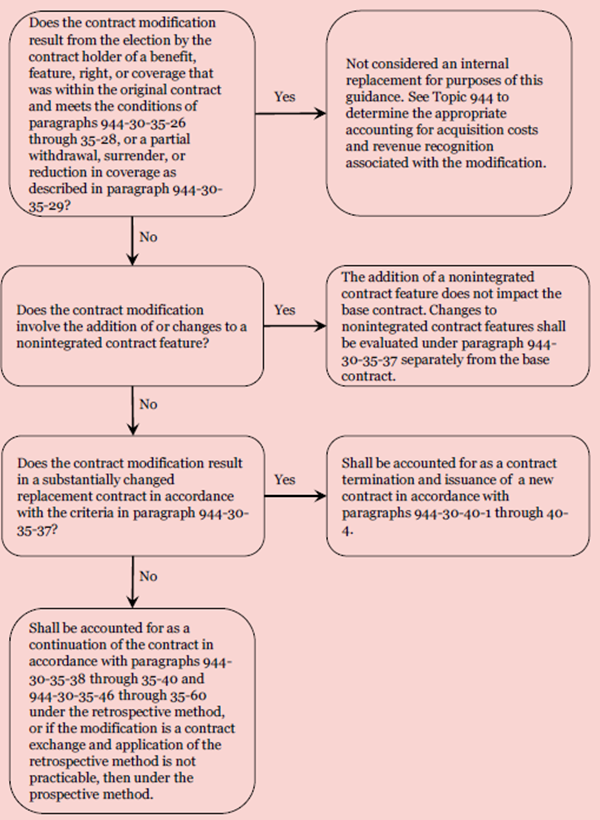

Internal replacements that do not meet the criteria established in

ASC 944-30-35-26 through

ASC 944-30-35-28 or

ASC 944-30-35-29 require further analysis. The next step in the analysis is to determine whether the internal replacement is a nonintegrated contract feature. If the internal replacement meets the definition of a nonintegrated feature, as defined in

ASC 944-30-35-30 and

ASC 944-30-35-31, it is not considered a substantial change in the original (base) contract, and no further analysis is required. The nonintegrated feature would be accounted for similar to a separately issued contract. Furthermore, as nonintegrated contract features, benefits, or coverages are more akin to separate contracts, any future modifications to such features are evaluated on a standalone basis (i.e., apart from the existing base contract). If the contract feature being modified is integrated, the transaction should be analyzed under

ASC 944-30-35-37 to determine if the original contract is substantially changed. See

IG 3.7.5 for further guidance on assessment of the internal replacement involving integrated contract features or coverages.

Figure IG 3-3 summarizes the definitions of integrated and nonintegrated features for short-duration and long-duration contracts.

Figure IG 3-3

Definitions of integrated and nonintegrated features for short-duration and long-duration contracts

Contract type |

Integrated |

Nonintegrated |

|

Contract features for which the benefits can only be determined in conjunction with the account value or other contract holder balances related to the base contract

|

Contract features for which the determination of benefits provided by the feature is not related to or dependent on the account value or other contract holder balances of the base contract

|

|

Contract features for which there is explicit or implicit re-underwriting or repricing of existing components of the base contract

|

Contract features that provide coverage that is underwritten and priced only for that incremental insurance coverage and do not result in the explicit or implicit re-underwriting or repricing of other components of the contract

|

Underwriting and pricing for nonintegrated features are typically executed separate from other components of the contract and theoretically could be purchased separately as an insurance contract, similar to a rider. In contrast, an integrated contract feature is one in which benefits provided by the feature can be determined only in conjunction with the account value or other balance relating to the base contract. However, the fact that the premiums to fund the additional or modified benefits are paid from the base contract’s value is not by itself an indication that the benefit feature is integrated.

In limited circumstances, it may not be clear if a contract feature is integrated or non-integrated, such as changes to the premium payment period of a life insurance contract from 10 years to 5 years, when the death benefit remains unchanged and the option was not part of the original contract provisions. As noted in TQA 6300.25, a contract feature is presumed to be integrated unless it clearly meets the definition of a non-integrated contract feature.

An example of an integrated contract feature for a short-duration contract is the addition of, or change to, an experience refund provision in a worker's compensation insurance contract.

Examples of integrated contract features for long-duration contracts include guaranteed minimum death benefits (GMDBs), guaranteed minimum income benefits (GMIBs), guaranteed minimum accumulation benefits (GMABs) and guaranteed minimum withdrawal benefits (GMWBs), as well as no lapse guarantees and secondary guarantees. These are integrated contract features because, in all cases, the benefit provided can only be determined in conjunction with the account value of the annuity contract.

Examples of nonintegrated contract features for short-duration contracts include a newly acquired automobile added to an existing personal automobile contract and a personal articles floater added to a homeowner's contract.

Examples of nonintegrated contract features for long-duration contracts may include a long-term care rider added to an annuity or disability contract, a term life rider added to an annuity contract, and an accidental death benefit feature added to a traditional life contract.

Waiver of premium benefits added to a traditional life contract is considered a nonintegrated modification. When added to a universal life type contract, waiver of premium could be integrated or nonintegrated, depending on the design of the benefits. A universal life waiver benefit that pays a fixed target premium would be considered nonintegrated but a similar benefit that pays cost of insurance (COI) charges would be considered integrated because the account balance is a factor in the determination of the COI charge.

Question IG 3-13

Do paid-up addition features (benefit allowing policyholders to use dividends to purchase additional increments of insurance) offered under certain participating life insurance meet the definition of an internal replacement? If so, are these features considered integrated or nonintegrated features?

PwC response

Paid-up addition features may in certain instances meet the conditions relating to contract holder elections as described in

ASC 944-30-35-26 and as such would not be considered internal replacements. See

IG 3.7.2 for additional information on the contract holder election criteria. However, in other instances, such paid-up additions may be considered internal replacements, but would generally meet the criteria to be considered a nonintegrated feature.

View image

View image