited Content

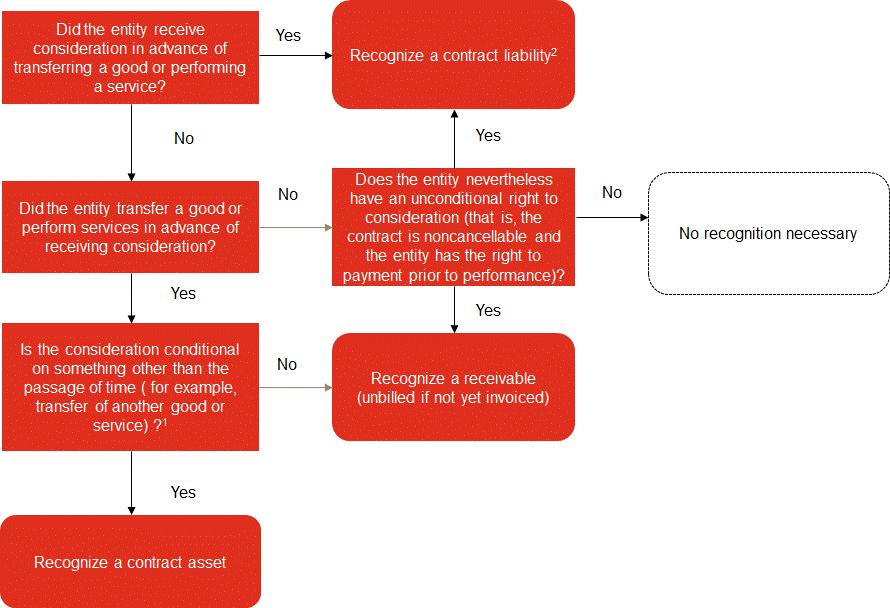

When either party to a contract has performed, an entity shall present the contract in the statement of financial position as a contract asset or a contract liability, depending on the relationship between the entity’s performance and the customer’s payment. An entity shall present any unconditional rights to consideration separately as a receivable.

Excerpt from ASC 606-10-45-3 [edits applicable upon adoption of ASU 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments]

A contract asset is an entity’s right to consideration in exchange for goods or services that the entity has transferred to a customer. An entity shall assess a contract asset for impairment in accordance with Topic 310 on receivables. [An entity shall assess a contract asset for credit losses in accordance with Subtopic 326-20 on financial instruments measured at amortized cost. A credit loss of a contract asset shall be measured, presented, and disclosed in accordance with Subtopic 326-20.]

Excerpt from ASC 606-10-45-4 [edits applicable upon adoption of ASU 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments]

A receivable is an entity’s right to consideration that is unconditional. A right to consideration is unconditional if only the passage of time is required before payment of that consideration is due…. An entity shall account for a receivable in accordance with Topic 310. […and Subtopic 326-20. Upon initial recognition of a receivable from a contract with a customer, any difference between the measurement of the receivable in accordance with Subtopic 326-20 and the corresponding amount of revenue recognized shall be presented as a credit loss expense.]

If a customer pays consideration or an entity has a right to an amount of consideration that is unconditional (that is, a receivable), before the entity transfers a good or service to the customer, the entity shall present the contract as a contract liability when the payment is made or the payment is due (whichever is earlier). A contract liability is an entity’s obligation to transfer goods or services to a customer for which the entity has received consideration (or an amount of consideration is due) from the customer.

Dr. Receivable

|

$5,000

|

|

Cr. Contract liability

|

$5,000

|

Dr. Cash

|

$5,000

|

|

Cr. Receivable

|

$5,000

|

Dr. Contract liability

|

$5,000

|

|

Cr. Revenue

|

$5,000

|

Dr. Receivable

|

$5,000

|

|

Cr. Revenue

|

$5,000

|

Dr. Cash

|

$5,000

|

|

Cr. Receivable

|

$5,000

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Financial statement presentation