During the deliberations of

ASU 2018-12, the FASB received comments from insurance entities that applying the new guidance on a retrospective basis would be challenging given that many of the contracts were written decades ago. In an effort to alleviate these concerns, the default method for adoption of the provisions relating to the liability for future policy benefits is a modified retrospective approach. Under this approach, an insurer would “pivot” off, or carry over, the existing liability at the transition date.

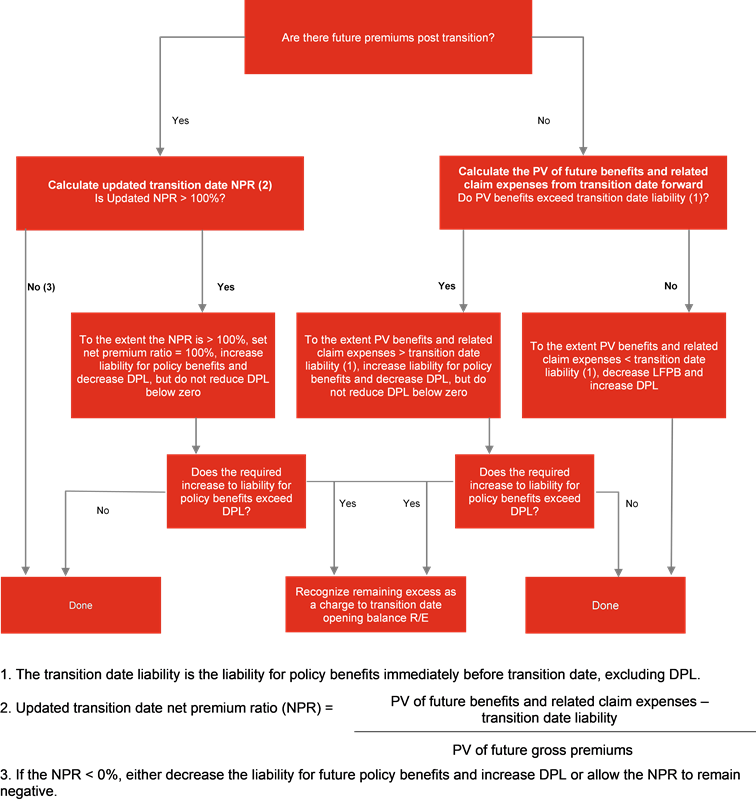

An insurer would apply the guidance to all in-force contracts at the transition date using the existing carrying amount of the liability, adjusted for the removal of any amounts in AOCI (e.g., any “shadow” premium deficiency liabilities recognized). Separately, after the net premium ratio is recalculated and any additional liability recognized relating to loss recognition, a balance sheet remeasurement will be required using the current upper-medium grade discount rate.

Figure IG 11-1 details how to “pivot” off the transition date balances for a traditional insurance contract.

Figure IG 11-1

Pivoting off of the balance at transition – traditional insurance contract

Start with the pre-adoption liability for future policy benefits (inclusive of any related premium deficiency). For a calendar year-end SEC filer (other than an SRC), this would be the balance at 12/31/20 (the transition date would be 1/1/21).

Step 1: Remove any previous AOCI adjustment

Step 2: Determine appropriate cohorts and their respective carrying amounts

Step 3: Allocate any existing premium deficiency to identified cohorts

Step 4: Calculate revised net premium ratio (using expected cash flows from transition date forward) for each cohort

Revised net premium ratio

|

|

Present value* of the updated future benefits and related claim expenses from transition date forward - carrying amount of the transition date liability (after removal of AOCI adjustment)

______________________________________________________________________

Present value* of the updated future gross premiums from transition date forward

|

|

*Present value is determined using the carryover locked-in interest rate assumption rather than the transition date upper-medium grade yield.

|

|

Step 5: If net premium ratio >100%, record loss for excess of net premiums over gross premiums as a debit to opening retained earnings (except that for limited-payment contracts, the deferred profit liability would first be reduced to zero).

Step 6: Remeasure liability using current single A discount rate and adjust AOCI (see Example IG 11-3).

At transition, the discount rate would not be reset for purposes of calculating the net premium ratio and future net premiums and interest accretion. As such, an insurer will continue to use the carryover locked-in interest rate assumption for determining benefit expense in current and future periods.

For existing traditional insurance contracts at transition, to the extent that the revised net premiums exceed revised gross premiums (i.e., a loss is expected), the liability for future policy benefits will be increased and the opening retained earnings balance would be decreased.

Existing liabilities will need to be divided into cohorts at transition that are subject to an annual cohort limitation. As such, it is possible that upon applying the annual cohort limitation to contracts that are currently grouped at a level above the annual cohort for premium deficiency purposes, a net premium ratio in excess of 100% could occur even though unamortized DAC is no longer included in the premium deficiency test. In this case, there would be a charge to opening retained earnings.

In periods subsequent to transition, in updating assumptions on a retrospective catch-up basis for contracts that were in force at transition, the transition date would be considered the revised contract issue date. For example, if an updated net level premium ratio was calculated in the fourth quarter of 2024 for business that was in force at an insurer’s January 1, 2021 transition date, the calculation would include historical benefit expense and gross premiums from 2021 through the date of the update, future benefits and gross premiums for 2025 and beyond, and total benefits would be reduced by the January 1, 2021 transition liability.

Question IG 11-1

When the net premium ratio at transition is greater than 100%, would the transition date carrying amount used subsequent to transition to recompute the net premium ratio be inclusive of the loss recognized at the transition date?

PwC response

No. For existing traditional insurance contracts at the transition date, when the updated present value of future benefits and related claim expenses less the transition date carrying amount exceeds the present value of future gross premiums, this results in a net premium ratio at transition greater than 100%, resulting in a loss for the cohort. In this situation, the liability for future policy benefits is increased and the opening retained earnings balance is decreased at the transition date. Additionally, the net premium ratio would be reset to 100% by including both the transition liability and the additional liability recognized at the transition date in the numerator of the net premium ratio until the next measurement date. However, that transition date increase in the liability for future policy benefits is not part of the transition date liability in subsequent updated calculations of the net premium ratio. See Example IG 11-1 for a numerical example.

Example IG 11-1 provides a numerical example of the accounting at transition and subsequently when the net premium ratio is greater than 100% at the transition date.

EXAMPLE IG 11-1

Net premium ratio exceeds 100% at transition

Insurer will adopt

ASU 2018-12 on January 1, 2023, with a transition date of January 1, 2021. For a given cohort at the transition date:

PV of future benefits and related claim adjustment expenses |

$210 |

|

PV of future gross premiums at the transition date |

$100 |

|

Transition date liability |

$102 |

|

How would Insurer calculate the net premium ratio at the transition date and subsequently when a loss is recognized at the transition date?

Analysis

At transition, in accordance with

ASC 944-40-65-2(d)(2), the present value of future benefits and related expenses less the transition date carrying amount would be compared to the present value of future gross premiums to calculate the updated net premium ratio.

NPR calculation at the transition date:

|

|

|

|

|

(PV of future benefits and related claim adjustment expenses

– transition date liability)

PV of future gross premiums

|

|

|

Because the net premium ratio is greater than 100%, Insurer would recognize a charge to retained earnings and an increase in the liability for future policy benefits for $8 million, the amount the numerator exceeds the denominator, bringing the total liability for future policy benefits at the transition date to $108 million. The net premium ratio would be reset to 100% by including both the $102 million transition liability and the additional $8 million in the numerator until assumptions are updated at the next measurement date.

NPR calculation at the transition date after recognizing additional liability:

|

|

|

|

|

(PV of future benefits and related claim adjustment expenses

– transition date liability – additional liability)

PV of future gross premiums

|

|

|

In calculating the updated net premium ratio in periods subsequent to transition, the numerator in the updated net premium ratio for this cohort would include the transition date liability of $102 million (i.e., the transition date liability remains $102 million; it is exclusive of any loss recognized at transition). To the extent the updated calculation resulted in an additional loss (i.e., the net premium ratio is above 108%), it would be immediately recognized in income, with an increase to the liability for future policy benefits. To the extent the updated calculation resulted in a loss less than originally expected (i.e., net premium ratio decreases from 108% but still remains above 100%), the liability for future policy benefits would be reduced and the reversal of the loss would be immediately recognized in income. If the net premium ratio decreases to an amount below 100%, the entire reversal of the additional liability recognized at transition would be immediately recognized in income, while the remaining benefit of the net premium ratio decrease would be recognized through the retrospective catch up adjustment in the current period and future periods’ revised margins.

Subsequent to the transition date:

|

|

|

Updated PV of future benefits and related claim adjustment expenses (historical and future) from the transition date forward

|

$205 |

|

PV of future gross premiums at the transition date

|

$100 |

|

Transition date liability

|

$102 |

|

In accordance with

ASC 944-40-65-2(d)(2), the present value of future benefits and related expenses less the transition date carrying amount would be compared to the present value of future gross premiums to calculate the updated net premium ratio:

NPR calculation subsequent to the transition date:

|

|

|

|

|

(Updated PV of future benefits and related claim adjustment expenses

– transition date liability)

PV of future gross premiums

|

|

|

The updated loss is $3 million rather than $8 million, resulting in a reduction in the liability for future policy benefits and an immediate credit to income of $5 million to reflect the updated estimate of the liability in the current period. The net premium ratio would be reset to 100% by including both the $102 million transition liability and the additional $3 million in the numerator until assumptions are updated at the next measurement date:

NPR calculation subsequent to the transition date after recognizing additional liability:

|

|

|

|

|

(Updated PV of future benefits and related claim adjustment expenses

– transition date liability – additional liability)

PV of future gross premiums

|

|

|

Question IG 11-2

Insurer adopts the new guidance for the liability for future policy benefits on a modified retrospective basis. If the “at inception” original assumptions (including the provision for adverse deviation) were more conservative than the new updated assumptions, the existing liability could be higher than the present value of the future benefits at the transition date, resulting in a negative net premium ratio.

How would this impact the calculation of the liability in future periods?

PwC response

The transition guidance requires an adjustment to the existing liability if future gross premiums are insufficient to cover future benefits. In this fact pattern, the existing liability is greater than what is ultimately needed. In future periods, the negative net premium ratio would be applied to gross premiums received, in effect creating a negative benefit expense that would reduce the liability over time to the amount needed for benefit payments.

Question IG 11-3

Under the modified retrospective transition approach, may an insurer change its methodology from using a single equivalent level investment yield rate to an investment yield curve (forward or spot) at the transition date? May it change from using an investment yield curve (forward or spot) to a single equivalent level investment yield rate?

PwC response

No, to both questions. As described in

ASC 944-40-65-2, the modified retrospective approach requires that for the purposes of calculating the net premium ratio and future net premiums and interest accretion, an insurance entity should retain the discount rate assumption that was used to calculate the liability immediately before the effective date. As such, an insurance entity will continue to use the carryover locked-in interest rate assumption (be it a single rate, a spot curve, or a forward curve) to determine the rate at which interest accretes throughout the expected lifetime of the cohorts. It may not change from a rate to a curve or a curve to a rate.

Question IG 11-4

Under the modified retrospective transition approach, how would an insurance entity determine the locked-in carryover discount rate (or curve) for a cohort comprised of individual policies each having different discount rates?

PwC response

Given that under existing guidance and employing a seriatum approach, the insurance entity previously had a single rate or a curve for each policy (i.e., prior locked-in investment yield rates), it must now determine the discount rate or curve that is appropriate for the cohort (i.e., the new group of policies). We believe that a reporting entity could determine the carry over locked-in investment yield discount rate (or curve) for the cohort by calculating a weighted average rate or curve for the cohort based on the previously locked-in rates or curves and expected cash flows at transition. Such rate or curve would be utilized for calculating the net premium ratio at transition and future net premiums and interest accretion relating to the liability for future policy benefits for the cohort. As noted in Question IG 5-7, in some instances an entity may instead deem it appropriate to use a discount rate or curve applicable for the issue date of each contract within the cohort.

Question IG 11-5The new guidance amended

ASC 944-40-30-15 to clarify that the expense assumptions used in estimating the liability for future policy benefits include termination and settlement costs, but exclude non-claim related costs such as policy maintenance costs. Prior to the adoption of the new guidance, some insurance entities may have included certain policy maintenance costs in the calculation of the present value of future policy benefits. How are policy maintenance costs previously included in estimating the liability for future policy benefits accounted for under the modified retrospective transition approach?

PwC response

Under the modified retrospective transition approach, the existing liability for future policy benefits at the transition date is carried over as of the transition date, adjusted for removal of any amounts in AOCI (i.e., any “shadow” premium deficiency liabilities recognized). There is no additional transition adjustment for the removal of previously included policy maintenance costs from the transition date liability for future policy benefits. However, for purposes of calculating the liability for future policy benefits at transition (and going forward), expected cash flows from the transition date forward exclude policy maintenance cost estimates. Maintenance costs after the transition date will be expensed as incurred.

Question IG 11-6The new guidance amended

ASC 944-40-30-7 to eliminate the requirement for a provision for adverse deviation (PAD) from the calculation of the present value of future policy benefits. How is the PAD previously utilized in estimating the liability for future policy benefits accounted for under the modified retrospective transition approach?

PwC response

Under the modified retrospective transition approach, the existing liability for future policy benefits at the transition date is carried over as of the transition date, adjusted for removal of any amounts in AOCI (i.e., any “shadow” premium deficiency liabilities recognized). There is no additional transition adjustment for the removal of the PAD from the transition date liability for future policy benefits. However, for purposes of calculating the liability for future policy benefits at transition (and going forward), expected cash flows from the transition date forward exclude any PADs, with the exception of any PADs applied to the discount rate.

In practice, some insurance entities apply a PAD to each individual assumption, including the discount rate (except for groups of contracts in premium deficiency). At transition, the discount rate is not reset for purposes of determining the benefit expense and for determining interest accretion on the liability balance subsequent to transition in accordance with

ASC 944-40-65-2(d)(1). As such, an insurance entity will continue to use the carryover locked-in interest rate assumption, inclusive of any PAD, for accreting interest on the liability and determining benefit expense in periods subsequent to transition for existing blocks of business at transition.

Question IG 11-7

Should insurance entities include claim liabilities in the liability for future policy benefits transition balance and expected cash flows relating to incurred claims in net premium ratio calculations?

PwC response

Yes, cash flows used to derive the net premium ratio should include all cash flows, including those for claim liabilities. Therefore, the liability for future policy benefits transition balance should include what was previously carried as a claim liability.

Question IG 11-8

How would an insurance entity determine the carryover discount rate for claim liabilities under the modified retrospective transition approach?

PwC response

The transition relief in

ASC 944-40-65-2(d)(1) extends to claim liabilities that are linked to the measurement of the net premium and liability for future policy benefits as of the transition date. The required transition may effectively be achieved by calculating a weighted average rate for the combined cash flows of the liability for future policy benefits and claim liability. As an alternative, an entity may retain the existing separate transition date discount rates when discounting future cash flows on claims incurred prior to the transition date. Claims reported after the transition date would, instead, be measured using the transition date liability for future policy benefits discount rate throughout the life of the contracts.

For business in-force at the transition date when the modified retrospective transition method is applied, subsequent to transition, presenting the claim liability separately or as part of the liability for future policy benefits should produce substantially similar results; differences could potentially arise depending on whether weighted discount rates or separate rates are used for the claim liability and liability for future policy benefits.