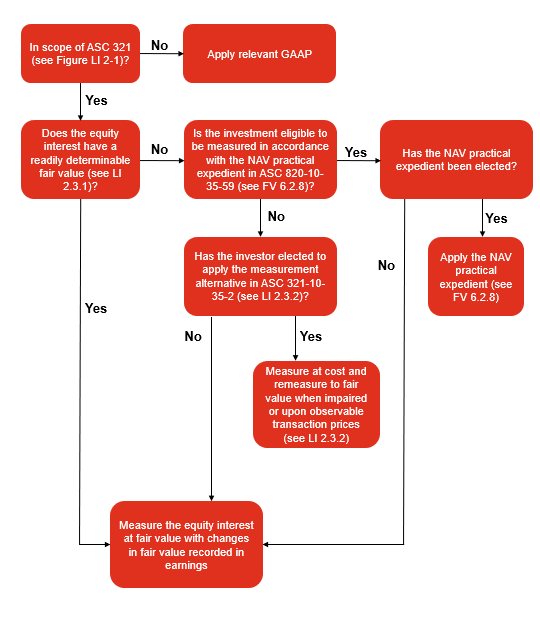

When a reporting entity elects the measurement alternative in

ASC 321, the equity interest is recorded at cost, less impairment. The carrying amount should be subsequently remeasured to its fair value in accordance with the provisions of

ASC 820 when observable price changes (i.e., observable prices in orderly transactions for an identical or similar investment of the same issuer) occur as of the date the transaction occurred or it is impaired. Any adjustments to the carrying amount are recorded in net income.

Question LI 2-8 discusses whether the costs to acquire an equity investment, that will be accounted for under the measurement alternative, can be capitalized as part of the carrying amount.

Question LI 2-8

Can the costs to acquire an equity investment that will be accounted for under the measurement alternative be capitalized as part of the carrying amount?

PwC response

ASC 321 does not address the initial measurement of equity investments accounted for under the measurement alternative. As a result, other applicable GAAP should be applied in determining the initial cost basis of the investment. However, it is explicit in

ASC 820 that transaction costs are not a characteristic of an asset or a liability; rather, they are specific to a transaction. Therefore, once an equity investment accounted for under the measurement alternative is remeasured to fair value based on an orderly transaction of the same or similar investment from the same issuer or due to an impairment, any transaction costs capitalized upon initial measurement would effectively be written off.

Orderly transactions

ASC 321-10-20

Orderly Transaction: A transaction that assumes exposure to the market for a period before the measurement date to allow for marketing activities that are usual and customary for transactions involving such assets or liabilities; it is not a forced transaction (for example, a forced liquidation or distress sale).

Observable transactions

ASC 321-10-55-8

To identify observable price changes, an entity should consider relevant transactions that occurred on or before the balance sheet date that are known or can be reasonably known. To identify price changes that can be reasonably known, the entity should make a reasonable effort (that is without expending undue cost and effort) to identify any observable transactions that it may not be readily aware of. The entity need not conduct an exhaustive search for all observable price changes.

Although companies are not expected to perform an exhaustive search to identify observable prices under this exception, companies should have the necessary processes and controls in place to identify observable price changes in accordance with the guidance.

Figure LI 2-3 shows examples of transactions and whether or not they would qualify as observable transactions/prices consistent with

ASC 321.

Figure LI 2-3Examples of observable transactions/prices consistent with

ASC 321

Transaction

|

Orderly and observable?

|

An investee entity issues the same or similar equity instrument to new or previously-existing equity owners in exchange for cash consideration.

|

Absent evidence that this is not an orderly transaction, the equity investment should be remeasured. A reporting entity should ensure that the remeasurement results in the investment being reported at fair value as defined by ASC 820. |

An existing investor sells the same or similar equity instrument from the same issuer to a new or existing investor for cash consideration.

|

Absent evidence that this is not an orderly transaction, the equity investment should be remeasured. A reporting entity should ensure that the remeasurement results in the investment being reported at fair value as defined by ASC 820. |

The equity investment of an investee is sold as part of a transaction between an existing investor and a new investor for cash. The transaction involves the sale of the same investment held by the reporting entity along with several other investments in other companies. The other investments have readily determinable fair values.

|

Absent evidence that this is not an orderly transaction, this transaction should be considered and the equity investment should be remeasured.

The observable price in this transaction would be calculated by subtracting the fair value of the other investments (which have readily determinable fair values) from the cash paid for the group of investments.

A reporting entity should ensure that the remeasurement results in the investment being reported at fair value as defined by ASC 820. |

The equity investments of an investee are sold as part of a transaction between an existing investor and a new investor for cash. The transaction involves the sale of the same investment held by the reporting entity along with several other investments. The other investments do not have readily determinable fair values.

|

This transaction, in isolation, would not be considered a remeasurement event unless it provided evidence of impairment.

Unlike the example above, the transaction involves other investments that do not have readily determinable fair values. The transaction price of the investment held by the reporting entity would not be observable without separate observable transactions/prices for the other investments.

|

Equity interests issued to employees as a form of compensation in exchange for services rendered as part of an approved long-term incentive compensation plan would not be considered an orderly transaction as it does not involve marketing activities that are usual and customary for sales of investments. In addition, it would likely not be considered an observable transaction/price because the value the reporting entity received in exchange for the equity instrument (the performance of services) is generally not observable. However, it may provide evidence of impairment.

Equity interests issued to non-employees may result in an observable transaction/price that would result in a remeasurement of the equity investment, or may provide evidence of impairment. The involvement of a third party could support a conclusion that the transaction is orderly but other factors may be considered, such as whether the price is considered observable. If the fair value of the services or goods exchanged are not readily determinable then it would be appropriate to conclude that this is not an observable transaction/price. However, it may provide evidence of impairment.

If the equity interest is remeasured or an impairment is recorded, the reporting entity should ensure that the remeasurement results in the investment being reported at fair value as defined by

ASC 820.

Question LI 2-9 discusses whether identifying an orderly transaction in the same investment or similar investment of the same issuer that occurred during a prior reporting period, but the transaction was not identified until after the issuance of the financial statements for that period, would be considered an error.

Question LI 2-9

Assume a reporting entity identifies an orderly transaction in the same investment or similar investment of the same issuer that occurred during a prior reporting period but the transaction was not identified until after the issuance of the financial statements for that reporting period. Would this be considered an error?

PwC response

A reporting entity should have processes and internal controls over identifying transactions. These processes and controls should continually be re-evaluated based on changes in market conditions and practices. If the reporting entity made a reasonable effort to search for observable transactions but did not identify the transaction, then the subsequent discovery of a pre-balance sheet date transaction would not constitute an error. The reporting entity should record an adjustment to the carrying value in the period in which the transaction is identified. If a reporting entity concludes that the transaction should have been identified in a previous reporting period because processes and controls were insufficient, this should be evaluated as an error under

ASC 250.

Question LI 2-10 and Question LI 2-11 discuss the accounting implications of identifying an orderly transaction in the same investment or similar investment of the same issuer after the balance sheet date but prior to the issuance of financial statements for that period.

Question LI 2-10

Assume a reporting entity identifies an orderly and observable transaction in the same investment or similar investment of the same issuer that occurred during the current reporting period, but the transaction is not identified until after the balance sheet date, yet prior to the financial statements being issued. Should the reporting entity adjust the carrying value of the equity interest to its fair value as of the date of the observable transaction in the financial statements that have not yet been issued?

PwC response

Yes, we believe a reporting entity should adjust the carrying value of that equity interest to its fair value because an orderly and observable transaction in the same or similar investment occurred prior to the balance sheet date and was identified before the financial statements were issued. ASC 321-10-35-2 states that a reporting entity should measure an equity interest at fair value as of the date the orderly transaction occurred. Since the orderly transaction occurred prior to the balance sheet date, the carrying value of that equity interest must be adjusted to reflect the remeasurement to fair value triggered by the observable transaction.

Question LI 2-11

Assume a reporting entity identifies an orderly and observable transaction in the same investment or similar investment of the same issuer that occurred after the balance sheet date but is identified prior to the financial statements being issued. Should the reporting entity adjust the carrying value of the equity interest to its fair value in the financial statements that have not yet been issued?

PwC response

ASC 321-10-35-2 states that the equity interest should be measured at fair value as of the date the orderly transaction occurs. As a result, the observable transaction would be a trigger to remeasure the equity investment to fair value in the subsequent reporting period.

However, an orderly transaction that occurs after the balance sheet date that indicates that the fair value of the equity interest is below the current carrying value could be an indication that an impairment existed as of the balance sheet date. If an impairment existed as of the balance sheet date, the reporting entity should measure the equity interest at its fair value as of the balance sheet date. Refer to

LI 2.3.2.5 for further discussion on the impairment of equity interests using the measurement alternative.

The reporting entity should consider disclosing the impact from remeasuring the instrument to fair value under the subsequent events guidance.

Similar investments

ASC 321-10-55-9 provides guidance on identifying similar investments of the same issuer.

ASC 321-10-55-9

To identify whether a security issued by the same issuer is similar to the equity security held by the entity, the entity should consider the different rights and obligations of the securities. Differences in rights and obligations could include characteristics such as voting rights, distributions rights and preferences, and conversion features. The entity should adjust the observable price of a similar security for the different rights and obligations to determine the amount that should be recorded as an upward or downward adjustment in the carrying value of the security measured in accordance with paragraph

321-10-35-2 to reflect the fair value of the security as of the date that the observable transaction for the similar security took place.

Application of the above guidance could be operationally challenging for reporting entities. In order to determine whether an equity interest issued by the same issuer is similar to an equity interest held by the reporting entity, a detailed understanding of the contractual terms of both equity interests must be obtained. Even in circumstances when differences in rights and obligations are readily apparent, determining whether two equity interests are similar is highly judgmental.

ASC 321 provides limited guidance on how to determine if an instrument is similar. To identify whether an instrument issued by the same issuer is similar to the equity instrument held by the reporting entity, the entity should consider if there are different rights and obligations of the investments, which may include differences in liquidation preferences, distribution/dividend rights, conversion features, or voting rights.

The reporting entity should consider, among other things, the following questions in evaluating whether the instruments are similar:

- Would differences in rights and obligations have a significant impact on the valuation of an instrument?

- Would the adjustment from the observable transaction price to reflect the differences in rights and obligations require significant use of unobservable data?

The determination of whether an instrument is similar should be based on a holistic analysis. Individual factors may not be determinative. For example, the adjustment to compensate for the differences between two instruments may involve significant use of unobservable data, but if the adjustment would have an insignificant impact on the fair value of the instrument, this may indicate that the instruments are similar. In other situations, the impact on fair value of an identified difference may be significant, but if it is easy to calculate and does not require significant use of unobservable data, this may also indicate the instruments are similar.

Conclusions on whether or not instruments are similar may change over time based on changes to the investee’s business and capital structure (e.g., a start-up versus an established company). Reporting entities should document the support of their conclusions.

Even if a reporting entity concludes that the observable transaction does not involve similar equity instruments, the transaction may be an indicator of impairment.

If a reporting entity concludes that the investments are similar, it should adjust the price of the similar investment as appropriate in order to arrive at a value that represents the fair value of the instrument held.