Search within this section

Select a section below and enter your search term, or to search all click Not-for-profit entities

Favorited Content

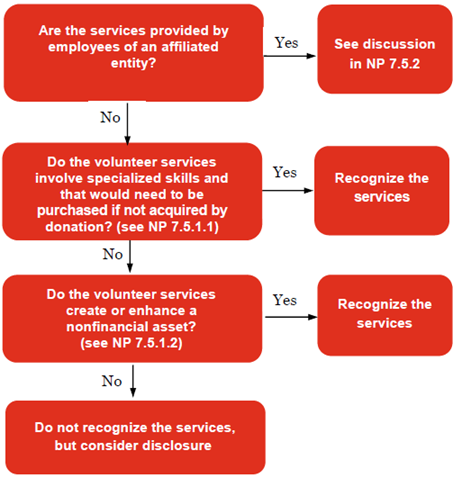

Excerpt from ASC 958-605-25-16

Contributions of services shall be recognized if the services meet any of the following criteria:

Dr. PP&E

|

$725,000

|

|

Cr. Contribution revenue

|

$325,000

|

|

Cr. Cash

|

$400,000

|

Dr. Compensation and benefits expense

|

$2,500,000

|

|

Cr. Contribution revenue

|

$2,500,000

|

An entity (NFPs and business entities) that receives contributed services shall describe the programs or activities for which those services were used, including the nature and extent of contributed services received for the period and the amount recognized as revenues for the period. Entities are encouraged to disclose the fair value of contributed services received but not recognized as revenues if that is practicable. The nature and extent of contributed services received can be described by nonmonetary information, such as the number and trends of donated hours received or service outputs provided by volunteer efforts, or other monetary information, such as the dollar amount of contributions raised by volunteers. Disclosure of contributed services is required regardless of whether the services received are recognized as revenue in the financial statements.

ASC Master Glossary

Affiliate

A party that, directly or indirectly through one or more intermediaries, controls, is controlled by, or is under common control with an entity.

The Services Received from Personnel of an Affiliate Subsections provide guidance for reporting services received by a not-for-profit entity (NFP) from personnel of an affiliate that directly benefit the recipient NFP and for which the affiliate does not charge the recipient NFP. Charging the recipient NFP means requiring payment from the recipient NFP at least for the approximate amount of the direct personnel costs (for example, compensation and any payroll-related fringe benefits) incurred by the affiliate in providing a service to the recipient NFP or the approximate fair value of that service.

The increase in net assets associated with services received from personnel of an affiliate that directly benefit the recipient not-for-profit (NFP) and for which the affiliate does not charge the recipient NFP shall be reported as an equity transfer, regardless of whether those services are received from personnel of an NFP affiliate or any other affiliate. The corresponding decrease in net assets or the creation or enhancement of an asset resulting from the use of services received from personnel of an affiliate shall be presented similar to how other such expenses or assets are presented. Paragraphs 954-220-45-2 through 45-3 provide additional guidance for not-for-profit, business-oriented health care entities.

ASC Master Glossary

Equity transfer

An equity transfer is nonreciprocal. An equity transfer is a transaction directly between a transferor and a transferee. Equity transfers are similar to ownership transactions between a for-profit parent and its owned subsidiary (for example, additional paid-in capital or dividends). However, equity transfers can occur only between related not-for-profit entities (NFPs) if one controls the other or both are under common control. An equity transfer embodies no expectation of repayment, nor does the transferor receive anything of immediate economic value (such as a financial interest or ownership).

Dr. Compensation and benefits expense

|

$100,000

|

|

Cr. Donated services received from affiliate

|

$100,000

|

|

To record administrative services performed by NFP personnel.

|

||

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Not-for-profit entities