Search within this section

Select a section below and enter your search term, or to search all click Stock-based compensation

Favorited Content

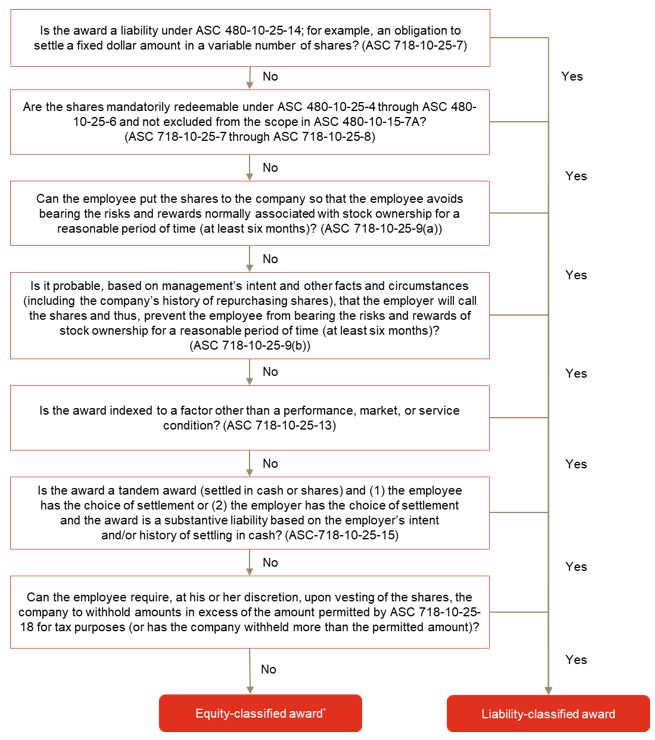

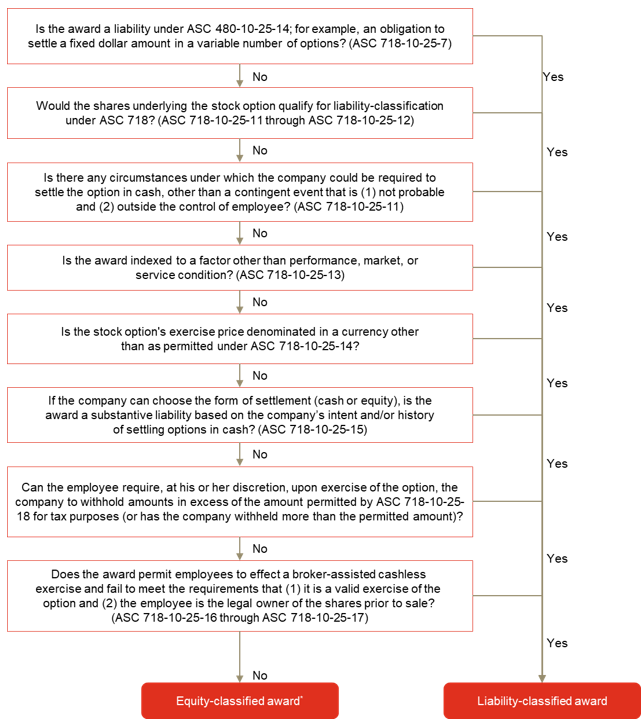

Instruments classified as liabilities |

Examples |

Mandatorily redeemable financial instruments

ASC 480 defines "mandatorily redeemable" as an unconditional obligation requiring the issuer to redeem the instrument by transferring its assets at a specified or determinable date (or dates) or upon an event that is certain to occur

|

|

Obligations to repurchase a company's equity shares by transferring assets

|

|

Certain obligations to issue a variable number of the company's shares

A financial instrument that meets both of the following conditions:

(1) the company must or could settle the obligation by issuing a variable number of its shares, and

(2) the obligation's monetary value is based solely or predominantly on any of the following factors at the obligation's inception:

|

|

Increase in EBITDA |

Dollar amount of award |

greater than 20% |

$1.0 million |

between 15% and 20% |

$0.8 million |

between 10% and 15% |

$0.5 million |

between 5% and 10% |

$0.2 million |

less than 5% |

$0 |

Increase in stock price |

Dollar amount of award |

greater than 20% |

$4 million |

between 15% and 20% |

$3.5 million |

between 10% and 15% |

$3 million |

between 5% and 10% |

$2.5 million |

less than 5% |

$0 |

Award |

Amount presented as temporary equity on the grant date |

Subsequent adjustments to temporary equity |

|

No amount is presented as temporary equity on the grant date because the option is unvested and has no grant-date intrinsic value.

|

Because it is probable that the underlying shares will become redeemable, the company should present the current intrinsic value at each reporting date as temporary equity as the option vests.

At the end of the first year, 25% of the intrinsic value, or $25,000, would be reclassified from permanent equity to temporary equity even though only $12,500 (25% of the option's grant-date fair value) has been credited to equity as compensation cost.

|

|

No amount is presented as temporary equity on the grant date because the option is unvested and has no grant-date intrinsic value.

|

The company will not present any amount as temporary equity until the change in control occurs, because the option had no intrinsic value on the grant date and it is not probable that the option will become redeemable. If it becomes probable that the options will be cash settled (i.e., the change in control occurs), the award would become a liability (accounted for as an equity-to-liability modification).

|

|

The intrinsic value of the option, or $30,000, is presented as temporary equity on the grant date because the option is vested and was granted in-the-money.

|

Because it is probable that the underlying shares will become redeemable, the company should continue to adjust the amount presented as temporary equity to the current intrinsic value at each reporting date.

At the end of the first year, an additional $70,000 would be reclassified from permanent equity to temporary equity, for a cumulative total of $100,000 presented as temporary equity, even though only $50,000 was credited to equity as compensation cost at the grant date fair value.

|

|

No amount is presented as temporary equity on the grant date because the restricted stock is unvested.

|

Over the vesting period, the company should present the grant-date fair value as temporary equity.

At the end of the first year, 25% of the grant-date fair value, or $37,500, would be reclassified from permanent equity to temporary equity.

Because it is not probable that the stock will become redeemable (change in control is not probable until it occurs), the company should not adjust the amount presented as temporary equity to the current intrinsic value (redemption amount, which also happens to be the fair value of the shares) at each reporting date.

If a change in control becomes probable and the put becomes active within six months of vesting, the award would become a liability under ASC 718 (accounted for as an equity-to-liability modification).

If a change in control becomes probable more than six months after the vesting date of the stock, the company should adjust the amount presented in temporary equity to the current fair value in each subsequent period as long as the put is active.

|

View image

View image

View image

View image

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Stock-based compensation