3.6 Transferee’s right to pledge or exchange transferred financial assets

Publication date: 31 May 2024

us Transfers of financial assets guide

The second criterion that must be met for a transaction to qualify for sale accounting requires the transferee to obtain the right to freely pledge or exchange the transferred assets.

This condition is met if both of the following conditions are met:

Each transferee (or, if the transferee is an entity whose sole purpose is to engage in securitization or asset-backed financing activities and that entity is constrained from pledging or exchanging the assets it receives, each third-party holder of its beneficial interests) has the right to pledge or exchange the assets (or beneficial interests) it received.

No condition does both of the following:

Constrains the transferee (or third-party holder of its beneficial interests) from taking advantage of its right to pledge or exchange

Provides more than a trivial benefit to the transferor (see paragraphs 860-10-40-15 through 40-21).

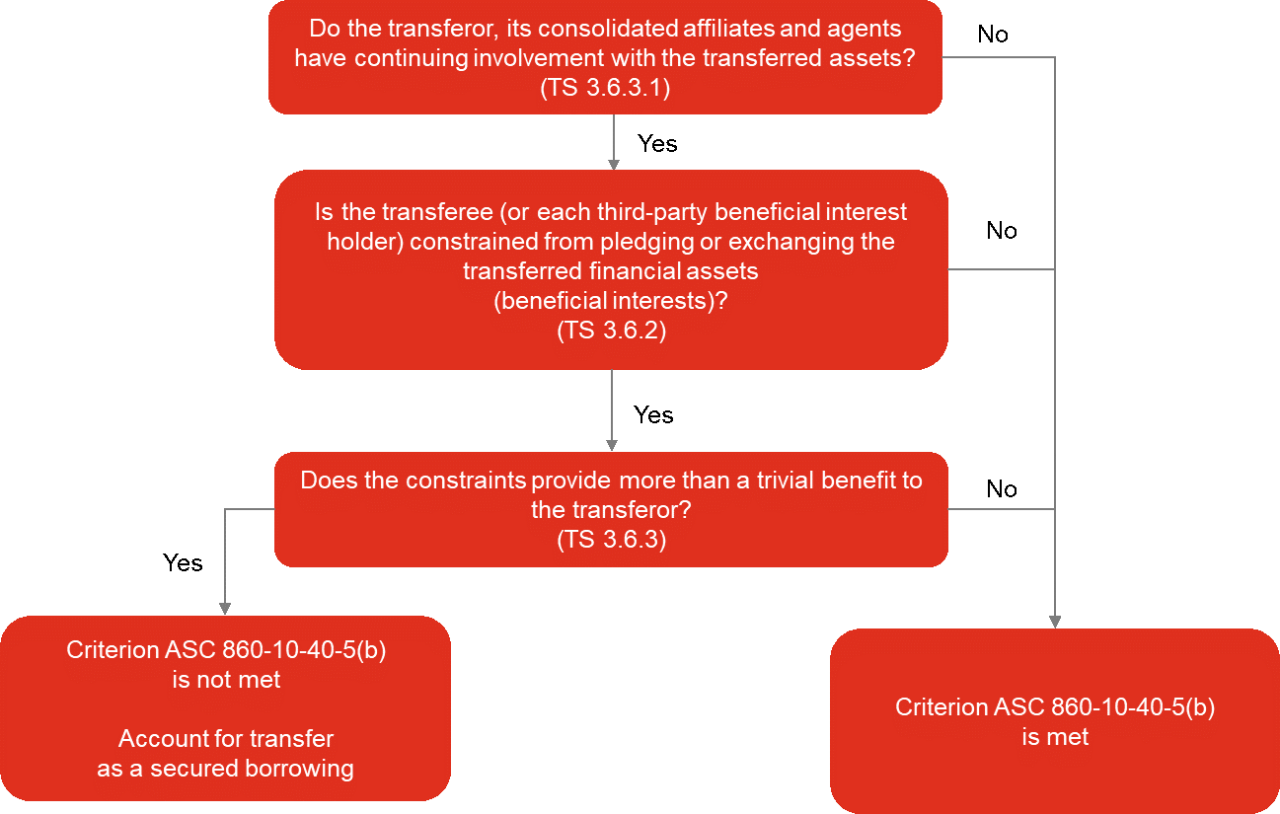

If the transferor, its consolidated affiliates included in the financial statements being presented, and its agents have no continuing involvement with the transferred financial assets, the condition under paragraph 860-10-40-5(b) is met.

Upon completion of a transfer, the transferor and transferee must determine whether, in fact, the transferee (or, if the transferee is an entity whose sole purpose is to engage in securitization or asset-backed financing activities and that entity is constrained from pledging or exchanging the assets it receives, each third-party holder of its beneficial interests) is able to freely pledge or exchange the assets (or beneficial interests). If the transferee (or holder) is not constrained from doing so, then the criterion is met. Conversely, if the transferee (or holder) is constrained by the transferor, a consolidated affiliate, or an unaffiliated agent, and that constraint provides more than a trivial benefit to the transferor, sale treatment for the transfer would be precluded.

3.6.1 Unit of account: the beneficial interest "look-through" accommodation

If the transferee entity’s sole purpose is to engage in securitization or asset-backed financing activities, the sale accounting analysis considers the ability of the transferee’s third-party beneficial interest holders to pledge or exchange their interests. This ability to "look through" the transferee entity acknowledges that securitization trusts and similar asset-backed financing entities must pledge the acquired financial assets coincident with their acquisition to protect the interests of the transferee’s beneficial interest holders and, in addition, may not freely dispose of or sell the assets while those interests remain outstanding. In these circumstances, the beneficial interests held by third-party investors are considered surrogates for the transferred assets themselves, and thus those beneficial interests serve as the "unit of account" or point of reference when applying ASC 860-10-40-5(b).

Although the look through guidance in ASC 860-10-40-5(b) is written in the context of "each third-party holder of [the transferee’s] beneficial interests," we do not believe the guidance is intended to imply that a third party beneficial interest holder must exist. For example, we believe that a transfer of financial assets to a guaranteed mortgage securitization entity, whereby the transferor retains all of the securities issued, may still meet this criterion. Further, it is our understanding that the reference to "each third-party holder" was intended to allow potential transfers in which the transferor is required to hold a certain amount of securities/beneficial interests (and is precluded from pledging or exchanging them) to achieve sale accounting, provided that the third-party holders, if any, could pledge or exchange their interests.

Depending on the facts and circumstances, an entity that arguably constitutes a securitization or an asset-backed financing entity will not qualify for ASC 860-10-40-5(b)'s look through accommodation. Example TS 3-3 illustrates this concept.

EXAMPLE TS 3-3 Evaluation of whether an asset-backed financing entity qualifies for the beneficial interest "look through" approach in ASC 860-10-40-5(b)

Transferor Co originates and periodically transfers loans to Warehousing Co, an unconsolidated LLC created specifically to acquire Transferor Co’s loans. A substantial portion of Warehousing Co’s financing consists of a credit line provided by Big Bank. In exchange for extending credit, Big Bank has a security interest in Warehousing Co’s loans, and thus Warehousing Co may not re-pledge them. Big Bank may look only to the loan collateral for repayment. The loan agreement further provides that, in the event Warehousing Co subsequently sells the loans, the proceeds must first be used to repay Big Bank’s loan. However, the loan agreement does not restrict Warehousing Co from selling the loan collateral to third parties and, similarly, there are no provisions in the LLC agreement that constrain Warehousing Co from doing so.

In connection with its assessment of the condition in ASC 860-10-40-5(b), should Transferor Co consider Warehousing Co to be an asset-backed financing entity constrained from pledging or exchanging the loans acquired from Transferor Co?

Analysis

No. To qualify for the "look through" test in ASC 860-10-40-5(b), a transferee must satisfy two conditions, namely (1) it engages solely in securitization or asset-backed financing activities, and (2) it is constrained from pledging or exchanging the assets received. Although Warehousing Co may be considered to meet the first condition, it does not satisfy the second. Given Big Bank’s security interest in the loans, Warehousing Co cannot re-pledge them. However, the loan agreement does not constrain Warehousing Co from exchanging (selling) the loans. Although the proceeds from any such sales must be used first to repay any indebtedness to Big Bank, that provision does not constrain Warehousing Co from converting the loans into cash (i.e., monetizing the loans).

Consequently, when assessing whether Warehousing Co meets the sale accounting requirement in ASC 860-10-40-5(b), the unit of account should be the transferred loans themselves – not the interests issued by Warehousing Co.

3.6.2 Constraints on pledging or exchanging financial assets or beneficial interests

Under ASC 860, determining whether a transferor has surrendered control over transferred financial assets involves, among other things, evaluating whether transferee (or, if applicable, a holder of a beneficial interest in those assets) has the ability to obtain all or most of the cash inflows from those assets (or beneficial interests), either by exchanging them or pledging them as collateral. This evaluation focuses on the owner’s ability to obtain all or most of the cash inflows, which is the primary economic benefit of a financial asset (or beneficial interest). It does not matter what method is used to accomplishing this end (i.e., by exchanging it or pledging it as collateral).

Constraints on a transferee’s (or holder’s) contractual right to pledge or exchange transferred financial assets may be explicitly imposed by provisions in the transfer agreement, or in other contemporaneous agreements. As observed in ASC 860-10-40-16, a condition imposed by a transferor that constrains a transferee is presumed to provide the transferor with more than a trivial benefit – in which case the condition in ASC 860-10-40-5(b) would not be satisfied.

However, in other cases, the constraints may stem from facts and circumstances unrelated to the transfer and related agreements. Examples include regulatory constraints (e.g., regulations that allow only qualified parties to acquire particular assets) or market conditions (e.g., limited investor appetite for the financial asset in question). Constraints or conditions of this type are presumptively not considered to constrain a transferee for purposes of the sale accounting analysis.

ASC 860-10-40-17 cites various conditions that both constrain the transferee and presumptively provide more than a trivial benefit to the transferor. Examples include:

Prohibition on the transferee’s subsequent sale or pledge of the financial assets

Transferor-imposed constraints that narrowly limit the timing or terms of any subsequent pledge or exchange (e.g., allowing a transferee to pledge assets only on the first day, or allowing the transferee to sell assets only on terms agreed with the transferor)

Right of transferor approval before any asset may be transferred by the transferee (unless contractually such approval cannot be unreasonably withheld)

Prohibition on the sale of the financial assets by the transferee to a competitor of the transferor, if that competitor is the only potential willing buyer of the transferred asset

Call option written by a transferee to the transferor on transferred assets not readily obtainable (this constrains a transferee because it might default if the call is exercised and it has previously exchanged or pledged the assets)

On the other hand, ASC 860-10-40-18 lists examples of conditions relating to transferred financial assets that presumptively would not, in isolation, preclude sales treatment under ASC 860-10-40-5(b):

A transferor’s right of first refusal on the occurrence of a bona fide offer to the transferee from a third party…

A requirement to obtain the transferor’s permission to sell or pledge that is not to be unreasonably withheld

A prohibition on sale to the transferor’s competitor if other potential willing buyers exist

A regulatory limitation such as on the number or nature of eligible transferees (as in the circumstance of securities issued under Securities Act Rule 144A or debt placed privately)

Illiquidity, for example, the absence of an active market

Certain economic constraints, such as a transferee (or holder of a beneficial interest) incurring significant tax liability upon sale of the asset, are not considered to preclude sale treatment. These types of constraints are beyond the control of the transferor.

Question TS 3-3, Question TS 3-4, Question TS 3-5, and Question TS 3-6 illustrate specific aspects of the guidance.

Question TS 3-3 How do restrictions on the sale of transferred assets to several competitors, rather than a single competitor, impact the analysis under ASC 860-10-40-5(b)?

PwC response

As long as there are other potential buyers, a provision that prohibits the transferee from selling a transferred financial asset to a single competitor would not violate the "ability to pledge or exchange" condition. Similarly, restrictions on sales to several competitors would not be problematic if, exclusive of those competitors, the universe of potential buyers is consequential. The determination of "consequential" in this context is a matter of judgment and should be based on the specific facts and circumstances.

Question TS 3-4 ASC 860-10-40-18(b) refers to a transferor’s permission to sell or pledge "that is not to be unreasonably withheld." Under what circumstances could this language be considered to constrain the transferee from pledging or constraining the transferred financial asset?

PwC response

ASC 860-10-40-18(b) presumes that a requirement to obtain permission to sell or pledge that may not be unreasonably withheld does not call into question the transferee’s right to pledge or exchange the acquired financial asset. However, before concluding, a reporting entity should consider why this restriction was imposed. A condition to obtain the transferor’s permission may be imposed by a transferor for business or competitive purposes. For example, if a transferor’s refusal to approve a proposed sale of a transferred financial asset to a competitor could be upheld under their discretionary right to consent – and all potential buyers of the asset in question are competitors of the transferor – then the consent right would likely be considered constraining. In practice, we would expect situations like this to be rare. Nevertheless, if uncertainty exists regarding the scope and nature of a potentially constraining consent right, advice of legal counsel may be warranted.

Question TS 3-5 Assume a transferee does not have the ability to pledge acquired loans, nor can the transferee sell the loans in their entirety to third parties. That is, the transferee may not transfer legal title to any acquired loan to a buyer. However, the transferee has an unconstrained right to sell participation interests in the loans (ownership interests in the loans’ cash flows). In view of this participation right, does the transferee meets the condition in ASC 860-10-40-5(b)?

PwC response

Potentially, yes. To conclude that the test in ASC 860-10-40-5(b) may be considered met in the circumstances described above, two conditions must be satisfied:

The transferee must have the unilateral contractual right (either explicit or implicit) to transfer participation interests in the loans that allow it to monetize substantially all (i.e., 90% or more) of the cash flows from the loans

There are no other provisions in the transaction agreements (or other facts and circumstances regarding the transferee or the characteristics of the transferred assets) that call into question whether the contractual right to sell participations is, in fact, substantive.

If these conditions are met, we believe a transferee’s right to sell participations in transferred financial assets may be sufficient, in and of itself, to conclude that the transferee has the right to freely exchange those assets. The requirement in ASC 860-10-40-5(b) focuses on a transferee’s ability to obtain all or most of the financial asset’s cash inflows, not on the legal form of that ability (by pledging or exchanging the asset). We do not believe that a conclusion that a transferee has the ability to exchange a transferred financial asset requires a contractual right to convey legal title to another party. A transferee can potentially monetize all the cash inflows of a financial asset (e.g., a debt instrument or equity security) by selling participation (ownership) interests that collectively entitle the participants to 100% of the asset’s cash inflows, and at the same time remain the legal owner of the financial asset.

Question TS 3-6 Assume a transferee can only pledge an acquired debt instrument and any such pledge must be on a full-recourse basis. The transferee owns other unencumbered assets that may be pledged to secure financing, along with the acquired asset. This asset base permits the transferee to obtain financing substantially in excess of the fair value of the debt instrument. Based on these facts and circumstances alone, can the transferor assert that the condition in ASC 860-10-40-5(b) is satisfied regarding the transferred debt instrument?

PwC response

No. Additional analysis is required. ASC 860-10-55-27 affirms that the condition in ASC 860-10-40-5(b) may be met even in instances when a transferee can only pledge transferred financial assets, albeit conditional on a careful analysis of the facts and circumstances.

To conclude that the requirement in ASC 860-10-40-5(b) is satisfied, a transferee must have the unconstrained right to obtain all or most of an acquired financial asset’s cash inflows, as those cash flows constitute the asset’s primary economic benefit.

In this example, it would be inappropriate to evaluate the "substantially all" hurdle based on financing that could be obtained by pledging both the debt instrument and other assets of the transferee. The unit of account is solely the transferred debt instrument, and thus the evaluation should exclude the financing capacity stemming from the transferee’s other assets. Accordingly, in our view, the condition in ASC 860-10-40-5(b) would be considered satisfied only if the transferor concludes that the incremental cash flows attributable to pledging only the debt instrument would meet the "substantially all" threshold – even though, as a legal matter, the financial asset in question may be pledged on a full recourse basis only.

When evaluating whether a transferee has the right to pledge or exchange a transferred financial asset, not only should the provisions in the relevant agreements that explicitly address this matter be considered, but also any other provisions in those agreements that could indirectly impact the transferee’s ability to exercise its stated rights to pledge or exchange. Particularly in this regard, conditional or contingent call options on transferred financial assets held by the transferor should be carefully evaluated to determine whether the options effectively constrain the transferee from pledging or exchanging the assets.

Example TS 3-4 and Example TS 3-5 illustrate how to apply this guidance in specific fact patterns.

EXAMPLE TS 3-4

Consideration of contingent call options – potential impact on transferee’s ability to pledge or exchange transferred financial assets

Originator Co sells consumer loans to Bank Co on a periodic basis. Originator Co continues to service the loans and holds a subordinated interest in the transferred pool. Originator Co has the right to repurchase any transferred loan that becomes delinquent, as defined in the servicing agreement. Given the credit quality of the loans, delinquencies are expected to occur with some degree of frequency, and Originator may find it advantageous to exercise its call to facilitate loan remediation/collection efforts. Bank Co has the contractual right to freely pledge or exchange any factored loan.

Since Bank Co is contingently obligated to return any delinquent loan to Originator Co, should its contractual right to pledge or sell the loans be considered substantive?

Analysis

It depends. Further analysis of the specific facts and circumstances would be required. The examples cited in ASC 860-10-40-17(c) can be read to suggest that the contingent call in this example presumptively should be considered to constrain Bank Co and provide more than a trivial benefit to Originator Co. However, upon further review, if commercially-feasible means exist that would allow Bank Co to monetize substantially all the value of the factored receivables if it so desired – the contingent call provisions and Originator Co’s subordinated interest notwithstanding – the condition in ASC 860-10-40-5(b) may be satisfied. For example, if Bank Co can unilaterally (and feasibly) sell undivided interests (participations) in the pool of factored receivables that would allow it to convert substantially all of the current value of its investment into cash, it may be appropriate to conclude that Bank Co has an unconstrained right to freely exchange the acquired loans.

EXAMPLE TS 3-5

Transferee’s ability to exchange transferred financial assets – consideration of all forms of transferor involvement

Transferor Co originates and periodically transfers loans to Warehousing Co, an unconsolidated LLC created specifically to acquire Transferor Co’s loans. Transferor Co, as Warehousing Co’s managing member, serves as Warehousing Co’s collateral manager. In that capacity, Transferor Co has the sole discretion to direct Warehousing Co to dispose of loans purchased from Transferor Co, including selling them to term securitization vehicles organized by Transferor Co.

A substantial portion of Warehousing Co’s financing consists of a credit line provided by Big Bank. In exchange for extending credit, Big Bank has a security interest in Warehousing Co’s loans, and thus Warehousing Co may not re-pledge them. Big Bank may look only to the loan collateral for repayment. The loan agreement further provides that, in the event Warehousing Co subsequently sells the loans, the proceeds must first be used to repay Big Bank’s loan. However, the loan agreement does not restrict Warehousing Co from selling the loan collateral to third parties and, similarly, there are no provisions in the LLC agreement that constrain Warehousing Co from doing so.

Should Warehousing Co be considered to have the unconstrained right to exchange (sell) the loans acquired from Transferor Co?

Analysis

No, it would be inappropriate to conclude that Warehousing Co has the right to freely sell the loans (and thus satisfy the condition in ASC 860-10-40-5(b)). Although, as a contractual matter, Warehousing Co has the unconstrained right to exchange loans acquired from Transferor Co, any such sale can be initiated only at the direction of Transferor Co in its capacity as the transferee’s collateral manager. ASC 860-10-40-17’s enumeration of conditions that both constrain a transferee and presumptively provide a transferor with a more than trivial benefit includes arrangements where a transferee can pledge or exchange transferred financial assets only on terms agreed to with the transferor. Transferor Co is the only party that can direct Warehousing Co to sell a loan. Warehousing Co cannot freely pledge the loans, given the security interest held by Bank Co.

Question TS 3-7 illustrates how to apply this guidance when the restriction is for a limited time period.

Question TS 3-7 A transferor initiates a plan to sell large blocks of receivables over a two-year period to reduce its credit risk. The transferor transfers the first block of receivables. To prevent the transferee from competing with it during the transferor’s next sale, the transferor restricts the transferee from selling or pledging the receivables for a period of 90 days. Does this restriction prevent sale treatment under paragraph ASC 860-10-40-5(b)?

PwC response

Yes. Sale treatment is precluded until the sale restriction lapses. Even if it were for only a week or a year. Transferor-imposed contractual constraints that narrowly limit timing or terms, such as those that allow the transferee to pledge only on the terms agreed to by the transferor, constrain the transferee and presumptively provide "more than a trivial" benefit to the transferor. Under this arrangement, the transferor benefits from knowing who currently owns the receivables and, further, the restriction ensures that the transferor will not be competing with the transferee as it seeks to sell additional receivables. By constraining the transferee, the transferor has not surrendered control over the transferred assets.

The transferor and transferee would initially account for the transfer as a secured borrowing, regardless of the length of the restriction. After the restriction is removed, the transfer would be recorded as a sale if the other conditions for derecognition are also met.

3.6.2.1 “Third-party purchaser” arrangements for CMBS

Under the Dodd-Frank rules, sponsors of commercial mortgage backed securities (CMBS) transactions are required to comply with certain “risk retention” obligations. This obligation can be satisfied if a third-party purchaser agrees to purchase and hold a prescribed interest in the securitization trust (sometimes referred to as the structure's "B-piece") for an extended period of time. During this extended period, the third-party purchaser is precluded from selling the prescribed interest. Accordingly, a question arose whether these transactions met the requirement for all third-party holders of beneficial interests issued in a securitization to have the right to freely pledge or exchange their investment.

In response to a submission by the Securities Industry and Financial Markets Association (SIFMA), the staff of the SEC's Office of the Chief Accountant (OCA) has indicated that it would not object to a conclusion by a transferor (securitizer) of commercial real estate loans that use of the "third-party purchaser" option permitted under the Dodd-Frank risk retention rules does not, in and of itself, jeopardize the transfer qualifying for de-recognition (sale accounting) in the transferor's financial statements. In a letter dated December 4, 2017, SIFMA confirmed its understanding of the SEC staff's position based on discussions held in November.

The SEC staff reached its view based on a broad array of considerations, which were not limited to its interpretation of the relevant provisions in ASC 860. The SEC staff considered the unique facts and circumstances described in SIFMA's submission, which arose as a result of a change in regulation in the securitization market, as well as the stated regulatory intent of the third-party purchaser option, which is to balance two overriding goals - namely, not to disrupt B-piece investor arrangements commonly seen in the CMBS market, while at the same time ensuring that risk retention promotes good underwriting. As a result, it would be inappropriate to extend the SEC staff's conclusions to other fact patterns.

3.6.3 More than a trivial benefit

A transferee may be constrained from taking advantage of its right to pledge or exchange a transferred financial asset. If the constraint provides the transferor with more than a trivial benefit, the transfer does not satisfy the requirement in ASC 860-10-40-5(b), and the exchange must be reported as a secured borrowing.

"More than a trivial benefit" is not a defined term. However, in practice, it connotes a very low bar or threshold. This may be inferred from the guidance in ASC 860-10-40-16:

A condition imposed by a transferor that constrains the transferee presumptively provides more than a trivial benefit to the transferor. A condition not imposed by the transferor that constrains the transferee may or may not provide more than a trivial benefit to the transferor. For example, if the transferor refrains from imposing its usual contractual constraint on a specific transfer because it knows an equivalent constraint is already imposed on the transferee by a third party, it presumptively benefits more than trivially from that constraint. However, the transferor cannot benefit from a constraint if it is unaware at the time of the transfer that the transferee is constrained.

A restriction imposed by a transferor presumptively provides more than a trivial benefit to the transferor; to assert otherwise begs the question why the transferor introduced the constraint in the first place. In our view, although all relevant facts and circumstances must be considered, this presumption can rarely, if ever, be overcome.

There are instances, however, when a transferor may be considered not to benefit from a constraint. These situations include:

The transferor is unaware of the constraint, as noted in ASC 860-10-40-16

As discussed in ASC 860-10-40-16A, although a transferor may be aware of a constraint, if it has no continuing involvement with the transferred financial assets, the condition in ASC 860-10-40-5(b) is nevertheless considered met

Example TS 3-6 illustrates how to apply this guidance to a specific fact pattern.

EXAMPLE TS 3-6

Evaluation of more than a trivial benefit

Company A transfers a group of loans to Company B, an operating entity that is highly leveraged, in exchange for cash and a beneficial interest in the loans. Company B is subject to covenants in debt agreements unrelated to the transfer that constrain it from pledging or otherwise monetizing the acquired loans. Company A is unaware of the constraints imposed by these debt covenants, and there are no provisions in the transaction’s purchase and sale agreement that impose any transfer restrictions on Company B.

How do the constraining covenants in the various lender agreements affect Company A’s assessment of Company B’s ability to pledge or exchange the transferred loans?

Analysis

Since Company A has no knowledge of the constraints imposed in the various lending agreements, it should not be considered to obtain more than a trivial benefit from them. The beneficiaries of the constraining covenants are presumptively Company B’s lenders – not Company A.

On the other hand, if Company A was aware of the constraining debt covenants at the time of the transfer, additional analysis would be required, since Company A has continuing involvement with the transferred loans. ASC 860-10-40-16 indicates that a constraining condition not imposed by a transferor may – or may not – provide more than a trivial benefit to the transferor, but provides no additional guidance in this regard. In this instance, if circumstances indicate or suggest that a constraining loan agreement was executed in contemplation of the transfer (so as to provide Company B with the funds necessary to acquire the loans from Company A), it may be appropriate to conclude that Company A obtains a more than trivial benefit from the constraint. Additionally, if Company A agreed to forego imposing its usual constraints due to corresponding provisions in the loan agreement, this too would suggest the existence of more than a trivial benefit.

3.6.3.1 Absence of continuing involvement

If a transferor has no continuing involvement with transferred financial assets, the condition in ASC 860-10-40-5(b) is considered met in all circumstances.

In some circumstances in which the transferor has no continuing involvement with the transferred financial assets, some conditions may constrain a transferee from pledging or exchanging the financial assets. Paragraph 860-10-40-5(b) states that if the transferor, its consolidated affiliates included in the financial statements being presented, and its agents have no continuing involvement with the transferred financial assets, the condition under paragraph 860-10-40-5(b) is met. For example, if a transferor receives only cash in return for the transferred financial assets and the transferor, its consolidated affiliates included in the financial statements being presented, and its agents have no continuing involvement with the transferred financial assets, sale accounting is allowed under paragraph 860-10-40-5(b) even if the transferee entity is significantly limited in its ability to pledge or exchange the transferred assets.

Question TS 3-8 explains the rationale behind this guidance.

Question TS 3-8 How does the absence of continuing involvement affect a transferor’s evaluation of the "right to pledge or exchange" criterion in ASC 860-10-40-5(b)?

PwC response

ASC 860-10-40-16A indicates that if the transferor has no continuing involvement with transferred financial assets, the lack of continuing involvement would be a determinative factor in concluding that the condition in ASC 860-10-40-5(b) is satisfied – even if the transferee is constrained from pledging or exchanging the assets, and regardless of the source of those restrictions. The rationale for this conclusion is that, even if a transferee is constrained, the transferor derives no benefit from the arrangement, as the transferor no longer has any interest in (or obligation to augment) the transferred assets’ cash flows. Said differently, if a transferor no longer has continuing involvement with a transferred asset’s cash flows, it would be anomalous to continue to report the asset on its balance sheet. Accordingly, absent continuing involvement, a transferor may consider the criterion in ASC 860-10-40-5(b) to be satisfied, even if the transferee is constrained.

3.6.4 Consideration of freestanding option or forward contracts

A transferor and transferee may enter into a freestanding option or forward contract that entitles or obligates the transferor to re-acquire the transferred financial asset.

If the asset is not readily obtainable in the marketplace, ASC 860-10-40-17 indicates that these arrangements should be considered to benefit the transferor, and likely to constrain the transferee. In these circumstances, careful analysis of the facts and circumstances is warranted if it is asserted that, the option or forward contract notwithstanding, the transferee nevertheless has the unconstrained ability to monetize substantially all the asset’s flows by pledging or exchanging it.

Similarly, a freestanding in-the-money put held by a transferee that entitles it to sell a transferred financial asset to the transferor should be evaluated carefully to assess whether the put constitutes a “constructive forward” contract, stemming from the option’s beneficial economic terms. If so, and if the underlying asset is not readily obtainable, it may be appropriate to conclude the contract constrains the transferee—as it may be unable to monetize substantially all the asset’s cash flows by pledging or exchanging it, and still be assured that it can deliver the asset to the transferor and benefit from the put’s beneficial terms.

A call option on transferred assets, depending on its features, could cause a transfer to fail either the condition in ASC 860-10-40-5(b) if it constrains the transferee as described above, or the condition in ASC 860-10-40-5(c) if it provides the transferor with effective control, or both. Hence, options on the transferred assets should be analyzed to see if they meet the requirements of both conditions. For example, a deep-in-the-money put held by a transferee may also be considered to provide the transferor with effective control. Another example is an attached call option which might not constrain the transferee from pledging or exchanging the asset, but could result in the transferor’s maintaining effective control because it gives the transferor the unilateral ability to cause whoever holds that specific asset to return it (see TS 3.7.2).

3.6.5 Summary

Most transferor-imposed constraints on a transferee’s ability to pledge or exchange acquired financial assets lead to a conclusion that the transfer does not satisfy the criterion of ASC 860-10-40-5(b). As such, sale accounting is precluded because control is not considered to have passed to the transferee. Conditions not imposed by a transferor that potentially constrain a transferee require additional analysis to determine their implications on sale accounting.

When performing this analysis, all arrangements involving the transferee and the transferor, its consolidated affiliates in the financial statements being presented, and its agents should be considered.

Although a contractual provision may not constrain the transferee (or holder) when evaluated on a standalone basis, certain terms or conditions may constrain the transferee (or holder) when evaluated collectively. Ultimately, the analysis of the impact of conditions imposed by the transferor or by others should be specific to the facts and circumstances of the transaction.

Finally, a transferor having no continuing involvement with transferred financial assets may conclude that the condition in ASC 860-10-40-5(b) is satisfied, even if the transferee is constrained from selling or pledging the assets.

9TS 3.6.3 discusses the “more than a trivial benefit” criterion.

10 A freestanding option or forward contract does not “travel” with the underlying asset, in contrast to an “attached” arrangement. The underlying trades separately from the contract.

11 If an agent is acting on behalf of a transferor, any transfer restrictions imposed by the agent in connection with the transaction should be considered the equivalent of a transferor-imposed constraint. If a more-than-trivial benefit is attributed to the constraint, then the transfer may fail the criterion in ASC 860-10-40-5(b).

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.