Search within this section

Select a section below and enter your search term, or to search all click Stock-based compensation

Favorited Content

Assumptions |

Impact on option's fair value as assumption/input increases |

Impact on option's fair value |

|

Less significant |

More significant |

||

Stock price |

Increase |

X |

|

Exercise price |

Decrease* |

X |

|

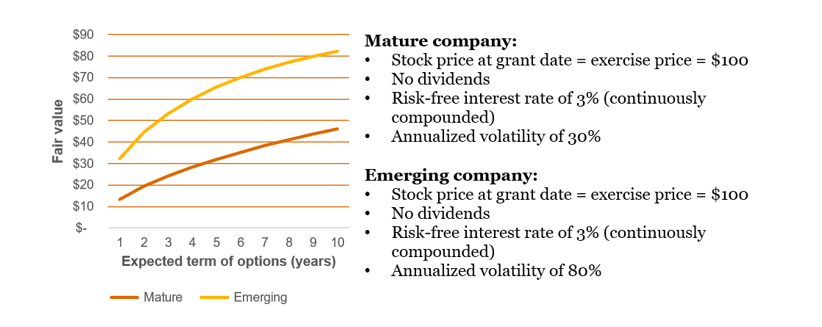

Expected term |

Increase |

X |

|

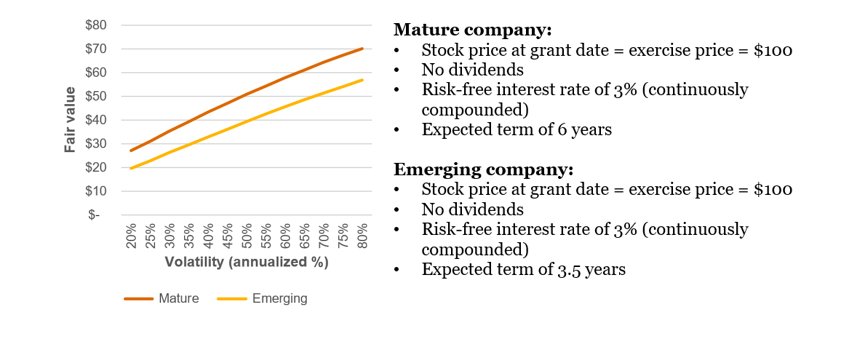

Expected volatility |

Increase |

X |

|

Expected dividend yield |

Decrease |

X** |

|

Risk-free interest rate |

Increase |

X |

|

* Assuming an at-the-money option, a higher exercise price (and stock price) would drive a higher option fair value, due to the higher time value component of the option value. For an in-the-money option, holding the stock price constant, the exercise price will have an inverse relationship on the intrinsic value of the option—i.e., a higher strike price would reduce the option's fair value.** For a large change in dividend yield (e.g., a change from 3% to 6%) this assumption can become more significant.

Minimum value computation: |

|

Current stock price |

$50.00 |

Less: |

|

|

41.76 |

|

2.90 |

Minimum value |

$5.34 |

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Stock-based compensation