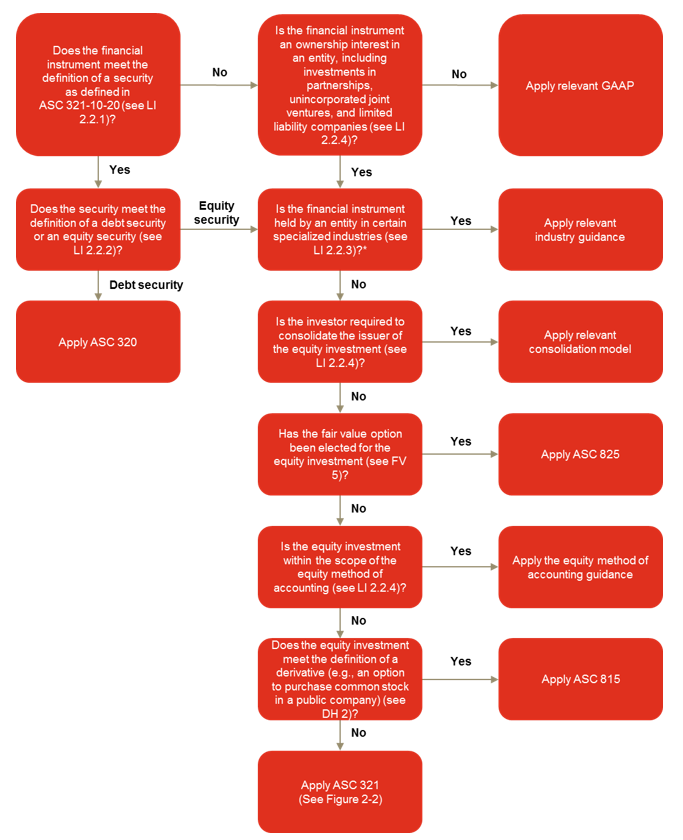

After a reporting entity determines that an equity interest meets the definition of a security, it should then determine whether the security meets the definition of an equity or debt security. The accounting for debt securities is discussed in

ASC 320,

Investments — Debt Securities and

LI 3.

Definition from ASC 321-10-20

Equity Security: Any security representing an ownership interest in an entity (for example, common, preferred, or other capital stock) or the right to acquire (for example, warrants, rights, forward purchase contracts and call options) or dispose of (for example, put options and forward sale contracts) an ownership interest in an entity at fixed or determinable prices. The term equity security does not include any of the following:

a. Written equity options (because they represent obligations of the writer, not investments)

b. Cash-settled options on equity securities or options on equity-based indexes (because those instruments do not represent ownership interests in an entity)

c. Convertible debt or preferred stock that by its terms either must be redeemed by the issuing entity or is redeemable at the option of the investor.

Securities that are legally equity interests may meet the definition of a debt security. For example, preferred stock that is mandatorily redeemable by the issuer or that can be redeemed at the option of the holder may be accounted for as a debt security. See

LI 3 for information on the accounting for investments in debt securities. The definition of an equity security also includes the right to acquire an ownership interest in an entity (e.g., warrants and forward purchase contracts) or dispose of an ownership interest in an entity (e.g., put options and forward sale contracts) at fixed or determinable prices. See

LI 2.2.4.1 for additional guidance.

Question LI 2-1 discusses whether an equity security issued by a mutual fund holding only US government debt should be accounted for as an equity security or a debt security.

Question LI 2-1

Should an equity security issued by a mutual fund holding only US government debt securities be accounted for as an equity security or a debt security?

PwC response

It is an equity security and is subject to the guidance in

ASC 321. As discussed in

ASC 320-10-55-8 and

ASC 321-10-55-6, an investor should not look through the form of its investment to the nature of the interests held by the investee to determine whether

ASC 320 or

ASC 321 applies.

If an equity interest meets the definition of a security, but not the definition of an equity security, it should assess whether the security meets the definition of a debt security. See

LI 3 for information on debt securities. Generally, we believe that the determination of whether a security meets the definition of a debt security or an equity security should be reassessed each reporting period.

Example LI 2-1, Example LI 2-2, and Example LI 2-3 discuss whether a contingently redeemable preferred stock investment should be classified as an equity security or a debt security.

EXAMPLE LI 2-1

Assessment of classification of a contingently redeemable preferred stock investment before continency has been resolved

On January 1, 20X1, a reporting entity purchases a preferred stock instrument with no maturity date. The preferred stock instrument has a contingent redemption feature such that if the issuer completes an initial public offering (“IPO”), the preferred stock instrument becomes redeemable at the investor’s option. If exercised, the redemption feature requires the issuer of the instrument to redeem the preferred stock for cash in an amount equal to its liquidation preference plus any unpaid dividends. Until such time that an IPO has been completed, the preferred stock instrument is not redeemable.

Should the reporting entity classify the preferred stock instrument as a debt or equity security at purchase?

Analysis

Upon purchase of the instrument, assuming an IPO has not yet been completed, the instrument should be considered an equity security and would be subject to the guidance in

ASC 321. The definition of an equity security under

ASC 321-10-20 states that preferred stock instruments that must be redeemed by the issuer or are redeemable at the investor’s option do not meet the definition of an equity security. While the preferred stock is contingently redeemable by the issuer, the redemption is only exercisable upon the successful completion of an IPO by the issuer, which is an event outside of the investor’s control. Upon purchase of the preferred stock, the instrument is neither mandatorily redeemable nor is it redeemable at the investor’s option. Therefore, the instrument would meet the definition of an equity security under

ASC 321-10-20, and the reporting entity should classify it as such.

EXAMPLE LI 2-2

Assessment of classification of a contingently redeemable preferred stock investment after contingency has been resolved

On January 1, 20X1, a reporting entity purchases a preferred stock instrument with no maturity date. The preferred stock instrument has a contingent redemption feature such that if the issuer completes an initial public offering, the preferred stock instrument becomes redeemable at the investor’s option. If exercised, the redemption feature requires the issuer of the instrument to redeem the preferred stock for cash in an amount equal to its liquidation preference plus any unpaid dividends. On December 1, 20X5, the issuer completes an IPO.

On December 31, 20X5, should the reporting entity classify the preferred stock instrument as a debt or equity security?

Analysis

Following the completion of the IPO by the issuer, the reporting entity should reclassify the instrument to account for it as a debt security under

ASC 320. Once the successful completion of the IPO has occurred, the redemption option is no longer contingently exercisable. The preferred stock instrument is now redeemable at any time at the reporting entity’s option.

ASC 320-10-20 states that the definition of a debt security includes preferred stock that is redeemable at the option of the investor. The preferred stock instrument in this example has become redeemable at the option of the investor and therefore meets the definition of a debt security. The reporting entity should account for the preferred stock under

ASC 320 as long as it has the right to redeem the security.

EXAMPLE LI 2-3

Assessment of classification of a redeemable preferred stock investment where the redemption option expires

On January 1, 20X1, a reporting entity purchases a newly issued preferred stock instrument with no maturity date. The preferred stock instrument becomes redeemable at the investor’s option five years after the issuance of the instrument (on January 1, 20X6). If exercised, the redemption feature requires the issuer of the instrument to redeem the preferred stock for cash in an amount equal to its liquidation preference plus any unpaid dividends. Once the preferred stock becomes redeemable, the investor has one year to exercise the redemption feature. After that one year, the preferred stock instrument is no longer redeemable (i.e., it is no longer redeemable as of January 2, 20X7).

On January 1, 20X1, should the reporting entity classify the preferred stock instrument as a debt or equity security? If the reporting entity still holds the instrument on January 2, 20X7 once the redemption option expires, should the reporting entity reassess the classification?

Analysis

The reporting entity should classify the preferred stock instrument as a debt security under

ASC 320 when purchased on January 1, 20X1. While the preferred stock is not yet redeemable, there is no contingent event outside of the investor’s control that would prevent the instrument from becoming redeemable. Since the preferred stock instrument becomes redeemable simply by the passage of time, the preferred stock would meet the definition of a debt security under

ASC 321-10-20.

If the reporting entity chooses not to exercise the redemption option when it becomes exercisable and the one-year exercise period passes, beginning on January 2, 20X7, the reporting entity should then reclassify the security to an equity security and account for it under

ASC 321. Once the exercise period has passed, the preferred stock instrument is no longer redeemable. Therefore, it no longer meets the definition of a debt security under

ASC 320-10-20 and now meets the definition of an equity security under

ASC 321-10-20.