The example in Figure SC 8-7 still assumes a single value for the expected term of the option rather than the more varied employee exercise behavior that would occur in reality, which may include the correlation between possible stock price appreciation and the expected time of exercise. However, the main reason to use a binomial model is to incorporate such assumptions over the option's contractual term. Because complex exercise pattern assumptions are not reflected in Figure SC 8-7, the estimates of fair value produced by the Black-Scholes model and the simplified binomial model will converge given a sufficient number of nodes.

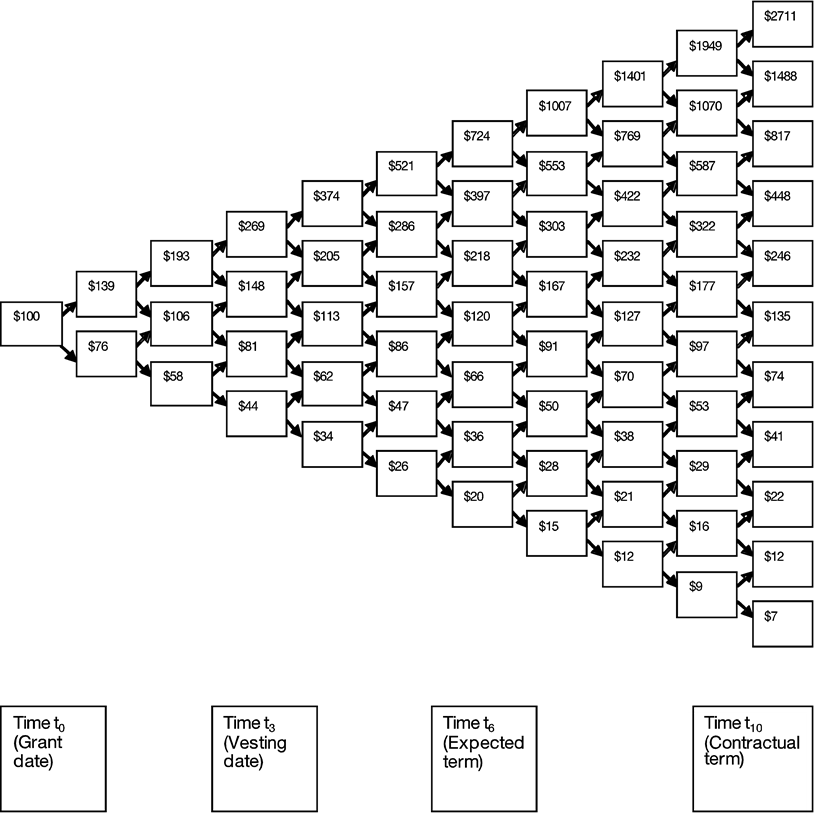

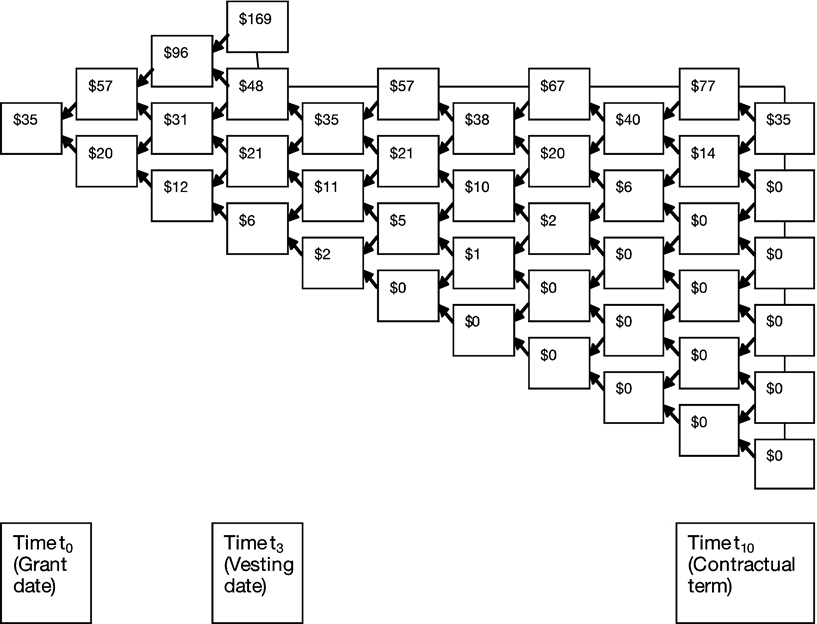

One method to incorporate early-exercise behavior assumes exercises based on stock price appreciation. As mentioned previously, a lattice model would simulate exercise behavior over the entire contractual term, rather than simply using the single average expected term as illustrated in Figure SC 8-7. Figure SC 8-8 shows another option valuation binomial tree-diagram, in which exercise is assumed to occur whenever the stock price reaches $200 (i.e., the stock to exercise price multiple of 2.0 is a "threshold" at which exercise is assumed to occur at a date prior to the end of the contractual term). The option value tree-diagram now covers the entire 10-year contractual life of the option instead of the six-year expected term as in Figure SC 8-7, since the option values must be simulated over the contractual life of the option in case the assumed exercise multiple is not reached. At time t10 (the end of the option's contractual life), the option is assumed to be exercised immediately if it has any intrinsic value at that point. If the stock price is less than the exercise price at time t10, the option expires worthless (i.e., the value is zero).

Figure SC 8-8

Option tree—ten-year contractual term with a 2.0 assumed exercise multiple

The values along the top boundary in Figure SC 8-8 will equal the option's intrinsic value (the greater of the stock price minus $100, or zero), similar to the values at time t6 in Figure SC 8-7. This boundary may be thought of as the "exercise frontier" (i.e., the points along the price-time continuum at which exercise is assumed to occur). As exercise is assumed to occur at these boundary points, no nodes above that line are necessary. The calculation proceeds "backwards" from the terminal values using risk-neutral probabilities and discounting for the time value of money. While the time-horizon imposed by the option's 10-year contractual life is reflected in this example, the constraint imposed by the three-year cliff vesting assumption has no effect because the highest potential stock-price at time t2 (the last node before vesting in our simple one step per year example) is $193, which is less than the assumed exercise threshold of $200. Refer to the corresponding node in Figure SC 8-6, which illustrates the potential stock prices; the values in Figure SC 8-8 above represent potential option-values.

The calculation shown in Figure SC 8-8 results in a fair value of approximately $42 or 17% higher than the approximately $36 fair-value (based on the static six-year expected term) from Figure SC 8-7. The use of an early-exercise assumption (i.e., the single average six-year expected term) will generally reduce the estimated fair value of an option as compared to a model that considers the full contractual life of ten years (on other than a dividend-paying stock, which can make it advantageous to exercise early in some circumstances). However, depending on where the assumed exercise multiple is set when exercise behavior is modeled based on stock-price appreciation, an option's fair value could be higher or lower than that of an otherwise similar option with an assumed static expected term.

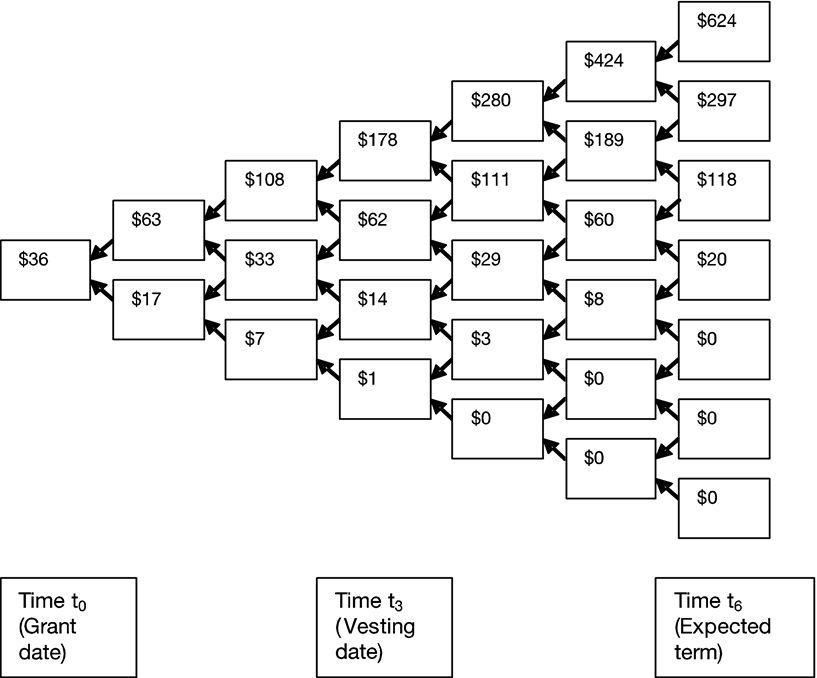

To explore the relationship between this type of early-exercise assumption and an option's fair value, Figure SC 8-9 presents another example, identical to the scenario presented in Figure SC 8-8, except that exercise is assumed to occur whenever the price of the underlying stock reaches $130 (i.e., when the assumed exercise multiple reaches 1.3).

Figure SC 8-9

Option tree—ten-year contractual term with a 1.3 assumed exercise multiple

The calculations in Figure SC 8-9 result in a fair value of approximately $27, 36% lower than the fair value of approximately $42, calculated in Figure SC 8-8 (using an assumed exercise multiple of 2.0). This dramatic decrease shows the sensitivity of fair value to the assumed exercise multiple—by essentially truncating the model for significantly more valuable payouts by using a lower exercise multiple, the fair value of the award is much lower. However, the calculation in Figure SC 8-9 may require further adjustment to reflect the terms and conditions of the award. Specifically, the exercise frontier shown in Figure SC 8-9 includes potential exercise scenarios as early as one year after grant (i.e., at a price of $139 at t1, as shown in Figure SC 8-6), which precedes the three-year cliff vesting date. Therefore, the unadjusted fair value calculation is based on assumptions that are inconsistent with the terms and conditions of the award and must be adjusted.

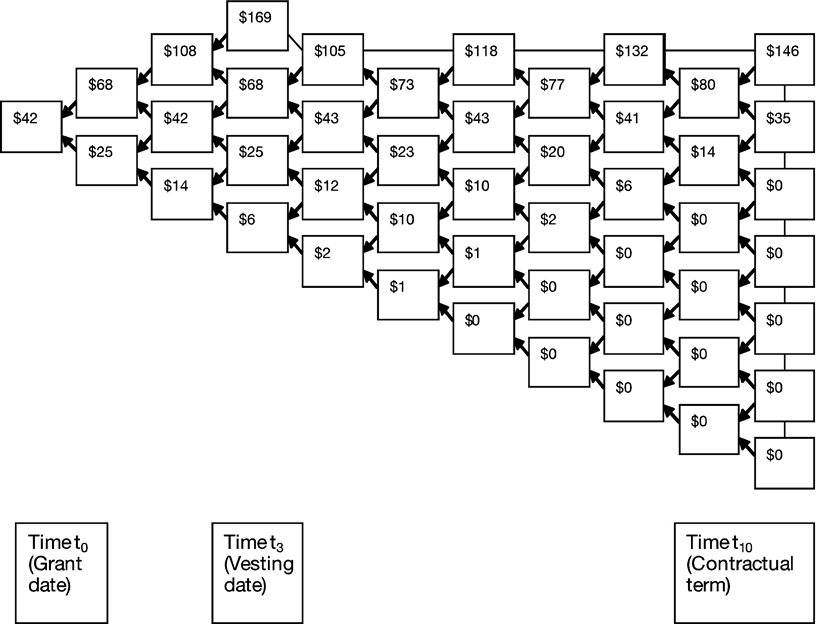

Figure SC 8-10 illustrates the adjusted calculation for the exercise multiple of 1.3 limited by the option's three-year vesting condition. This results in an exercise frontier with three segments—a vertical barrier at time t3, to reflect the vesting condition, a horizontal barrier from t3 to t10, to reflect the exercise multiple of 1.3, and another vertical barrier at t10, to reflect the contractual term of 10 years. If the stock price were to go to its highest possible node at the end of the second year (time t2), the option would be exercised at the end of the next year, because the stock price will be above $130, with intrinsic value greater than $30 ($130 stock price minus $100 strike price) regardless of whether the stock price moves up or down from time t2 to time t3. The resulting calculation moves the estimated fair value to $34.56 (rounded to $35), very near to its estimated fair value in the original binomial lattice using a six-year static expected term (approximately $35.88, rounded to $36 in Figure SC 8-7).

Figure SC 8-10

Option tree—ten-year contractual term with a 1.3 assumed exercise multiple limited by the three-year cliff-vesting condition

The results of the calculations in Figure SC 8-8, Figure SC 8-9 and Figure SC 8-10 are affected by the use of one-year time-steps in the lattice model. These time-steps are intended to illustrate the workings of the model. As noted earlier, a more realistic model would use shorter time intervals (e.g., daily) resulting in significantly more nodes. The model in Figure SC 8-7 with one-year time steps resulted in a valuation fairly close to the Black-Scholes value using a simple six-year expected term. In contrast, for the exercise assumptions in Figure SC 8-8, Figure SC 8-9 and Figure SC 8-10, a lattice model with smaller time intervals could produce values that differ by as much as 20% from those shown above. This is because the lattice values with the longer intervals may yield a stock price that well-exceeds an assumed exercise threshold in a single step when the option would theoretically be exercised at a lower price when shorter intervals are used. The values shown in the figures above are rough approximations illustrating the general relationship between results and model inputs with three-year cliff vesting and stock price volatility of 30%, as well as the exact calculations on a simplified basis (note the relationships will vary with different vesting schedules and volatility assumptions).

The examples shown above depict a constant exercise-frontier (except as affected by vesting or expiration of an option). In a more elaborate binomial model, the assumed early-exercise frontier may have a different slope or may be a probability distribution curve, rather than a straight line, that varies with both the price of the underlying stock and time. The binomial model can also incorporate additional assumptions regarding post-vesting cancellations, as discussed in

SC 9.3.3.

For complex binomial models that reflect the correlation of stock price and early exercise, software applications may be employed to perform such modeling. As discussed further in

SC 9.1, developing these models and the underlying assumptions manually will require considerable time and effort.

The lattice model also may be used to develop an implied expected term assumption, which is a required disclosure under

ASC 718. The analysis of exercise patterns in a lattice model may yield an expected term that is shorter (or longer) than the expected term used in an otherwise similar Black-Scholes model. There are several methods to infer a single expected term from a lattice model, such as the method included in

ASC 718-10-55-30, which solves for an implied expected term in the Black-Scholes model such that the Black-Scholes model's fair value equals the lattice model's fair value. Using this method, with an assumed exercise multiple of 2.0, the expected term assumption inferred in Figure SC 8-8 is approximately 8.2 years. Using the risk-neutral expected life method, the inferred expected term assumption is approximately 8.3 years. For typical options, the theoretical, inferred, risk-neutral expected term is much longer than the more realistic, and easily interpreted, implied Black-Scholes expected term.

There is a third method that would involve using a risk-adjusted expected rate of return in conjunction with early exercise assumptions built into the lattice model. The expected term assumption disclosed for companies using lattice models will therefore vary based upon the method used to infer it. The method used to infer the expected term should be applied consistently.