Assessing whether a contractual arrangement is a variable interest is an important element of the VIE consolidation model. This requires an assessment of the design and purpose of the entity being evaluated, as well as the risks in the entity that interest holders may be required to absorb that would result in those interests being variable interests. The determination of which contractual and ownership interests are variable interests is based on this evaluation of the design and risks of the VIE.

Partial definition from ASC 810-10-20

Variable Interests: The investments or other interests that will absorb portions of a variable interest entity’s (VIE’s) expected losses or receive portions of the entity’s expected residual returns are called variable interests. Variable interests in a VIE are contractual, ownership, or other pecuniary interests in a VIE that change with changes in the fair value of the VIE’s net assets exclusive of variable interests.

Potential variable interests in a single power plant entity include power purchase agreements, equity interests, debt interests, management agreements, operations and maintenance agreements, and other contractual arrangements. This section discusses the overall framework for determining whether a contractual or other interest is a variable interest.

10.2.1 The “by-design” approach to determining variability and variable interests

The “by-design” model is a fundamental aspect of assessing the variable interests in a VIE. It was introduced in FASB Staff Position (FSP) No. FIN 46(R)-6, Determining the Variability to Be Considered in Applying FASB Interpretation No. 46(R) (FSP FIN 46(R)-6), in 2006. FSP FIN 46(R)-6 was issued to address diversity in the methods used to identify variable interests and has been codified in ASC 810.

10.2.1.1 What is the “by-design” model?

At a high level, the by-design model requires consideration of:

• The design of the entity being evaluated

• The types of risks and rewards that the entity is designed to create and that the interest holders are asked to absorb or benefit from, based on the purpose for which the entity was created

• Whether the individual interests create or absorb risks

In making the initial assessment, reporting entities should consider all contractual documents that relate to the entity, including those concerning formation, governance, marketing, and other arrangements with interest holders. Each of these sources of information provide insight into the risks the entity was designed to create and which parties are expected to absorb those risks or receive associated benefits. Those interests that absorb risk and the variability created by those risks should be assessed as variable interests.

10.2.1.2 How is the by-design model applied?

ASC 810-10-25-22 provides guidance for applying the by-design model.

The variability to be considered in applying the Variable Interest Entities Subsections shall be based on an analysis of the design of the legal entity as outlined in the following steps:

a. Step 1: Analyze the nature of the risks in the legal entity (see paragraphs 810-10-25-24 through 25-25).

b. Step 2: Determine the purpose(s) for which the legal entity was created and determine the variability (created by the risks identified in Step 1) the legal entity is designed to create and pass along to its interest holders (see paragraphs 810-10-25-26 through 25-36).

Considerations in applying this model to a single power plant entity follow.

Step 1: analyze the risks in the entity

The guidance outlines potential risks to be considered, including credit risk, interest rate risk, commodity price risk, and operations risk. This list is not all inclusive, and reporting entities should consider all risks in the entity. Risks typical to a single power plant entity include:

• Construction risk associated with building the power plant

• Price risk related to changes in the value of the power plant asset

• Credit risk associated with sales or purchase agreements

• Commodity price risk

• Production risk (for certain renewable plants or experimental technology)

• Operations risk associated with operating the power plant

Reporting entities should also consider other potential risks (e.g., foreign currency exchange risk if the power plant is located in another country and interest rate risk associated with any investments) in evaluating the overall design of the entity. When assessing the risk profile of a single power plant entity, it may be beneficial to consider the characteristics of a merchant generator regardless of the nature of contracts that may be in place (e.g., power purchase agreement, fuel supply contract, regulatory authority). This will ensure that a full analysis of potential risks has been considered in the evaluation, even if certain of those risks may have been allocated among entities by the design of the legal entity.

Step 2: determine the purpose for the entity and variability

As discussed in ASC 810-10-25-25, the identification of risks and variability in a variable interest entity should incorporate all relevant facts and circumstances, including the entity’s activities, terms of the entity’s contractual arrangements, nature of ownership interests issued, how interests were negotiated with or marketed to potential investors, and which parties participated in the entity’s design.

ASC 810-10-25-26 further states that other contracts may appear to both create and absorb variability and that the assessment of whether the contract is a variable interest should be based on the role of the contract in the design of the entity, regardless of its legal form or accounting classification. The guidance also highlights a number of strong indicators that suggest whether an interest is a variable interest (i.e., an absorber of variability).

Typically, assets and operations of the legal entity create the legal entity’s variability (and thus, are not variable interests), and liabilities and equity interests absorb that variability (and thus, are variable interests).

A qualitative evaluation of the design of the entity often is sufficient to identify the variability that should be considered and to determine which interests are variable interests. ASC 810-10-25-30 through 25-36 also provide the following indicators to consider in evaluating variability:

• Terms of interests issued — is risk and/or return of assets or operations of the VIE transferred to the interest holder? This is a strong indication of the type of variability the entity is designed to create and pass along to interest holder(s).

• Subordination — if both senior and subordinated interests are issued, is the interest substantively subordinate to senior interests? This is another indication that the interest is designed to absorb variability.

• Certain interest rate risk — will interest rate fluctuations result in variations in cash proceeds from sales of fixed-rate investments or other investments that will be sold prior to maturity to meet the entity’s obligations? This is a strong indicator that the entity was designed to pass along this variability to its interest holders.

• Certain derivative instruments — is the interest a derivative with an underlying based on an observable market price and with a counterparty senior to other interest holders? If yes, this is a strong indication that the derivative creates, rather than absorbs, variability of the entity. However, even if these two conditions are met, a derivative may still be a variable interest, if it absorbs the variability associated with the majority of the VIE’s assets or operations. In such cases, further evaluation would be necessary.

A single power plant entity is not typically designed to pass along interest rate risk to its variable interest holders; therefore, this risk is not further discussed in this section. See CG 3.2.5 for further information on considerations related to the evaluation of interest rate risk.

Question 10-1 How should a reporting entity assess whether a power purchase agreement is a variable interest?

PwC response

In accordance with ASC 810, the by-design model should be used to identify the types of variability in an entity that may create a variable interest. However, at the time FASB Interpretation (FIN) No. 46 (revised 2003), Consolidation of Variable Interest Entities, an interpretation of ARB No. 51 (FIN 46(R)), was originally adopted, practice developed whereby reporting entities applied one of two methods in evaluating whether a power purchase agreement was a variable interest: the “fair value method” or the “cash flow method.”

• Fair value method — focuses on whether the contract being analyzed shields the variable interest entity from changes in the fair value of its assets. As a general rule, a contract would be a variable interest if the existence of the contract reduces the variability in the value of the variable interest entity’s assets.

• Cash flow method — focuses on whether the contract directly absorbs some or all of the operating cash flows of the variable interest entity.

As discussed above, the FASB issued FSP FIN 46(R)-6 to address this diversity in practice. The guidance was codified in ASC 810-10-25-23.

After determining the variability to consider, the reporting entity can determine which interests are designed to absorb that variability. The cash flow and fair value are methods that can be used to measure the amount of variability (that is, expected losses and expected residual returns) of a legal entity. However, a method that is used to measure the amount of variability does not provide an appropriate basis for determining which variability should be considered in applying the Variable Interest Entities Subsections.

In accordance with this guidance, reporting entities should apply the by-design model to determine the type of variability that may create a variable interest. The cash flow and fair value methods may then be used to measure the amount of variability. ASC 810-10-55-55 provides examples of how to apply the by-design model. See UP 10.6 for examples of applying the by-design model in evaluating potential variable interests in a single power plant entity.

The following sections include information on how to assess potential variable interests in single power plant entities (e.g., power purchase agreements and equity investments) using the by-design model.

10.2.2 Power purchase agreements

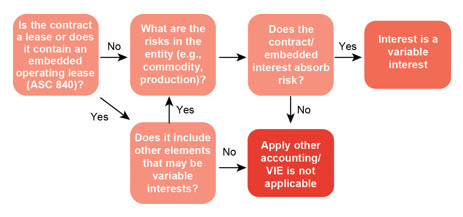

Many single power plant entities include plant-specific power purchase agreements. The accounting for and evaluation of a power purchase agreement under the variable interest entity model depends, in part, on how the entity accounts for the power purchase agreement (i.e., lease, derivative, or nonderivative executory contract). Therefore, the evaluation of whether a power purchase agreement is a variable interest begins with a determination of the appropriate contract accounting model. Figure 10-3 depicts the overall process for evaluating whether a power purchase agreement is a variable interest.

Figure 10-3 Evaluating whether power purchase agreements are variable interests

Power purchase agreements may create or absorb various risks, including commodity price risk, production risk, operations risk, fuel risk, and credit risk.

10.2.2.1 Is the contract a lease or does it contain an embedded lease?

Power purchase agreements are often accounted for as leases in accordance with ASC 840. To preserve the existing model for lease accounting, the FASB provided a specific exception in the VIE guidance for those agreements qualifying as operating leases.

Receivables under an operating lease are assets of the lessor entity and provide returns to the lessor entity with respect to the leased property during that portion of the asset’s life that is covered by the lease. Most operating leases do not absorb variability in the fair value of a VIE’s net assets because they are a component of that variability. Guarantees of the residual values of leased assets (or similar arrangements related to leased assets) and options to acquire leased assets at the end of the lease terms at specified prices may be variable interests in the lessor entity.

Consistent with this guidance, in general, an operating lease agreement (including an operating lease embedded in a power purchase agreement) where the VIE is the lessor is not a variable interest. However, all contractual arrangements, including operating leases, should be evaluated to determine if the agreements contain other embedded elements that should be evaluated as variable interests. Therefore, reporting entities should not automatically bypass operating lease contracts in the evaluation of variable interests. Potential variable interests in a lease include:

• Lessee residual value guarantees

• Lessee purchase option or call at specified prices

• Lessee renewal options at a specified price other than fair value

• Put option on the leased assets by the VIE

These instruments generally provide an “option” or impose an “obligation” that triggers with a change in the price of the asset and either entitle a holder to a gain (purchase option) or obligate it to incur a loss (residual value guarantee). As highlighted in ASC 810-10-55-39, these elements likely represent variable interests that require further consideration in the evaluation of the primary beneficiary.

Question 10-2 Is a contractual arrangement accounted for as a capital lease a variable interest?

PwC response

It depends. The lease exception included in ASC 810-10-55-39 is specifically provided for operating leases and does not extend to capital leases. The guidance states that operating lease receivables do not absorb variability (thus are not variable interests) because they are a component of the variability of the fair value of the VIE’s net assets.

In evaluating whether a capital lease is a variable interest, a reporting entity should gain an understanding of the reasons the lease is classified as a capital lease. Capital leases that are the substantive equivalent of a loan would not be a variable interest. These are the types of leases that require the lessee to pay periodic rents for a term that is at least 75% of the property’s economic life or that amounts to at least 90% of the property’s value. In contrast, capital leases that contain fixed price purchase options or residual value guarantees would be considered to contain variable interests. The reporting entity may conclude that this type of lease arrangement is a creator of variability, similar to an operating lease (i.e., because the capital lease is a financial receivable for the entity, it is a creator of risk).

All lease agreements should also be analyzed to determine whether they include a variable interest such as an embedded operations and maintenance agreement, a residual value guarantee, or some other protection against variability. Even if the capital lease itself is deemed not to be a variable interest, such components within the agreement may be variable interests that would require further consideration.

Question 10-3 Is a contract that otherwise qualifies as a lease, but that was grandfathered under the transition provisions of EITF 01-8, eligible for the lease exception provided by ASC 810?

PwC response

No. The lease exception applies only to contracts that are accounted for as leases. It should not be applied by analogy to other contracts that are economically similar to leases but that are not accounted for as leases. Prior to the Codification, EITF 01-8, paragraph 16, provided the following transition provisions, in part:

The consensus in this Issue should be applied to (a) arrangements agreed to or committed to, if earlier, after the beginning of an entity’s next reporting period beginning after May 28, 2003, (b) arrangements modified after the beginning of an entity’s next reporting period beginning after May 28, 2003, and (c) arrangements acquired in business combinations initiated after the beginning of an entity’s next reporting period beginning after May 28, 2003.

Thus, some power purchase contracts that include embedded leases under the provisions of ASC 840 do not follow lease accounting because they were “grandfathered” by EITF 01-8. These contracts are not eligible for the exception provided for leases and should be analyzed as potential variable interests.

Question 10-4 Are energy price and dispatch risks part of the design of an entity if the generating plant has been fully contracted to a third party in an agreement accounted for as an operating lease?

PwC response

Generally, no. Power purchase agreements may be structured in terms of the output from the property (e.g., the off-taker has the right to all power produced from the facility and has the right to dispatch). However, if the power purchase agreement is a lease, the agreement is effectively for the use of the property itself, and not for the purchase of the output from the property. As such, dispatch and energy price risk are exposures for the lessee and are thus primarily outside the design of the entity. However, in many cases, the offtake agreement includes some payment amounts that are contingent on future operations (e.g., variable operations and maintenance payments based on plant dispatch and/or energy production). These contingent payments allow the owner/operator to participate in the success or failure of the off-taker. The variability of rents linked to volume is included in the design of the entity and is generally absorbed by the equity participants.

Embedded fuel or operations and maintenance agreements

In addition to the potential variable interests highlighted above that may be embedded in a lease, leases may also include fuel, management, operations and maintenance, or other service agreements. This type of embedded agreement may create or absorb risk in the entity, depending on its terms.

For example, in a tolling agreement, only a portion of the payments (the amount related to the contractual use of the plant) represent minimum lease payments and related executory costs under ASC 840. The remainder of the payments would be identified as contractual payments to the VIE for management and operations. Similarly, a fixed-price arrangement or a heat rate contract may also include an element for fuel (i.e., an embedded fuel supply agreement). The energy component may be separately identified in the agreement or included in another cost element. Depending on the structure and contractual terms, these types of embedded agreements may represent variable interests, because payments for fuel or operations and maintenance may absorb a significant amount of the variability of the entity.

In assessing whether these contracts absorb risk, the reporting entity should evaluate whether the entity has more risk with or without the contract. For example, the entity may be exposed to some risk associated with a long-term operations and maintenance agreement if the pricing is based on an inflation escalator (i.e., the entity has risk that its costs will increase faster than inflation). However, without the agreement, the entity would be exposed to potential volatility and uncertainty and the risk that its costs may not be recovered. Therefore, in this fact pattern, the embedded operations and maintenance agreement is a net absorber of risk from the entity and is a variable interest. The factors for evaluating embedded agreements are similar to those considered in evaluating nonlease power purchase agreements (see UP 10.2.2.2).

10.2.2.2 Does a power purchase agreement or embedded interest create or absorb risk in the entity?

If a power purchase agreement does not qualify for the operating lease exception or if there are potential variable interests embedded in an operating lease,

the reporting entity should perform further analysis of the design of the entity to determine if the power purchase agreement is a creator or absorber of risk. Key considerations in making this assessment include the nature of the contract, the rights that it conveys to the holder, and the interaction with other interests in the entity. The evaluation should follow the by-design model as discussed in UP 10.2.1. ASC 810-10-55-27 through 55-28 also provide guidance on how to evaluate fixed-price forward contracts.

Forward contracts to buy assets or to sell assets that are not owned by the VIE at a fixed price will usually expose the VIE to risks that will increase the VIE’s expected variability. Thus, most forward contracts to buy assets or to sell assets that are not owned by the VIE are not variable interests in the VIE.

Conversely, ASC 810-10-55-28 indicates that fixed-price forward contracts to sell assets that are owned by the entity generally absorb or reduce variability and are variable interests with respect to the assets. ASC 810-10-55-29 provides additional guidance in the context of derivative instruments; however, this guidance is also helpful in the evaluation of all types of power purchase agreements (other than leases, as specifically discussed above).

ASC 810-10-55-29

Derivative instruments held or written by a VIE shall be analyzed in terms of their option-like, forward-like, or other variable characteristics. If the instrument creates variability, in the sense that it exposes the VIE to risks that will increase expected variability, the instrument is not a variable interest. If the instrument absorbs or receives variability, in the sense that it reduces the exposure of the VIE to risks that cause variability, the instrument is a variable interest.

In evaluating whether a power purchase agreement creates or absorbs risk, the reporting entity should assess the pricing structure of the contract and the nature of the entity’s operations. Case H in ASC 810-10-55-81 through 55-86 illustrates the application of the by-design model to a VIE with a power purchase agreement.

Whether a contract creates risk for the entity or absorbs a risk already existing in the entity is a key factor in determining whether a contract is a variable interest. If the intent of the contract within the design of the VIE is to absorb an element of its risk, absent an exception to the accounting, it will be a variable interest. Reporting entities should also consider the relative seniority of the contract. A contract that appears to absorb risk may not be a variable interest if it is senior to debt and equity interests and its use as a risk absorber is remote. See the response to Question 10-5 for further information.

In evaluating power sales agreements that are not leases, the entity is selling output that has not yet been generated (and is thus not owned). Therefore, in applying this guidance to these types of arrangements, we typically consider the risk associated with activities necessary to produce the output. If the entity has a fixed-price power sales agreement and is exposed to fuel price risk, the analysis generally follows the evaluation for a fixed-price contract for sale of an asset that is not owned because of the procurement risk associated with fuel (assuming that the entity has not locked in the price of fuel through long-term contracts or financial hedges). However, if there is no fuel price risk because it is absorbed in the contract (such as in a tolling agreement), fixed in the initial design, or otherwise not applicable to the entity (as in the case of a renewable plant), the evaluation of a fixed-price contract would more closely follow that for an asset that is owned.

In another scenario, if a power plant is designed to sell some of the output into the market and some through a power purchase agreement, the power purchase agreement may be a variable interest since the single power plant entity is designed to take on some commodity price risk.

Figure 10-4 summarizes application of this guidance to common power purchase agreements (assuming the contracts are not leases). The design of the entity, the contract terms, and other contractual arrangements should be evaluated in determining whether a specific contract creates or absorbs risk. All power purchase agreements create credit risk, unless fully collateralized. However, unless the contract is with a counterparty that has an unusual level of credit risk that is not appropriately mitigated by the contract terms, credit risk generally would not change the conclusion as to whether the contract is a creator or absorber of risk in an entity. As noted in Figure 10-4, the considerations for renewable energy projects and fossil fuel plants may vary due to differences in the risk profiles of the production facilities.

A reporting entity should consider the design of the entity as well as a contract’s predominant characteristics in considering whether it is a creator or absorber of risk. For example, a fixed-price contract may escalate with inflation or have scheduled increases over the life of the contract. Although the price is changing over time, this contract is predominantly fixed price because the purchase price does not fluctuate with fuel or energy prices.

Figure 10-4 Variable interests: Evaluation of common power purchase agreements

Power plant type

Contract type

Considerations

Evaluation

Fossil (e.g., coal, natural gas)

Fixed-price contract

A fixed-price contract for an asset that is not owned creates risk (fuel price risk).

Contract generally creates risk and is generally not a variable interest (ASC 810-10-55-27), unless fuel cost is also fixed in the initial design.

Tolling agreement

Effectively a service agreement; absorbs commodity price risk. Volume-based pricing may create risk.

Contract absorbs risk and is likely a variable interest.

Heat rate contract

Protects the entity from natural gas/energy price risk; ensures return. Level of return may have variability if payments are linked to volumes.

A heat rate contract based on the plant heat rate absorbs risk and is likely a variable interest.

Renewable (e.g., wind, solar)

Fixed-price contract; no minimum quantity guarantee1

A fixed-price contract absorbs commodity price risk. Variability of volume is risk retained in the entity.

Contract absorbs risk and is likely a variable interest.

A fixed-price contract absorbs commodity price risk; however, a minimum guarantee may create production risk for the VIE.

Further evaluation is required. The assessment depends on level of risk associated with production guarantee.

Variable price contract; linked to price of natural gas

Contract price linkage creates commodity price exposure to the entity.

Contract creates risk and is not a variable interest.

Fixed-priced contract up to certain production level; price reduced for additional production above specified quantity

A fixed-price contract generally absorbs commodity price risk; however, a reduction in price may create production risk for the VIE.

Further evaluation is required. The assessment depends on the magnitude of the pricing change.

1Minimum quantity guarantees are commonly included in renewable energy power purchase agreements and are typically supported by an engineering study that projects, at a high statistical confidence level, the expected output of an asset. If the minimum guaranteed production level is not achieved, the contract usually includes a penalty or default clause compensating the off-taker.

The following discussion provides a general framework for the evaluation of different types of contracts; however, each contract should be evaluated in the context of its individual facts and circumstances. See UP 10.6 for examples of how to determine whether various types of contracts are variable interests.

Fossil fuel projects

Fossil fuel projects include coal, oil, and natural gas-fired power plants. The operations of, and production of electric energy from, fossil fuel plants are generally highly reliable. However, these types of power plants are exposed to fluctuations in the price of fuel, which is often volatile. Key evaluation factors when considering whether different types of power purchase agreements create or absorb risk in a fossil fuel plant are discussed below. These discussions assume that the contracts are not accounted for as leases.

Fixed-price contracts

The evaluation of a fixed-price contract that is not a lease generally follows the guidance for forward contracts in ASC 810-10-55-27. In the case of a fixed-price power sales agreement sourced by a specific power plant, the entity has the ability to create energy but may not own all of the primary inputs that would be consistent with ownership of the asset (primarily the fuel supply). In the case of a natural gas or other fossil fuel plant, a fixed-price contract exposes the entity to fuel price risk because the quantity required under the contract must be delivered regardless of the cost of production. Therefore, consistent with the guidance in ASC 810-10-55-27, fixed-price power sales agreements are usually not variable interests because these contracts are designed to create, rather than absorb, risk in the entity.

However, a reporting entity should consider all contractual arrangements of the entity in evaluating the design. For example, if the entity signs a fixed-price long-term fuel-supply agreement as part of its formation and concurrently a fixed-price power sales agreement, the fuel supply and power sales agreement together absorb the entity’s commodity price risk. Furthermore, the design may be such that the fixed price established in the contract is high enough to assure a certain degree of gross margin, thereby in fact absorbing a high degree of variability. In such cases, the power sales agreement may be a net absorber of commodity risk in the entity. Consideration should be given to the lengths and terms of the respective contracts. A short-term fuel-supply agreement may not sufficiently absorb risk from an entity that has a long-term power sales agreement in place. Contracts rarely cover the full life of a power plant asset, so the duration of the agreements may be a relevant factor. Refer to Question 10-6.

Tolling agreements

In a tolling agreement, the off-taker provides its own fuel for production and the generator provides energy based on a specified heat rate (typically based on the operations of the underlying facility). In a tolling agreement, fuel price risk is absorbed through the contract and the off-taker is effectively paying the entity for a conversion service. This type of contract absorbs a significant amount of risk from the entity because it has locked in a defined level of profit on its future sales. The entity generally retains some operational risk, including the risk that it will not operate at the level of efficiency specified in the contract (based on the specified heat rate), that its cost of operations will increase faster than the level of reimbursement provided in the tolling agreement, and that unscheduled down-time will result in reduced capacity payments.

In evaluating whether the contract is a creator or absorber of risk, the entity should generally perform a “with-and-without” analysis (i.e., is there more risk with or without the contract?). Although the entity may have risk associated with increases in the cost of operations or decreases in the efficiency of the plant, this risk is typically minimal compared to the risk of volatility associated with operating as a merchant plant. In addition, some tolling agreements expose the entity to market price risk because cash flows vary depending on dispatch; however, again, this exposure is usually minimal compared to operations without the contract. As such, a tolling agreement protects the debt and equity holders and typically provides assurance of future cash inflows. Therefore, in general, we would expect this type of agreement to be a variable interest.

Heat rate contracts

A single power plant entity may enter into a power sales arrangement that passes through fuel costs to the buyer, based on a specified heat rate. The heat rate represents the efficiency of the power generating plant, or the amount of energy used by a power plant to generate one kilowatt hour (kWh) of electricity. The higher the heat rate, the lower the plant efficiency. The specific arrangement may vary to meet the needs of the power plant and the off-taker. For example, a power plant may operate as a base load unit, with a specified amount of fuel and energy provided every day, while a peaking facility may dispatch as requested by the off-taker. In general, the risk profile of a heat rate contract is similar to a tolling agreement because fuel price risk is passed along to the off-taker.

However, depending on the structure of the heat rate contract, the entity may retain some exposure to fuel prices. Thus, the parties to a heat rate contract should not automatically conclude that it absorbs fuel risk of the entity. For example, if the heat rate in the contract is higher than the heat rate of the plant (i.e., because it is market-based rather than based on the operating profile of the power plant), profitability will fluctuate with changes in natural gas prices. In a heat rate contract, the off-taker may pay for (or supply) a specified amount of natural gas, based on the specified heat rate. If the heat rate is higher than the plant heat rate, the off-taker will pay more for natural gas than will be purchased by the plant operator for use in generation. As a result, the entity retains exposure to fuel price risk: as natural gas prices increase or decrease, the seller’s profit will increase or decrease irrespective of the efficiency of the power plant. For example, if natural gas prices increase from $2/MMBtu to $10/MMBtu, the seller’s net profit will increase.

Heat rate contracts should be evaluated to determine whether they are a net absorber of risk based on their specific facts and circumstances. In general, we would expect a heat rate contract to be a net risk absorber (and thus a variable interest).

Renewable energy projects

Renewable energy projects include wind, solar, geothermal, biomass, hydro, landfill gas, and other renewable sources. The risk profile of these types of power plants is significantly different from fossil fuel facilities. In some cases, such as wind or solar, production is highly dependent on the location of the facility and the availability of wind or the sun. Although the reporting entity can influence the success of the plant based on the initial strategic location decisions, ultimately the plant’s operations are heavily dependent on weather. In contrast, a biomass, geothermal, landfill gas, or hydro resource may have significantly higher reliability once the original source of supply is established. These reliability differences may impact the evaluation of whether a particular type of power purchase contract is a variable interest. Considerations in evaluating contracts with renewable facilities are discussed below.

Fixed-price contract, no production guarantee

In general, a power purchase agreement in a renewable energy project that establishes a specified price for the quantity provided (e.g., certain qualifying facilities contracts) with no production guarantee is likely a variable interest. For a typical renewable energy project, the ongoing cost of production is generally minimal and limited to the cost of operations and maintenance (there is usually minimal to no cost associated with the source of supply). As a result, a fixed-price sales agreement protects the entity from the commodity price risk associated with sales into the energy markets (i.e., the agreement absorbs risk from the entity and the entity has less risk with the contract).

Fixed-price contract, production guarantee

Consistent with the discussion above, a fixed-price contract with a production guarantee establishes a fixed price for the power delivered and thus protects the entity against commodity price risk. Therefore, the contract is absorbing risk from the entity. However, if the contract includes a production guarantee, it may also create some level of risk to the entity. In evaluating whether the contract is a variable interest, the reporting entity needs to evaluate the significance of the risk created. In many cases, such as a geothermal or biomass plant, production at some level may be virtually assured and a production guarantee may create minimal additional risk for the entity.

However, for less established technologies, especially when the contract is signed before there is any operating history, a production guarantee may create significant risk for the entity, depending on the level of the guarantee compared to the expected output. For example, if the entity has wind studies demonstrating an expected capacity factor for a facility of 65%, a 35% production guarantee will create much less risk than a 60% guarantee, depending on the reliability of the original studies. In evaluating this type of contract, the level of the guarantee (and associated default provisions), the reliability of production (based on experience with the same or similar projects), and any other uncertainties inherent in the project should be considered.

Variable-price contract

There are numerous existing qualifying facilities contracts with pricing linked to the price of natural gas, the incremental production price of the local utility, or other commodity-related benchmarks. Any linkage of payment for production from renewable energy projects to another commodity, such as natural gas, or to the utility’s cost of production creates a new risk for the entity. For example, a typical renewable project may not have any exposure to the price of natural gas; a contract linked to the price of natural gas creates a new exposure. Thus, this type of contract is a creator of risk and not a variable interest.

However, other types of variable-price contracts (e.g., contracts with linkage to the consumer price index or another index intended to replicate changes in employee costs) would need to be evaluated to determine whether and how the arrangement creates or absorbs risk. In general, any indexation or external price linkage should be evaluated to determine whether it introduces risk to the entity or absorbs a risk likely to be present.

Question 10-5 Are there any specific considerations for power purchase agreements that are derivatives?

PwC response

Yes. ASC 810 provides specific guidance for the evaluation of derivative instruments, focusing on whether the derivative will be a creator or absorber of risk for the entity. This guidance applies to all derivatives, including contracts that meet the normal purchases and normal sales scope exception. In addition, the guidance provides a helpful framework in considering all power purchase agreements.

The following characteristics, if both are present, are strong indications that a derivative instrument is a creator of variability:

a. Its underlying is an observable market rate, price, index of prices or rates, or other market observable variable (including the occurrence or nonoccurrence of a specified market observable event.

b. The derivative counterparty is senior in priority relative to other interest holders in the legal entity.

If the changes in the fair value or cash flows of the derivative instrument are expected to offset all, or essentially all, of the risk or return (or both) related to a majority of the assets (excluding the derivative instrument) or operations of the legal entity, the design of the legal entity will need to be analyzed further to determine whether that instrument should be considered a creator of variability or a variable interest.

In accordance with this guidance, if the derivative counterparty is senior to other interests in the entity and the pricing is based on a market-based index, the derivative is likely a creator of variability. If the contract is an absorber of risk, its seniority should be considered to determine if it will be treated as a variable interest. A derivative that has seniority to other interests is generally not a variable interest because its seniority would require both debt and equity holders to absorb losses before the derivative counterparty. In such cases, the derivative’s use as a risk absorber would be remote.

In analyzing common single power plant entities, the debt is often the most senior interest and the power purchase agreement is typically subordinate to the debt. In all cases, whether the power purchase agreement is a derivative or accounted for as an executory contract, the reporting entity should focus on the risks in the entity and whether the contract will create or absorb risk in evaluating whether it is a variable interest.

Question 10-6 Does the length of a contract factor into the variable interest determination?

PwC response

It depends. In evaluating whether a short-term offtake agreement (e.g., one year) could be a variable interest, the key factor to consider is whether a contract of limited duration will substantively impact the risk and economic performance of the entity.

For purposes of applying the Variable Interest Entities Subsections, only substantive terms, transactions, and arrangements, whether contractual or noncontractual, shall be considered. Any term, transaction, or arrangement shall be disregarded when applying the provisions of the Variable Interest Entities Subsections if the term, transaction, or arrangement does not have a substantive effect on any of the following:

a. A legal entity’s status as a VIE

b. A reporting entity’s power over a VIE

c. A reporting entity’s obligation to absorb losses or its right to receive benefits of the legal entity.

ASC 810-10-15-13B further states that applying this guidance is a matter of judgment. The FASB added these provisions to ensure that reporting entities consider substance over form in evaluating an entity’s structure and contractual relationships. In considering a single power plant entity, in some situations, a short-term arrangement (e.g., one month or one year) may not be a variable interest based on entity design or other factors.

10.2.3 Other potential variable interests

This section highlights key considerations in evaluating other interests that are often present in a single power plant entity structure.

10.2.3.1 Equity and debt interests

Equity and debt interests are among the most obvious forms of variable interests. Single power plant entities typically have at least one equity holder (e.g., common or preferred stock, partnership interests, membership interests). In addition, these entities usually issue other debt or equity interests, which may be structured as secured financings, preferred returns, or legal form equity. Factors to consider in the evaluation of debt and equity interests are discussed in ASC 810-10-55-22 through 55-24 and include:

Equity

If an equity investment is at risk, or if it absorbs or receives some of the entity’s variability, it is a variable interest. In general, legal form equity investments are variable interests unless the source of funds for the investment did not come from the investor or the investor is protected from losses. See UP 10.3.1.1.1 for further information on equity investments and what constitutes “at risk.”

Senior beneficial interests or senior debt

ASC 810-10-55-24 states that the senior beneficial interests and senior debt instruments normally would absorb a minimal amount of a VIE’s variability. However, it further states that all liabilities of a VIE may be variable interests because a decrease in the fair value of the VIE’s assets could be so great that the decrease is absorbed by all liabilities. Therefore, senior debt may be a variable interest.

Subordinated beneficial interests or subordinated debt

These interests are likely variable interests because they would be expected to absorb all or a part of the expected losses of the entity.

Debt and equity financing for single power plant entities may take multiple forms, but are typically designed to absorb risk and expected losses from the entity. Therefore, almost all debt or equity holders likely are variable interest holders. See CG 3.3 for further information.

10.2.3.2 Lease agreements (entity is the lessee)

The evaluation of leases in UP 10.2.2.1 is focused on situations where the entity is the lessor of a facility. However, in some cases, such as a sale-leaseback transaction or a ground lease in the case of a renewable facility, the single power plant entity itself may be a lessee. Such transactions, in substance, are considered financing arrangements and should be assessed using the guidance for debt interests. Therefore, we would generally expect leases where the VIE is the lessee to be variable interests.

10.2.3.3 Management and service agreements

It is common for single power plant entities to enter into various service or management-type agreements, including:

• Operations and maintenance agreements

• Long-term service agreements for major maintenance

• Fuel-supply agreements (fee for service with a separate charge for fuel)

• Accounting and administrative service agreements

• Engineering, procurement, and construction contracts for the construction of a power plant

In accordance with ASC 810, all types of service contracts are evaluated in a similar manner. The guidance distinguishes between a service provider whose role is fiduciary in nature (such arrangements would not be variable interests) and a provider whose role is not (such arrangements may be variable interests). Under ASC 810-10-55-37, arrangements with decision makers or service providers do not represent variable interests if all of the following criteria are met:

• The fees are compensation for the service and are appropriate based on the level of effort involved.

• The decision maker or service provider (including certain related parties) do not hold other interests in the VIE that alone or in the aggregate would absorb more than an insignificant amount of the expected losses or receive more than an insignificant amount of the expected residual returns of the VIE.

• The service agreement has terms and conditions that are customary and consistent with arm’s length contracts for similar services.

We would generally expect a standard operations and maintenance, accounting and administrative, or long-term maintenance agreement with a third party to meet these criteria. However, the terms and conditions should be carefully considered. For example, if the service provider’s operations and maintenance agreement is otherwise standard but includes a significant output guarantee, the arrangement would generally be considered a variable interest. In addition, there are specific considerations in evaluating contracts with related parties.

Related party interests

When evaluating whether a service agreement is a variable interest, a reporting entity should consider the interests held by related parties. An interest held by a related party that is under common control with the reporting entity would be considered a direct interest held by the reporting entity. All other related party interests would be included in the analysis based on its proportionate share of the interest. For example, a reporting entity that holds a 30% interest in a related party that has a 10% equity interest in the potential variable interest entity would include a 3% indirect equity interest in the analysis (30% x 10% = 3%).

10.2.3.4 Agreements to purchase green attributes

Renewable energy credits generated from a renewable energy plant may be sold to the purchaser of the power (embedded in a power purchase agreement) or may be sold separately. In determining whether all or a portion of this type of multiple-element agreement is a variable interest, reporting entities should consider the role of the RECs in the design of the entity. In addition, a reporting entity’s determination of whether RECs are output from the facility will affect this analysis, because it may impact the determination of whether the power purchase agreement is a lease. See UP 7.3.2 for further information about the evaluation of RECs as output.

A reporting entity should apply the framework used in evaluating sales of energy from a renewable facility in assessing these arrangements. Figure 10-5 summarizes key considerations in evaluating whether the sale of RECs is a variable interest.

Figure 10-5 Sales of RECs: considerations for the variable interest analysis

Type of sale

Evaluation

Considerations

Contract contains a lease — RECs are output

The sale of RECs is part of the use of the facility; no separate evaluation of the sale of RECs is required.

An operating lease qualifies for a specific exception and is not a variable interest1

Capital leases are often not variable interests in the entity. Refer to discussion in UP 10.2.2.1

Contract contains a lease — RECs are not output

Sale of RECs is not part of the lease arrangement and is accounted for separately; evaluate as potential variable interest.

Fixed-price contract generally absorbs risks from the entity; likely a variable interest

A minimum quantity guarantee should be evaluated because it may create risk; further evaluation may be required

REC sale included in a non-lease power purchase agreement

Evaluate as part of overall power purchase agreement; no separation required.

Entire contract should be evaluated as a potential variable interest

Stand-alone sale of RECs

A stand-alone REC sale may be a variable interest.

Fixed-price contract generally absorbs risks from the entity; likely a variable interest

A minimum quantity guarantee should be evaluated because it may create risk; further evaluation may be required

1The REC is a lease element and is embedded in the contract as a component of the operating lease; therefore, it does not create or absorb any variability in the entity.

In general, a REC sale at a fixed price will absorb risk from the entity and will be a variable interest. However, if there is a minimum guarantee, further evaluation is required to determine whether the guarantee creates risk for the entity. See UP 10.2.2.2 for further information on evaluation considerations.

10.2.4 Joint plant arrangements

Many electric utilities have interests in a joint plant whereby two or more utilities own an undivided interest in the underlying power plant assets. Because of the structure of those arrangements (i.e., undivided interests in the assets rather than an interest in an entity), the VIE guidance generally does not apply. See UP 15.3 for further information.

1 Note—For simplicity, the remainder of this section refers to the evaluation considerations in the context of a power purchase agreement. However, the same considerations would apply in the evaluation of elements embedded in a lease. See UP 10.6 for application examples that include embedded elements.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.