Set-up and mobilization costs are direct costs typically incurred at a contract’s inception to enable a reporting entity to fulfill its obligations under the contract. For example, outsourcing reporting entities often incur costs relating to the design, migration, and testing of data centers when preparing to provide service under a new contract. Set-up costs may include labor, overhead, or other specific costs. Some of these costs might be addressed under other standards, such as property, plant, and equipment. Management should first assess whether costs are addressed by other standards and if so, apply that guidance.

Mobilization costs are a type of set-up cost incurred to move equipment or resources to prepare to provide the goods or services in an arrangement. Costs incurred to move newly acquired equipment to its intended location could meet the definition of the cost of an asset under property, plant, and equipment guidance. Costs incurred subsequently to move equipment for a future contract that meet the criteria in

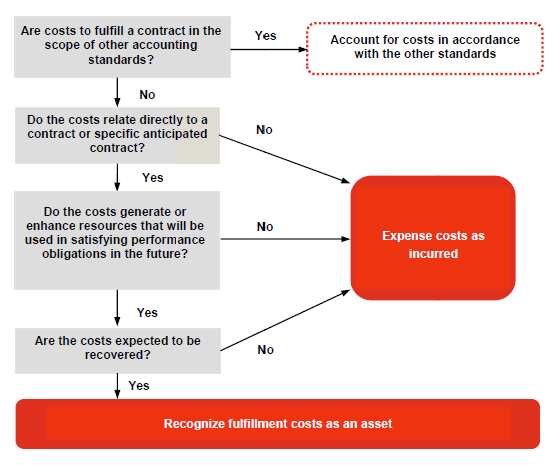

RR 11.3 are costs to fulfill a contract and therefore assessed to determine if they qualify to be recognized as an asset.

Certain pre-production costs related to long-term supply arrangements are addressed by specific guidance (that is,

ASC 340-10,

Other Assets and Deferred Costs—Overall). As such, costs in the scope of

ASC 340-10 should be assessed under that guidance to determine whether they should be capitalized or expensed. Management may need to apply judgment in assessing the guidance that applies to pre-production costs (for example,

ASC 340-10,

ASC 340-40,

Other Assets and Deferred Costs—Contracts With Customers, ASC 730,

Research and Development). Refer to

PPE 1.5.2 for a discussion of

ASC 340-10 and

RR 3.6.1 for further discussion of pre-production activities.

Example RR 11-6 illustrates the accounting for set-up costs. This concept is also illustrated in Example 37 of the revenue standard (

ASC 340-40-55-5 through

ASC 340-40-55-9).

EXAMPLE RR 11-6Set-up costs — technology industry

TechCo enters into a contract with a customer to track and monitor payment activities for a five-year period. A prepayment is required from the customer at contract inception. TechCo incurs costs at the outset of the contract consisting of uploading data and payment information from existing systems. The ongoing tracking and monitoring is automated after customer set up. There are no refund rights in the contract.

How should TechCo account for the set-up costs?

Analysis

TechCo should recognize the set-up costs incurred at the outset of the contract as an asset since they (1) relate directly to the contract, (2) enhance the resources of the company to perform under the contract, and relate to future performance, and (3) are expected to be recovered.

An asset would be recognized and amortized on a systematic basis consistent with the pattern of transfer of the tracking and monitoring services to the customer. The prepayment from the customer should be included in the transaction price and allocated to the performance obligations in the contract (that is, the tracking and monitoring services).