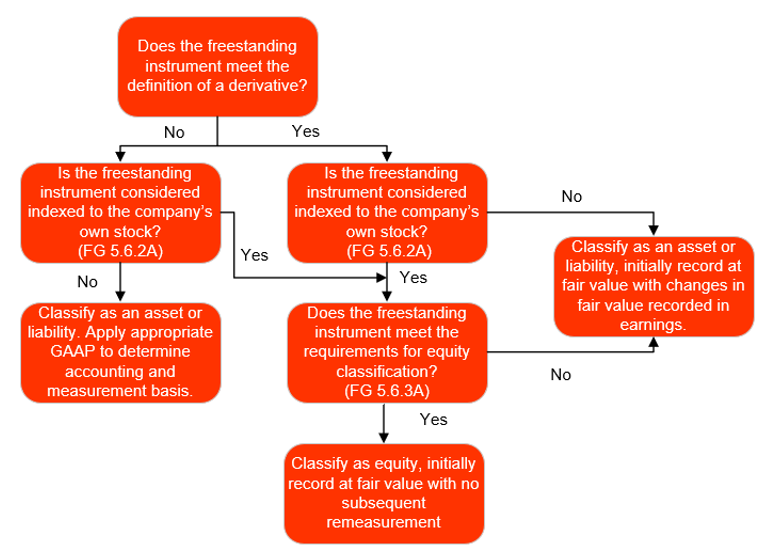

ASC 815-40-15-7C provides guidance on how to evaluate an instrument’s settlement provisions to determine whether the instrument is indexed to the reporting entity’s own stock. This guidance is often referred to as the “fixed for fixed” rule.

ASC 815-40-15-7C

An instrument (or embedded feature) shall be considered indexed to an entity’s own stock if its settlement amount will equal the difference between the following:

a. The fair value of a fixed number of the entity’s equity shares

b. A fixed monetary amount or a fixed amount of a debt instrument issued by the entity.

For example, an issued share option that gives the counterparty a right to buy a fixed number of the entity’s shares for a fixed price or for a fixed stated principal amount of a bond issued by the entity shall be considered indexed to the entity’s own stock.

The strike price or the number of shares used to calculate the settlement amount is not considered fixed if the terms of the instrument or embedded component allow for any potential adjustment (except as discussed below), regardless of the probability of the adjustment being made or whether the reporting entity can control the adjustment.

ASC 815-40-15-7E discusses the exception to the “fixed for fixed” rule. This exception allows an instrument to be considered indexed to the reporting entity’s own stock even if adjustments to the settlement amount can be made, provided those adjustments are based on standard inputs used to determine the value of a “fixed for fixed” forward or option on equity shares (and the step one analysis does not preclude such a conclusion).

ASC 815-40-15-7E

A fixed-for-fixed forward or option on equity shares has a settlement amount that is equal to the difference between the price of a fixed number of equity shares and a fixed strike price. The fair value inputs of a fixed-for-fixed forward or option on equity shares may include the entity’s stock price and additional variables, including all of the following:

a. Strike price of the instrument

b. Term of the instrument

c. Expected dividends or other dilutive activities

d. Stock borrow cost

e. Interest rates

f. Stock price volatility

g. The entity’s credit spread

h. The ability to maintain a standard hedge position in the underlying shares.

Determinations and adjustments related to the settlement amount (including the determination of the ability to maintain a standard hedge position) shall be commercially reasonable.

Including other variables, or incorporating a leverage factor that increases the instrument’s exposure to the variables in

ASC 815-40-15-7E, would preclude the instrument from being considered indexed to the reporting entity’s own stock.

Example FG 5-7A through Example FG 5-11A illustrate the application of step two of the indexation guidance.

EXAMPLE FG 5-7A

Evaluation of an arrangement with multiple potential settlement alternatives

A company enters into an arrangement to issue shares with the following provisions:

- Three-year maturity

- 100,000 shares will be issued if the VWAP of the company’s stock is greater than $15 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $20 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $25 for any 20 days within a 30-day trading period

Analysis

This arrangement provides for multiple settlement alternatives. The contract could result in the issuance of 0, 100,000, 200,000, or 300,000 shares based on whether VWAP exceeds targeted prices. When evaluated under step one of the indexation guidance, in all scenarios, the event that triggers the issuance of shares is based on an observable market price, but it is the price of the company’s shares. However, unlike Example FG 5-5A, since there could be a different number of shares issued as a result of the multiple settlement alternatives (i.e. 0, 100,000, 200,000, or 300,000 shares), the arrangement would need to be analyzed under step two of the indexation guidance.

Under step two of the indexation guidance, stock price determines the number of shares to be issued, which is an input into a “fixed-for-fixed” valuation model. If the other requirements in

ASC 815-40 are met (see

FG 5.6.3A), this arrangement may be considered an equity instrument.

EXAMPLE FG 5-8A

Evaluation of an arrangement with multiple potential settlement alternatives, including a change in control event

A company enters into an arrangement under which additional shares will be issued if during the subsequent three-year period, certain thresholds are met, as follows:

- 100,000 shares will be issued if the VWAP of the company’s stock is greater than $15 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $20 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $25 for any 20 days within a 30-day trading period

- 300,000 shares will be issued if there is a change in control of the company

The arrangement meets the definition of a derivative under

ASC 815.

Analysis

This arrangement provides for multiple settlement alternatives. The contract could result in the issuance of 0, 100,000, 200,000, or 300,000 shares based on whether the VWAP exceeds targeted prices. In addition, if there is a change in control, 300,000 shares are issued. Since there could be a different number of shares issued, it would be analyzed under step two of the indexation guidance.

Stock price impacts the number of shares to be issued, which is an input into a “fixed-for-fixed” valuation model. However, in the event of a change in control, 300,000 shares are issued, which is not an input into a “fixed-for-fixed” valuation model. As a result, this arrangement would be required to be classified as a liability and measured at fair value with changes in fair value recorded in current earnings.

There may be other arrangements similar to Example FG 5-8A with multiple stock price triggers and other triggers that should be analyzed. For example, an instrument that meets the definition of a derivative under

ASC 815 with multiple stock price triggers might also include the following provisions:

- If there is a change in control of the company, and stock price is greater than $20, then 300,000 shares are issued

- If there is a liquidation of the company, then 300,000 shares are issued

- If there is a change in control of the company, and stock price is greater than $10, then a pro-rata number of shares between 0 and 100,000 will be issued

Similar to Example FG 5-8A, when analyzed under step two, these fact patterns (when coupled with multiple stock price triggers) will result in the instrument being liability classified and measured at fair value with changes in fair value reported in current earnings because change in control or a liquidation of the company are not inputs into a “fixed-for-fixed” pricing model.

EXAMPLE FG 5-9A

Evaluation of an arrangement to issue shares with multiple settlement alternatives and measures

A company enters into an arrangement under which additional shares will be issued if during the subsequent three-year period, certain thresholds are met, as follows:

- 100,000 shares will be issued if the VWAP of the company’s stock is greater than $15 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $20 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $25 for any 20 days within a 30-day trading period

- If there is a change in control of the company, the price at which the change in control occurred will be used to determine the number of shares to be issued (based upon the same stock price triggers above) as opposed to the VWAP

The arrangement meets the definition of a derivative under

ASC 815.

Analysis

This arrangement provides for multiple settlement alternatives. The contract could result in the issuance of 0, 100,000, 200,000, or 300,000 shares based on whether the VWAP or the change in control price exceeds targeted prices. For the purposes of this example, the application of step 1 of the indexation guidance is not illustrated. Since there could be a different number of shares issued (0, 100,000, 200,000, or 300,000), it would be analyzed under step two of the indexation guidance.

In evaluating the arrangement under step two, it is important to determine if stock price is the only measure that can determine the number of shares to be issued because stock price is an input into a “fixed-for-fixed” valuation model. If the manner in which the change in control price is determined and VWAP over a short time period are both reasonable means in which to measure the fair value of the company’s stock, the arrangement may be considered indexed to the entity’s own stock.

Assessing whether the change in control price is a reasonable measure of the fair value of the company’s stock requires careful consideration of (1) the events considered to be a change in control under the arrangement and (2) the manner in which the change in control price is calculated. For example, many change in control provisions include a company selling substantially all of its assets. If the change in control price calculation does not consider the potential dilutive impact of this arrangement (and potentially other arrangements), it would not be deemed to be a reasonable manner in which to calculate the fair value of the company’s stock. If, however, the change in control price calculation considers the potential dilutive impact of this arrangement (and potentially other arrangements), it may be deemed to be a reasonable manner in which to calculate the fair value of the company’s stock. Calculations that consider the dilutive impact of the arrangement itself are complex and likely require iterative or simultaneous equation calculations.

If the change in control price calculation is not a reasonable manner in which to calculate the fair value of the company’s stock, the arrangement would be required to be classified as a liability and measured at fair value with changes in fair value recorded in current earnings.

If the change in control price calculation is a reasonable manner in which to calculate the fair value of the company’s stock and the other requirements in

ASC 815-40 are met (see

FG 5.6.3A), this arrangement may be considered an equity instrument.

EXAMPLE FG 5-10A

Evaluation of a warrant issued in a SPAC transaction

A warrant issued in a SPAC transaction exercisable for 1 share of common stock over a five-year term has a strike price of $11.50 and includes the following provisions:

- In the event that the stock price of the company exceeds $18, the company can redeem the warrant for $0.01.

- If the company elects to redeem the warrant, the warrant holder can exercise the warrant.

- The company cannot redeem the warrant while it is held by the sponsor/founder of the SPAC; the company is only able to redeem the warrant if the sponsor/founder transfers the warrant

- In the event that there is a change in control in which shareholders receive a specified form of consideration:

- the warrant holders will have the ability to exercise their warrants,

- the exercise price is reduced in an effort to compensate the holders for lost time value of the option (because they would be exercising before the warrant’s maturity date - a make-whole provision) based on an option valuation model, and

- the option valuation model works differently if the warrant is held by the founder/sponsor (not reflecting any ability of the company to redeem the warrants if transferred to a third party) or a third party (reflecting the company’s ability to redeem the warrants).

The arrangement meets the definition of a derivative under

ASC 815.

Analysis

In this example, the make-whole provision (exercise price reduction) is calculated differently depending on who holds the warrant (the founder/sponsor or a third party). The identity of the holder of the warrant is not an input to a “fixed-for-fixed” valuation model. This warrant would not be considered indexed to a company’s own stock. As a result, this warrant would be required to be classified as a liability and measured at fair value with changes in fair value recorded in current earnings.

In analyzing these features, it is important to understand if the warrant’s settlement amount can be impacted by who holds the warrant. In this example, the warrants issued to sponsors/founders contain provisions that change potential settlement amounts if the warrants are transferred to a third party. However, the SPAC warrants that are held by the public may not contain such features. If the warrants do not have any features that could change the settlement amount or how settlement is calculated, the warrants may be considered indexed to an entity’s own stock.

We understand that this is an example of a provision addressed in the SEC’s public statement (see

FG 5.6.5A for additional information).

There may be other features in a warrant agreement issued in connection with a SPAC that result in changes to settlement amounts or how settlement amounts are calculated depending on who holds the warrant. For example:

- In the event the company elects to redeem certain warrants and the holders exercise their warrants, the settlement amount may be different if the holder is a director or officer of the company.

- Some warrants permit net share settlement upon exercise (frequently referred to as a cashless exercise). In some warrant agreements, the inputs used to calculate the net settlement amount (i.e., shares to be delivered) may be different depending on if the warrant is held by the founder/sponsor or if it is held by a third party. For example, settlement could be based on:

- the ten day VWAP when held by a sponsor/founder and the average closing price of the stock over a ten-day period when held by another party, or

- the trailing average of stock price based on the date a warrant is exercised when held by the sponsor/founder and based on the date the warrant is redeemed by the company if held by others.

Based on the guidance in the SEC’s public statement (see

FG 5.6.5A), these warrants would not be considered indexed to a company’s own stock because the holder of the warrant can impact the settlement amount and the identity of a holder is not an input into a “fixed for fixed” valuation model. As a result, these warrants would be classified as liabilities and reported at fair value with changes in fair value reported in current earnings.

EXAMPLE FG 5-11A

Evaluation of arrangements when the number of shares issuable may increase based on employee behavior (sometimes referred to as a “last person standing provision”)

Arrangements in the company’s stock are issued to investors and employees with vested and unvested stock compensation awards. Assume that additional shares will be issued if during a three-year period, certain thresholds are met, as follows:

- 100,000 shares will be issued if the VWAP of the company’s stock is greater than $15 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $20 for any 20 days within a 30-day trading period

- An additional 100,000 shares will be issued if the VWAP of the company’s stock is greater than $25 for any 20 days within a 30-day trading period

The arrangements issued to employees with unvested options are subject to continued employment vesting requirements (which may be based on the employment vesting requirements in their unvested stock compensation awards). In the event that these arrangements are forfeited by employees, the number of shares that could be issued under these arrangements are “re-allocated” on a pro-rata basis to the other holders. This is sometimes referred to as a “last person standing provision”.

The arrangements meet the definition of a derivative under

ASC 815.

Analysis

The arrangements issued to unvested option holders in this case would be considered compensation and subject to the guidance in ASC 718. See

SC 1.3 for further discussion on awards in the scope of

ASC 718 as well as

SC 2 and

SC 3 for measurement and classification considerations. For the arrangements not subject to

ASC 718, analysis under

ASC 815-40 is required.

These arrangements provide for multiple settlement alternatives. In total the arrangements could result in the issuance of 0, 100,000, 200,000, or 300,000 shares based on whether the VWAP exceeds targeted prices. In addition, the number of shares an individual holder may receive is also based on the continued employment of certain employees that were granted these arrangements. The number of shares an individual holder receives may increase based on the forfeiture of the arrangements granted to employees with unvested options. Since there could be a different number of shares issued depending on certain events, the arrangements would be analyzed under step two of the indexation guidance. For the purposes of this example, the application of step 1 of the indexation guidance is not illustrated.

In evaluating the arrangements under step two, the vesting/continued employment of certain employees is not an input into a “fixed-for-fixed” valuation model. As a result, the arrangements subject to

ASC 815-40 would be required to be classified as a liability and measured at fair value with changes in fair value recorded in current earnings.

Antidilution features

Settlement adjustments designed to protect a holder’s position from being diluted by a transaction initiated by an issuer will generally not prevent a freestanding instrument or embedded component from being considered indexed to the issuer’s own stock provided the adjustments are limited to the effect that the dilutive event has on the shares underlying the instrument. Common examples of adjustments that do not preclude a contract from being considered indexed to the issuer’s own stock include the occurrence of a stock split, rights offering, stock dividend, or a spinoff. In addition, settlement adjustments due to issuances of shares for an amount below current fair value, and repurchases of shares for an amount that exceeds the current fair value of those shares, do not preclude the contract from being considered indexed to the issuer’s own stock.

Not all “antidilution” settlement adjustments will meet the criteria for being considered indexed to a reporting entity’s own stock in

ASC 815-40-15. Settlement adjustments that overcompensate the holder (i.e., the potential adjustments exceed the potential impact of the dilution) prevent a freestanding instrument or embedded component from being considered indexed to the reporting entity’s own stock.

Down round features

Some equity-linked financial instruments may contain price protection provisions requiring a reduction in an instrument’s strike price as a result of a subsequent at-market issuance of shares below the instrument’s original strike price, or as a result of the subsequent issuance of another equity-linked instrument with a lower strike price. This is typically referred to as a “down round” feature. Down round features are most often found in warrants and conversion options embedded in debt or preferred equity instruments issued by private entities, but may also be found in financial instruments issued by public companies.

The issuance of shares for an amount equal to the current market price of those shares is not dilutive. Further, the possibility of a market price transaction occurring at a price below an instrument’s strike price is not an input to the valuation of a standard “fixed for fixed” instrument. The guidance in

ASC 815-10-15-75A effectively makes an exception with respect to down round features to the base model for determining when an instrument or an embedded feature is considered solely indexed to an entity’s own stock.

The term “down round” can be applied to provisions with varying terms. As such, a reporting entity should evaluate the specific provision to determine whether it affects the reporting entity’s ability to consider an instrument indexed to its own stock.

Adjustment provisions should be evaluated to determine whether they meet the definition of a down round.

The ASC Master Glossary provides the definition of a down round feature.

Definition from ASC Master Glossary

Down round feature: A feature in a financial instrument that reduces the strike price of an issued financial instrument if the issuer sells shares of its stock for an amount less than the currently stated strike price of the issued financial instrument or issues an equity-linked financial instrument with a strike price below the currently stated strike price of the issued financial instrument.

A down round feature may reduce the strike price of a financial instrument to the current issuance price, or the reduction may be limited by a floor or on the basis of a formula that results in a price that is at a discount to the original exercise price but above the new issuance price of the shares, or may reduce the strike price to below the current issuance price. A standard antidilution provision is not considered a down round feature.

As discussed in

ASC 815-10-15-75A, a reporting entity can disregard a down round feature that meets this definition when determining whether the instrument is considered indexed to the reporting entity’s own stock. However, when a down round feature is triggered, there are earnings per share implications for certain instruments, as discussed in

ASC 260-10-45-12B and

FSP 7.4.1.5A.

If a feature does not meet the definition of a down round, the instrument must be evaluated under the base model to determine whether it is solely indexed to an entity’s own stock.

Example FG 5-12A and Example FG 5-13A illustrate the evaluation of down round features.

EXAMPLE FG 5-12A

Strike price adjustment based on common stock valuation

Company A, a private company, issues a warrant for the purchase of 100,000 shares of Company A common stock, with a strike price of $10.00. The warrant provides for net settlement in shares and meets the definition of a derivative under

ASC 815. The terms of the warrant state that the strike price of the warrant will be reduced if a subsequent valuation indicates that the fair value of Company A’s common stock is below the current strike price. Historically, Company A has prepared a valuation when it issues instruments such as common stock, warrants, and convertible instruments, but it also has had valuations prepared when it issues equity-linked compensation to its employees.

Is the provision regarding the change in the warrant’s strike price a down round feature as defined in the guidance?

Analysis

While this feature is similar to a down round feature in that it is designed to protect warrant holders against declines in stock price, the provision does not meet the definition of a down round.

A down round feature contemplates a sale of a company’s stock or issuance of an equity-linked financial instrument. If Company A were to obtain or prepare a valuation of its common stock, this could trigger a reset of the instrument’s strike price, even if no instrument is issued by Company A. For example, Company A may be contemplating issuing equity to raise capital, but may decide to issue debt based upon the valuation of the common stock. Further, if Company A grants stock options to its employees with vesting requirements, they are not considered issued until they vest under GAAP.

In addition, if Company A were to issue warrants, convertible debt, or convertible preferred stock with a strike price higher than the strike price on the outstanding warrant, but the common stock valuation indicated a common stock price below the outstanding warrant strike price (i.e., Company A issued an out-of-the-money instrument), the strike price on the outstanding warrant would be adjusted downward. This would not be consistent with the definition of a down round, which indicates that the strike price on the outstanding warrant should only be adjusted if the strike price on the issued equity-linked instrument is below the outstanding warrant’s strike price.

EXAMPLE FG 5-13A

Adjustment to the number of shares

Company B issues a warrant for the purchase of 100,000 shares of Company B common stock, with a strike price of $10.00. The warrant provides for net settlement in shares and meets the definition of a derivative under

ASC 815. The terms of the warrant provide that when Company B sells common stock below the strike price on the warrant or issues a financial instrument with a strike price below the strike price on the warrant, the warrant will be exercisable into more than the initial 100,000 shares. The strike price of the warrant is not adjusted. This feature is designed to ensure that Company B receives a fixed amount of proceeds upon exercise of the warrant.

Is the provision to adjust the number of shares upon exercise of the warrant a down round feature?

Analysis

Although the definition of a down round refers only to a reduction in strike price, we believe that an increase in shares underlying the warrant can achieve the same economic objective. Therefore, we believe the provision could be considered a down round feature. As a result, it would not, in isolation, cause an instrument to not be considered indexed to an entity’s own stock. Increasing the number of shares an instrument is exercisable into is the only practical manner in which a down round can be implemented in a convertible instrument.

Although we believe that an increase in the number of shares underlying a warrant and reducing the strike price achieve the same economic objective, we believe that the increase in the number of shares pursuant to such a provision should not permit a transfer of more value to the holder than a reduction of a strike price would. For example, while the definition of a down round would permit the strike price of an instrument to be adjusted below the issuance or strike price of the issued instrument, the amount of value that could be transferred by a strike price reduction is limited as the strike price cannot be reduced below zero.