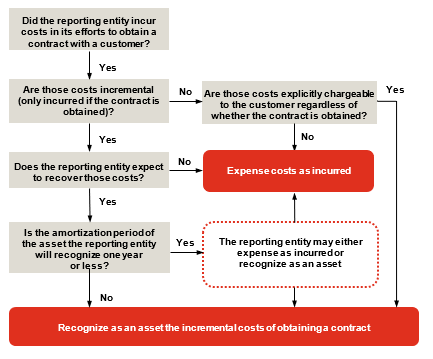

Figure RR 11-1 summarizes the accounting for incremental costs to obtain a contract.

Figure RR 11-1

Costs to obtain a contract overview

Example RR 11-1, Example RR 11-2, Example RR 11-3, Example RR 11-4, and Example RR 11-5 illustrate the accounting for incremental costs to obtain a contract. These concepts are also illustrated in Examples 36 and 37 of the revenue standard (

ASC 606-10-55-281 through

ASC 606-10-55-282).

EXAMPLE RR 11-1

Incremental costs of obtaining a contract — practical expedient

A salesperson for ProductCo earns a 5% commission on a contract that was signed in January. ProductCo will deliver the purchased products throughout the year. The contract is not expected to be renewed the following year. ProductCo expects to recover this cost.

How should ProductCo account for the commission?

Analysis

ProductCo can either recognize the commission payment as an asset or expense the cost as incurred under the practical expedient. The commission is a cost to obtain a contract that would not have been incurred had the contract not been obtained. Since ProductCo expects to recover this cost, it can recognize the cost as an asset and amortize it as revenue is recognized during the year. The commission payment can also be expensed as incurred because the amortization period of the asset is one year or less.

The practical expedient would not be available; however, if management expects the contract to be renewed such that products will be delivered over a period longer than one year, as the amortization period of the asset would also be longer than one year.

EXAMPLE RR 11-2

Incremental costs of obtaining a contract — construction industry

ConstructionCo incurs costs in connection with winning a successful bid on a contract to build a bridge. The costs were incurred during the proposal and contract negotiations, and include the initial bridge design.

How should ConstructionCo account for the costs?

Analysis

ConstructionCo should expense the costs incurred during the proposal and contract negotiations as incurred. The costs are not incremental because they would have been incurred even if the contract was not obtained. The costs incurred during contract negotiations could be recognized as an asset if they are explicitly chargeable to the customer regardless of whether the contract is obtained.

Even though the costs incurred for the initial design of the bridge are not incremental costs to obtain a contract, some of the costs might be costs to fulfill a contract and recognized as an asset under that guidance (refer to

RR 11.3).

EXAMPLE RR 11-3

Incremental costs of obtaining a contract — telecommunications industry

Telecom sells wireless mobile phone and other telecom service plans from a retail store. Sales agents employed at the store signed 120 customers to two-year service contracts in a particular month. Telecom pays its sales agents commissions for the sale of service contracts in addition to their salaries. Salaries paid to sales agents during the month were $12,000, and commissions paid were $2,400. The retail store also incurred $2,000 in advertising costs during the month.

How should Telecom account for the costs?

Analysis

The only costs that qualify as incremental costs of obtaining a contract are the commissions paid to the sales agents. The commissions are costs to obtain a contract that Telecom would not have incurred if it had not obtained the contracts. Telecom should record an asset for the costs, assuming they are recoverable.

All other costs are expensed as incurred. The sales agents’ salaries and the advertising expenses are expenses Telecom would have incurred whether or not it obtained the customer contracts.

EXAMPLE RR 11-4

Incremental costs of obtaining a contract — bonus based on a revenue target

TechCo’s vice president of sales receives a quarterly bonus based on meeting a specified revenue target that is established at the beginning of each quarter. TechCo’s revenue includes revenue from both new contracts initiated during the quarter and contracts entered into in prior quarters.

Is the bonus an incremental cost to obtain a contract?

Analysis

No. The revenue target is impacted by more than obtaining new contracts. As such, the payment would not be an incremental cost to obtain the contract.

If the revenue target was based on obtaining new contracts, the substance of the payment would be the same as a sales commission. If this were the case, the bonus might be an incremental cost.

EXAMPLE RR 11-5

Incremental costs of obtaining a contract — payment requires future service

Employee A, an internal salesperson employed by ProductCo, earns a 5% commission on a new contract obtained in January 20X1. The commission plan requires Employee A to continue providing employee service through the end of 20X2 to receive the commission payment.

Is the payment an incremental cost to obtain a contract?

Analysis

No. Employee A has to provide future service to receive the payment; therefore, the payment is contingent upon factors other than obtaining new contracts. ProductCo would recognize the expense over the service period in accordance with

ASC 710,

Compensation.