ASC 810-10-25-38B

A reporting entity must identify which activities most significantly impact the VIE’s economic performance and determine whether it has the power to direct those activities. A reporting entity’s ability to direct the activities of an entity when circumstances arise or events happen constitutes power if that ability relates to the activities that most significantly impact the economic performance of the VIE. A reporting entity does not have to exercise its power in order to have power to direct the activities of a VIE.

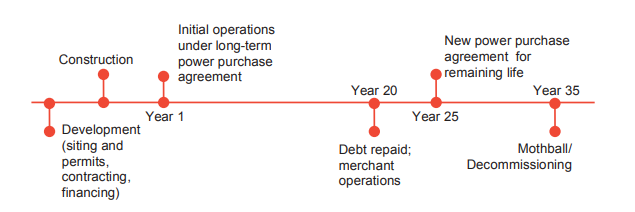

The primary beneficiary of a VIE is the variable interest holder with the power to direct the activities of the VIE that most significantly impact the VIE’s economic performance. The significant activities of a single power plant entity evolve and mature over the life of the power plant and, as a result, the party controlling those activities may also change over time. The life cycle of a typical power plant is depicted in Figure 10-9:

Figure 10-9

Typical power plant life cycle

The primary beneficiary should also have a significant financial interest; however, this is not typically a key consideration because most variable interest holders will meet this criterion. Multiple parties may have potentially significant financial interests, but only one party can have the power to direct the most significant activities. Therefore, the identification of the most significant activities impacting the economic performance of the entity and evaluation of who controls these activities are critical steps in the determination of the primary beneficiary.

A single power plant entity is engaged in different activities over its life cycle (i.e., the activities are generally linear), and each significant activity is contingent on the prior significant activity. As a result, a reporting entity’s evaluation of which activities are most significant should focus on the uncertainty of completing each stage as well as the activities in each stage that will most significantly impact the economic performance of the entity. If there is uncertainty that the entity will achieve the next stage of its operations, usually only the significant activities in the current phase are considered. However, once the uncertainty regarding achieving progress to additional phases has lapsed, the reporting entity should evaluate which powers are most significant considering the remaining life cycle of the entity.

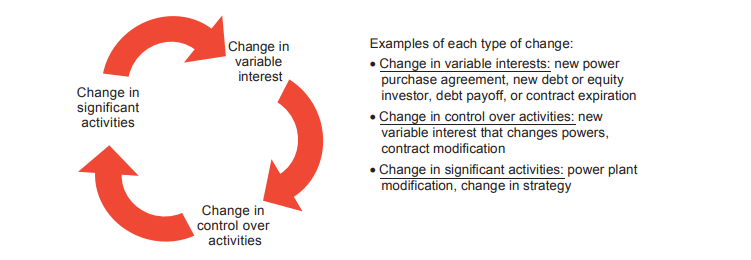

Once the reporting entity identifies which activities most significantly impact the economic performance of the VIE, it should determine which party controls these activities. Contractual arrangements often dictate which party, if any, has the power to direct activities that are most significant to the economic performance of a VIE. In completing this analysis, a shift in which party holds a specific power as a result of changes in contractual arrangements or counterparties should not be considered until those changes are in effect. This analysis may result in changes in the primary beneficiary over the life cycle as control of significant activities moves among the parties involved with the power plant and the VIE. For example, a purchase option embedded in an operations and maintenance agreement might lead to a change in the party with control, but the party with the option is not deemed to have control until the point at which the option is exercised. However, a reporting entity can anticipate how those changes are likely to impact the primary beneficiary conclusion and should make sufficient disclosures for potential material changes in the future. Figure 10-10 provides a summary of activities that may require consideration in determining the significant activities over the life of a typical power plant.

Figure 10-10

Significant activities during a power plant’s life cycle

|

Development stage

- Siting and permitting may impact future profitability (location may impact dispatch, success of renewable plant)

- Financing may be obtained during this stage; the entity frequently depends on a long-term power purchase agreement

- Strategy may involve decisions on investment, future development, supply, and energy production

|

- Key strategic decisions (e.g., location, type of power plant, technology) are likely to have the most significant impact during this stage

- During development, control is typically retained by the equity holders

- Due to significant inherent uncertainty, prior to the start of construction the determination of the primary beneficiary usually focuses on powers held during this stage

|

Construction stage

- Construction is the primary activity during this phase; completion of construction may be a condition for the activation of other operating agreements

|

- The EPC contractor and developer are likely actively involved in oversight of construction; an EPC contract may absorb risks associated with the entity through completion of this phase

- A power purchase agreement or debt arrangement may include protective rights that would not impact the evaluation

- Once construction commences, there is generally a high degree of certainty that the entity is viable. See the response to Question 10-9 for discussion of primary beneficiary.

|

Operations stage

- Operations and maintenance activities are essential for the power plant to dispatch and earn a profit; may be substituted among different service providers for most types of power plants

- Power plant dispatch, when combined with control over fuel supply, may dominate economic performance for certain power plants

- Fuel strategy may significantly influence power plant economic performance (e.g., storage, hedging, pricing)

|

- Multiple parties may share power over different activities

- Although parties holding the power may shift in the future (e.g., operations and maintenance provider will change), the evaluation usually focuses on which party currently holds the powers

- Evaluation of relative importance of various activities may be supported by quantitative analysis, if necessary

- Lease arrangements may impact the determination of which activities are significant (i.e., the existence of a lease may mean that fuel and dispatch risks are designed out of the entity)

|

Post-operation/ decommissioning

- Strategy of managing the power plant post-commercial operation

- Dismantling the power plant can be complex, depending upon the type of generation

- Asset retirement obligations must be satisfied

|

- Equity holders are likely the primary party involved at this stage

|

The evaluation points in Figure 10-10 are based on typical activities and common contractual arrangements. A reporting entity should consider its specific facts and circumstances in completing the primary beneficiary analysis.

Question 10-9

How do changes in significant activities over the life of the power plant impact the primary beneficiary determination?

PwC response

The significant activities of a single power plant entity during its life cycle are generally sequential: beginning with development, then construction, followed by operations, with a final wind-down and decommissioning. In evaluating the relative significance of the powers during each stage, the parties should focus on the purpose and design of the entity, the significance of the activities throughout the life of the entity, the ability of the variable interest holders to impact the completion of each phase, and the likelihood the phases will be successful.

Factors to consider include:

- Development

Significant uncertainty is often present during the development stage while the entity identifies a location, obtains permits and financing, and potentially contracts for output of the plant. All other activities of the plant (construction and operation) are contingent on the completion of development, and entities do not always advance beyond this stage. Due to this uncertainty, the parties would generally conclude that the power to control strategy and development, as well as arranging financing, are the most important powers during this stage of the life cycle.

- Construction

Once the entity has obtained all required permits and financing and has executed a construction contract, there is generally a high degree of certainty that the power plant will be completed and that operations will commence. As such, in evaluating the most significant activities during this stage, the parties may consider the powers that will impact economic performance over the entire remaining life cycle of the power plant. This may lead to the conclusion that the powers held during the operations phase are more significant than the powers during construction. Note that this conclusion may change if there is more uncertainty during construction (e.g., experimental technology) or if there is uncertainty about the operations phase (e.g., power contracts, operations and maintenance agreements, or other service contracts are not yet executed). Any uncertainty about successful completion of the project would lead to a focus on construction activities only in completing the evaluation during this stage.

- Operations

The key activities identified during the operations phase will often have the most significant overall impact on the economic performance of the entity over its life-cycle (once uncertainty about reaching the construction phase has been resolved). Therefore, once there is a high level of assurance that construction will be achieved, the evaluation generally focuses on which parties control key operating decisions. See

UP 10.6 for examples of application of by-design in the evaluation of potential variable interests in a single power plant entity.

The consideration of who controls the significant activities is judgmental, and specific facts and circumstances can result in different conclusions. Factors that may influence the conclusion are discussed in the following sections.

Question 10-10

Does contract length factor into the evaluation of the primary beneficiary?

PwC response

Generally, no. When considering a contract that is a variable interest, the term of the contract is generally not important to the holder’s power relative to the VIE. Holding powers provided by the contract for a longer period should therefore not impact the conclusion as to which party is the primary beneficiary.

Thus, in general, we do not believe that contract length is a defining factor in determining which variable interest holder controls activities that are most significant to the entity. As discussed above, once development is completed and construction begins, the evaluation is typically focused on which party holds the most significant powers during the operations phase (unless there is significant uncertainty regarding construction). If the party holding those powers shifts over time, the primary beneficiary analysis is performed based on who has the power to direct the most significant activities as of the reporting date, without incorporating the impact of expected future contractual changes (e.g., expiration of certain contractual arrangements). Therefore, the length of a contract would not impact this analysis. However, in some cases contract length may impact the determination of whether a contract is a variable interest (see the response to Question 10-6).