Search within this section

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets

Favorited Content

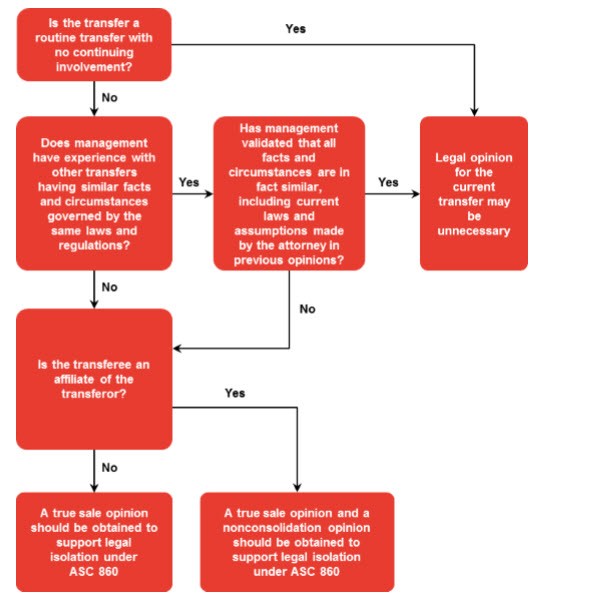

The transferred financial assets have been isolated from the transferor—put presumptively beyond the reach of the transferor and its creditors, even in bankruptcy or other receivership. Transferred financial assets are isolated in bankruptcy or other receivership only if the transferred financial assets would be beyond the reach of the powers of a bankruptcy trustee or other receiver for the transferor or any of its consolidated affiliates included in the financial statements being presented. For multiple step transfers, a bankruptcy-remote entity is not considered a consolidated affiliate for purposes of performing the isolation analysis. Notwithstanding the isolation analysis, each entity involved in the transfer is subject to the applicable guidance on whether it shall be consolidated (see paragraphs 860-10-40-7 through 40-14 and the guidance beginning in paragraph 860-10-55-18). A set-off right is not an impediment to meeting the isolation condition.

Definition from ASC 860-10-20

Consolidated Affiliate: An entity whose assets and liabilities are included in the consolidated, combined, or other financial statements being presented.

Excerpt from AU 9336.14

"We believe (or it is our opinion) that in a properly presented and argued case, as a legal matter, in the event the Seller were to become subject to receivership or conservatorship, the transfer of the Financial Assets from the Seller to the Purchaser would be considered to be a sale (or a true sale) of the Financial Assets from the Seller to the Purchaser and not a loan and, accordingly, the Financial Assets and the proceeds thereof transferred to the Purchaser by the Seller in accordance with the Purchase Agreement would not be deemed to be property of, or subject to repudiation, reclamation, recovery, or recharacterization by, the receiver or conservator appointed with respect to the Seller."

Excerpt from AU 9336.14

"Based upon the assumptions of fact and the discussion set forth above, and on a reasoned analysis of analogous case law, we are of the opinion that in a properly presented and argued case, as a legal matter, in a receivership, conservatorship, or liquidation proceeding in respect of the Seller, a court would not grant an order consolidating the assets and liabilities of the Purchaser with those of the Seller."

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets