This section comprises a series of hypothetical scenarios to illustrate considerations in evaluating whether a contractual or other arrangement is a variable interest and in determining the primary beneficiary in evaluating single power plant entities. These examples have been simplified, and different facts may significantly change the analysis. All of the examples assume that the entity is a VIE and the analysis is from the perspective of the developer. Similar considerations would apply to other variable interest holders. The analysis included in the examples does not apply to all scenarios, and a careful evaluation of all relevant facts and circumstances should always be performed for each specific fact pattern.

EXAMPLE 10-4

Tolling agreement that is not a lease

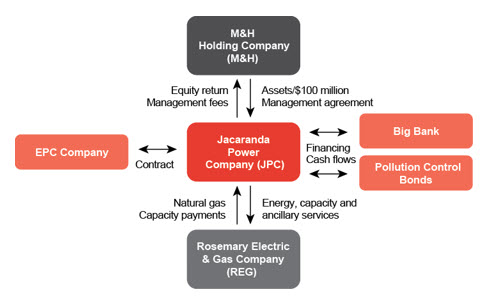

M&H Holding Company establishes a wholly owned subsidiary, Jacaranda Power Company (JPC), to design, construct, own, and operate a 500 MW combined-cycle natural gas-fired facility. M&H contributes land, air permits, and a turbine to JPC during the preconstruction phase. M&H also contributes $100 million in equity, approximately 30% of the expected construction cost of $325 million. M&H spends one year obtaining the remaining necessary permits, bargaining with an EPC contractor (EPC Company), identifying sources of construction financing, and negotiating a tolling agreement with the local utility. During the initial development stage, M&H holds the only interests in JPC and accounts for it as a consolidated subsidiary.

Construction and operations

On August 1, 20X1, the state regulator approves a proposed tolling agreement and JPC executes certain agreements:

- A 30-year tolling agreement with Rosemary Electric & Gas Company for all of the energy and capacity from the plant. Under the terms of the agreement, REG will supply natural gas to the facility and will receive electricity based on a 7.00 heat rate. The plant is expected to be operated as a base-load plant and REG will pay a fixed price for capacity, escalated annually by 2%. REG determines when to dispatch; there is no separate energy charge. The plant must have at least 90% availability; and REG has approval over operations and maintenance schedules. JPC must pay liquidated damages if the plant is not operational by a specified date. REG has certain step-in rights in the event of default. JPC determines that the contract does not meet the definition of a lease or a derivative and accounts for the agreement as an executory contract.

- Senior debt financing from Big Bank for $175 million of the cost of plant construction. Under the terms of the debt agreement, the borrowings are repaid annually for the first 10 years after the commercial operation date. The senior debt financing agreement also includes certain protective rights (e.g., approval over the sale of the plant).

- JPC also issues pollution control bonds for the remaining cost of construction. The pollution control bonds will be paid after the senior debt is fully repaid and must be fully retired 20 years after COD.

JPC also enters into an agreement with EPC Company, an unrelated construction company, for construction of the plant. The plant will be built to JPC’s specifications and construction, will have a 35-year life, and will be managed by M&H under a management agreement. EPC Company is required to pay JPC liquidated damages if the plant does not achieve commercial operation by a specified date. In addition, M&H will be responsible for operations and maintenance of the facility. The following diagram summarizes JPC’s key contractual agreements and other arrangements:

At the time of execution of the agreements, M&H performs an assessment and determines that JPC is exposed to the following risks:

- Construction risk associated with constructing the facility

- Operational risk associated with maintaining capacity as required by the contract (if capacity is not maintained, the debt and equity holders will not be fully repaid)

- Credit risk associated with possible default by the counterparty to the tolling agreement

- Commodity price risk associated with fuel and energy prices. During the contract period, the commodity price risk is absorbed by the tolling agreement. The plant is exposed to fuel and energy price risk beyond the initial contract period; however, given that the contract is for 30 years and the plant has a 35-year life, the risk beyond the initial contract is relatively minimal.

M&H evaluates the purpose and design of the entity as follows:

- The primary purpose for which the entity was created was to provide REG with use of the plant for 30 years, with substantially all of the benefits and obligations of ownership. JPC retains operational responsibility, and its ability to obtain the expected payments under the tolling agreement is dependent on its ability to operate the plant within the specified capacity and heat rate parameters. However, REG decides when to operate the plant and retains fuel cost exposure.

- The tolling agreement is designed to absorb energy price risk associated with the output during the contract period (30 years out of the expected 35-year useful life of the plant). This contract transfers a significant amount of the energy and capacity price risk to REG. The contract period will be sufficient to repay the debt holders and provide M&H with its expected return. M&H will retain exposure to expected fluctuations in the value of the property after year 30; however, any residual is considered upside by M&H.

- JPC was marketed to the lenders as an entity that is exposed to credit risk associated with the tolling agreement. The debt is senior to the tolling agreement. REG is a regulated utility with a strong credit rating. However, the transaction still involves credit risk, particularly due to the duration of the contract.

- JPC is exposed to construction risk with respect to completion of the generating facility in accordance with specified standards. M&H has a history of successfully completing similar projects and the EPC contractor has built numerous similar plants. Management does not anticipate significant variance from the budgeted overruns, based on historical experience and the nature of the plant.

What are the variable interests and the significant activities during each phase of the project?

Analysis

Based on the above analysis, M&H concludes that JPC was designed to create and pass along construction, operations, and credit risk to M&H and the lenders. It was also designed to create and pass along price risk related to the plant assets to REG through the tolling agreement. M&H also retains exposure to variability of cash flows in the period after expiration of the tolling agreement.

The potential variable interests are as follows:

Interest | Create or absorb risk? | Evaluation |

M&H equity interests | Absorb | Variable interest—Equity is the junior interest and is paid last ( ASC 810-10-55-23). |

Senior debt | Absorb | Variable interest—Even senior debt is exposed to potential losses ( ASC 810-10-55-24); however, the risk of significant loss is slight. |

Pollution control bonds | Absorb | Variable interest—Subordinated debt is exposed to potential losses ( ASC 810-10-55-24). |

Tolling agreement | Absorb | Variable interest—The contract locks in future commodity price and protects JPC from commodity price risk (see further discussion of key evaluation factors in UP 10.2.2.2). |

EPC contract | It depends | The agreement may meet the service contract scope exception. Judgment is required to determine if the liquidated damage provisions are customary in these types of arrangements (see UP 10.2.3.3). |

Management contract, including operations and maintenance | Absorb | Variable interest—The contract payments are made to a decision maker, but the contract does not qualify for the service agreement exception because the decision maker holds other variable interests that would absorb more than an insignificant amount of the VIE’s expected residual returns (see UP 10.2.3.3). |

All variable interest holders have the obligation to absorb losses of the entity or the right to receive benefits from the entity that could be significant. Therefore, as all variable interest holders would meet the second criterion of

ASC 810-10-25-38A, further evaluation would be performed to determine which of the parties has the power to direct the activities of the VIE that most significantly impact its economic performance.

The most significant activities during the power plant life cycle are as follows:

|

|

Initial strategy, siting, and other activities to prepare for construction

Contracting, financing and regulatory approvals

|

M&H (no other variable interests during this stage)

|

|

Completion of construction

|

M&H (through equity and management contract) and EPC Company are both involved in significant decisions over construction. REG is entitled to liquidated damages in the event of default, but has no specific powers during this phase.

|

Operations— contracted period

|

Operations and maintenance

Dispatch

|

M&H and REG each have responsibility for certain activities; see further evaluation below.

|

|

Same as initial contracted period

|

Depends on whether M&H enters into a new contract or operates the plant as a merchant facility

|

Construction phase

Once the financing is in place and the tolling agreement is executed, JPC signs the EPC contract. The EPC contractor will be managed by M&H through a management agreement; however, the contractor is responsible for construction of the plant in accordance with the specifications established by M&H and approved by REG. EPC Company will be required to pay liquidated damages to M&H if construction is not completed and commercial operation is not achieved by a specified date.

M&H determines that the initial strategy and contracting as well as control of operations, as further described below, are expected to have more significant impact than construction on JPC’s economic performance over the life of the entity (which is expected to be the same as the life of the facility).

Who is the primary beneficiary of JPC during the construction phase?

Analysis

Although the EPC contract is important, there is not significant risk with construction because the contractor is experienced and the technology has been proven. As such, M&H would deem it highly likely that construction will be completed and that the plant will enter the operations phase. As a result, M&H would conclude that it is the primary beneficiary.

Operations — contracted period

During the contract period, M&H and REG will have responsibility for certain activities as follows:

- Operations and maintenance — M&H

- Dispatch — REG

- Fuel procurement — because of the structure of the contract (tolling agreement), the fuel procurement strategy does not have a direct impact on JPC’s economic success. Fuel price risk is absorbed by the tolling agreement with REG.

Who is the primary beneficiary of JPC during the contract period?

Analysis

M&H had responsibility for the initial development of the project, contracting, and strategy. The significant activities during the operational phase are operations and maintenance, and dispatch. The determination of which of these activities is more significant depends on the terms of the tolling agreement. Because all cash flows to JPC are obtained through the capacity payment, M&H would likely conclude that operations and maintenance (leading to availability) is the most important activity. In contrast, if the contract terms resulted in substantially all of the cash flows being obtained through start-up charges and the energy payment, dispatch may be more important. In this case, because operations and maintenance was determined to be the most significant activity, M&H would be considered the primary beneficiary.

Post-contract

At the time the tolling contract ends, M&H would need to reassess significant activities and control based on any contractual agreements put in place after the initial contract period.

Debt holder considerations

Throughout the life cycle of the power plant, the debt holders do not have the power to direct activities that most significantly impact JPC’s economic performance; therefore, they are likely not the primary beneficiary at any stage. The rights held by the debt holders have the characteristics of protective rights, rather than providing any substantive controlling financial interest. The debt holders would need to include appropriate disclosure of their interests in their separate financial statements.

EXAMPLE 10-5

Tolling agreement that is a lease

Assume the same facts as in Example 10-4; however, the fixed pricing in the tolling agreement escalates annually by changes in the Consumer Price Index. M&H Holding Company concludes that the contract is an operating lease. M&H assesses the design of the entity and the related risks. It concludes that the only difference from the evaluation performed in Example 10-4 is that risk associated with the inputs and outputs of the facility has been designed out of the entity during the contract period because of the lease arrangement with Rosemary Electric & Gas Company.

Who is the primary beneficiary of JPC?

Analysis

The tolling agreement is not a variable interest because it is an operating lease. However, the lease includes an embedded operations and maintenance agreement (generally represented by a portion of the energy payments). The operations and maintenance agreement absorbs risk from the entity by reducing the variability of JPC’s cash flows compared to operation as a merchant facility, which would not have an operations and maintenance contract. Although there is some uncertainty because payments will not be made unless the plant dispatches, the facts indicate that the plant is expected to be operated as a base-load plant, with a 90% capacity factor. Therefore, M&H would likely conclude that REG holds a variable interest in JPC via the operations and maintenance agreement embedded in the lease.

In evaluating the most significant activities, the key change as a result of the conclusion that the contract is a lease is that fuel procurement and dispatch are generally outside the scope of the VIE’s activities. The lease is for the use of the power plant itself. Thus, the production inputs and the output from the plant are associated with the lease contract itself and are outside the design of the entity. In this fact pattern, the plant is base load and expected to dispatch whenever available. Therefore, in assessing the most significant activities, operations have the most significant impact on the VIE’s economic performance. M&H would therefore be the primary beneficiary of the VIE because it controls operations.

In this example, REG does not make any separate payments for dispatching the plant. However, if the lease payments included a component based on dispatch, JPC would retain the risk of variability in payments related to these contingent rents. In such cases, M&H would need to assess the relative importance of operations as compared to dispatch in determining which activities are most significant.

EXAMPLE 10-6

Fixed-price power purchase agreement that is not a lease

Assume the same facts as in Example 10-4; however, the agreement is a fixed-price power purchase agreement. JPC is responsible for procuring its own fuel and will sell capacity and energy to Rosemary Electric & Gas Company (REG) at fixed prices as established in the contract, escalated annually by CPI. REG is required to take all power produced by the entity and has no dispatch rights. At the time the energy sales agreement is signed, JPC signs natural gas supply agreements for the first five years of operations. M&H Holding Company, JPC’s equity holder, identifies an additional risk—fuel-supply risk created by the fixed-price power purchase agreement. The purpose and design of the entity are considered as follows:

- The primary purpose for which the entity was created was to provide REG with an assured source of supply at a fixed price and to provide the equity holders with a return. M&H, the owner of JPC, retains operational responsibility and substantially all of the risks of ownership, including fuel-supply risk. JPC’s ability to obtain the expected payments under the power purchase agreement is dependent on its ability to operate the power plant within the specified capacity parameters.

- The offtake agreement provides JPC with an expected payment stream for 30 years of the expected 35-year useful life of the plant. The contract period is expected to be sufficient to repay the debt holders and provide M&H with its expected return. However, its ability to make these payments is highly dependent on its ability to obtain fuel at prices low enough to make a profit. JPC also will retain exposure to expected fluctuations in value of the property after year 30.

- JPC was marketed to the lenders as an entity that is exposed to credit risk associated with the power purchase agreement with REG. REG is a regulated utility with a strong credit rating. However, the transaction still involves credit risk, particularly due to the duration of the contract.

- There is no change in construction risk compared to Example 10-4.

Who is the primary beneficiary of JPC?

Analysis

In evaluating the potential variable interests, the power purchase agreement is a creator of risk due to the fuel-supply risk that it has introduced into the entity structure. The same conclusions as in Example 10-4 regarding the other variable interests apply to this example.

As M&H controls fuel, dispatch, and operations and maintenance, it is the primary beneficiary.

EXAMPLE 10-7

Outsourced operations and maintenance

Assume the same facts as in Example 10-4 above; however, M&H Holding Company contracts with a third party to provide operations and maintenance services to Jacaranda Power Company (JPC). M&H can replace the operations and maintenance service provider for any reason with one-year notice. It can also replace the operations and maintenance provider for cause at any time. The services will be provided as specified in the contract, with general oversight by M&H. M&H analyzes the contract in accordance with the guidance in

ASC 810-10-55-37, and determines that the operations and maintenance agreement is not a variable interest because it meets all of the criteria for the service provider exception.

Who is the primary beneficiary of JPC?

Analysis

The operations and maintenance provider is working at M&H’s direction under standards established by M&H, and M&H can, at its own discretion (subject to the terms of the contract), replace the operations and maintenance provider. As a result, M&H still has the power to direct the operations and maintenance activities. As such, there would be no change to the conclusion reached in Example 10-4 and M&H would be the primary beneficiary.

Note that additional evaluation should be performed if the operations and maintenance agreement was for a longer duration and did not provide for oversight by M&H or the ability of M&H to replace the third party.

EXAMPLE 10-8

Tolling agreement with a call option

Assume the same fact pattern as Example 10-5 (tolling agreement is a lease); however, Rosemary Electric & Gas Company (REG) has the contractual right to call the plant for a fixed price at the end of the contract period. The pricing of the call option is such that REG would be expected to exercise the option at the end of the tolling period. M&H Holding Company concludes that this call option is a variable interest in accordance with

ASC 810-10-55-39.

Who is the primary beneficiary of JPC?

Analysis

The determination of the primary beneficiary should be based on the existing rights and powers held by the various parties to the VIE and the impact of those powers on the entity’s economic performance during its life. If the same or substantially the same powers are held by different parties at different times in the entity’s life, those powers should be attributed to the entity holding them at the reporting date. During the initial phase, M&H had control of strategy and contracting; however, it agreed to cede this power to REG at the end of the contract term pursuant to the power purchase agreement. M&H also retains operational control of the power plant during the initial contract period.

The call option would not change the determination that M&H is the primary beneficiary during the contract period as determined in Example 10-5 because the powers provided by the call are substantially consistent with the powers held by JPC during the initial contract period. Because the powers are similar in nature, they are considered only by the party that holds them as of the reporting date. The expectation of control in the future is not part of the current primary beneficiary analysis. REG’s ability to exercise power over the activities is contingent upon exercise of the call option and would not become effective until that occurs. However, given the significance of the call option, M&H should disclose this variable interest and the potential for the future call in the notes to its financial statements.

EXAMPLE 10-9

Renewable energy project

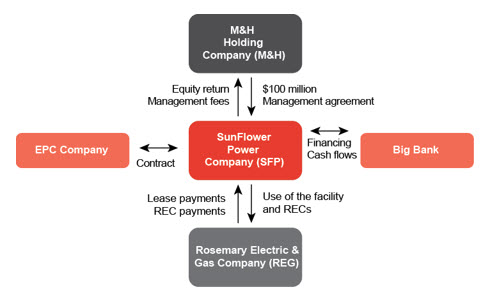

M&H Holding Company (M&H) decides to expand into renewable resources and establishes a wholly owned subsidiary, SunFlower Power Company (SFP), with the intention of building a 100 MW solar facility. M&H intends to finance the solar plant with a combination of additional equity and debt. M&H spends six months conducting solar studies, obtaining land leases, ordering solar panels, and performing other activities in preparation for construction. M&H provides $100 million in initial equity financing. On March 12, 20X2, SFP executes the following agreements:

- A 20-year agreement with Rosemary Electric & Gas Company (REG) for the sale of all energy and renewable energy credits from the solar facility. The contract price is based on a fixed price for energy, escalated annually based on a CPI, plus $25 per renewable energy credit. The price for renewable energy credits will also increase annually in accordance with changes in the CPI. SFP guarantees a minimum availability of the plant of 30% and REG is required to take all energy and RECs produced. REG has certain step-in rights in the event of default during the construction and operations phases and has approval rights over the timing of operations and maintenance activities. M&H determines the contract is an operating lease.

- Senior debt financing from Big Bank for the remaining $350 million of the cost of construction. The debt is repaid annually for the first 10 years after the commercial operation date and includes certain protective rights (e.g., approval over the sale of the power plant).

M&H has previously adopted an accounting policy that RECs are not output (see

UP 7 for more information about accounting for RECs). It separately evaluates the REC sale as part of a multiple-element arrangement and accounts for the forward sale of RECs as an executory contract.

SFP also enters into an agreement with EPC Company, an unrelated construction company, for construction of the plant. The plant will be built to SFP’s specifications and construction will be managed by M&H under a management agreement. In addition, M&H will be responsible for operations and maintenance of the facility. The following diagram summarizes SFP’s key contractual agreements and other arrangements:

This example does not further discuss the construction phase because the considerations are similar to those discussed in Example 10-4. M&H determines that SFP is exposed to the following risks:

- Construction risk associated with constructing the facility

- Operational risk associated with the level of production from the plant (if there is not sufficient production, the debt holder and M&H will not be fully repaid)

- Credit risk associated with possible default by REG

- Energy and REC price risk beyond the contract period; the 20-year contract period is expected to be sufficient to fully repay the debt and equity holders, including a return.

M&H evaluates the purpose and design of SFP as follows:

- The primary purpose for which the entity was created was to provide REG with the use of the facility and the RECs for a 20-year period (the regulated utility needs the credits to meet the state renewable-portfolio standards). As a result of the production guarantee, SFP takes on additional operational risk that there will be sufficient sunlight to meet the minimum availability requirements. In addition, SFP retains operational responsibility and its ability to obtain the expected payments under the power purchase agreement is dependent on the initial siting of the plant, weather and solar conditions.

- The 20-year offtake agreement provides REG with benefit over that period. The contract period is expected to be sufficient to repay the debt holders and to provide M&H with its expected return. M&H retains exposure to expected fluctuations in the value of the property after year 20; however, it considers any residual as potential upside.

- SFP was marketed to the lenders as an entity that is exposed to credit risk associated with the power purchase agreement and production risk associated with initial siting of the plant (see further discussion below) and production levels that are dependent on weather. REG is a regulated utility with a strong credit rating; however, the transaction still involves credit risk, particularly due to the duration of the contract.

- The entity is exposed to construction risk with respect to completion of the solar facility in accordance with specified standards. M&H performed solar studies and obtained other support for the expected level of production; however, this is its first venture into renewable power plants.

Based on the above analysis, SFP was designed to create and pass along construction, operational, and credit risk to M&H and the lenders. In addition, REG may have risk associated with the RECs because they are dependent on production.

Who is the primary beneficiary?

Analysis

The potential variable interests are as follows:

Interest | Absorb or create risk? | Evaluation |

M&H equity interests | Absorb | Variable interest — equity is the junior interest and will be paid last ( ASC 810-10-55-23). |

Senior debt | Absorb | Variable interest — even senior debt is exposed to potential losses ( ASC 810-10-55-24). |

Power purchase agreement | Not applicable | Not applicable — the power purchase agreement is an operating lease and qualifies for the operating lease exception in ASC 810-10-55-39. However, M&H concludes that the power purchase agreement also includes an operations agreement (see management contract below). |

REC sale included in the power purchase agreement | Absorb | Variable interest — the REC sale absorbs price risk from the entity. M&H considers whether the minimum production guarantee creates risk; however, it has studies that indicate an expected capacity factor of 65%, well in excess of the 30% minimum. Therefore, this risk is deemed minimal and does not impact the conclusion that the REC sale is a variable interest. |

EPC contract | It depends | Variable interest — the EPC contract may qualify for the service contract exception (see UP 10.2.3.3). |

Management contract, including operations and maintenance | Absorb | Variable interest — the payments are made to the decision maker, but the contract does not qualify for the service agreement exception because the decision maker holds other variable interests that would absorb more than an insignificant amount of the VIE’s expected residual returns (see UP 10.2.3.3). |

All variable interest holders have the obligation to absorb losses of the entity or the right to receive benefits from the entity that could be significant. Therefore, further evaluation is necessary to determine which of the parties has the power to direct the activities of the VIE that most significantly impact its economic performance.

Both Big Bank and REG hold protective rights in the entity. However, M&H is the only entity with any power to direct the activities. Although REG has approval rights over the schedule of operations and maintenance activities, M&H has overall responsibility. Therefore, M&H would be considered the primary beneficiary.

EXAMPLE 10-10

Renewable energy project — renewable energy credits are output

Assume the same facts as in Example 10-9; however, M&H Holding Company’s accounting policy is that RECs are part of the output of the facility (see

UP 7 for further information about accounting for RECs).

Who is the primary beneficiary?

Analysis

Because the RECs are output, the RECs are part of the operating lease and do not represent a separate variable interest (the REC output is obtained from use of the facility). However, the REC accounting policy does not change any of the powers held by the parties. Therefore, M&H would still be the primary beneficiary, consistent with the analysis in Example 10-9.

EXAMPLE 10-11

Renewable energy project — certain shared powers

Assume the same facts as in Example 10-9; however, M&H Holding Company obtains a portion of the financing for SunFlower Power Company (SFP) from a tax equity investor, Desert Sun Tax (DST), a wholly-owned subsidiary of a U.S.-based C-Corporation. Under the terms of the agreement, DST will provide $65 million in initial financing in exchange for all of the production tax credits and priority in distribution. DST will receive 90% of the distributions until its equity contribution is fully repaid or a specified investment return has been achieved, at which time its share will be reduced to 10%. DST participates on the management committee with M&H and all major decisions (e.g., sources of additional financing, budgets, project expansion) require agreement from both parties. M&H will be responsible for all day-to-day operations under a management agreement. DST can unilaterally replace M&H in the event of default; otherwise, a change in operator requires agreement from both parties.

Who is the primary beneficiary?

Analysis

DST’s investment is a variable interest because it has exposure to losses and will absorb a portion of the risk from the entity. M&H would also need to consider whether DST’s participation in the management committee and shared involvement in major decisions would impact the determination of the primary beneficiary. Key considerations in this evaluation include:

- M&H was responsible for the initial design of the entity and conducted certain pre-development activities before DST became involved. As further discussed in UP 10.4.1.6, involvement in initial design is a factor in the determination of the primary beneficiary. M&H is the operator and has day-to-day power over operations. Absent a default, M&H cannot be replaced without its consent.

- The activities that will most significantly impact the success of the entity were substantially determined during the development stage, including determining the sources (and cost) of financing, siting the facility, negotiating the power purchase agreement, and obtaining all necessary permits. These activities were conducted by M&H.

- After initial development, the activity with the most influence over performance is operation of the facility. M&H holds this power through its management agreement and, as noted, cannot be replaced unless it agrees to such replacement, absent default.

- Because of the nature and purpose of the entity, the decision-making powers held by the management committee (approval of budgets, expansion of the project, new contracts) are not expected to have a significant impact on SFP’s economic performance. However, any significant changes in strategy could have a material impact on SFP’s economic performance.

Based on the factors outlined above, there is a bias that M&H retains the power over the significant activities of SFP. It established the initial design, is responsible for managing operations, and would share power over any other decisions significantly impacting the economic performance of the plant. Although certain powers are shared such that no one party has the power to direct those activities, M&H alone holds additional powers with the ability to impact SFP’s economic performance. Based on these factors, M&H would be the primary beneficiary.

EXAMPLE 10-12

Renewable energy project — energy and renewable energy credits sold to separate off-takers

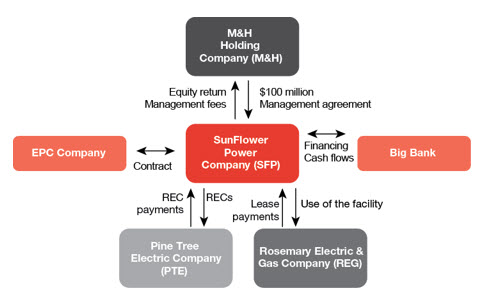

Assume the same facts as in Example 10-9; however, two years after the project commences operations, Rosemary Electric & Gas Company (REG) determines that it no longer needs the RECs. SunFlower Power Company (SFP) and REG agree to a termination payment that is approved by Big Bank on the condition that SFP sign a replacement agreement for equal or greater value. REG will continue to buy the energy at the scheduled price in the contract. SFP negotiates an agreement with Pine Tree Electric Company (PTE) to purchase the renewable energy credits for $30 each, increasing annually by the CPI.

Who is the primary beneficiary?

Analysis

As a result of this change, the primary beneficiary should be reassessed. The PTE contract was signed after the power plant was already in operation, which suggests that it may not have been contemplated in the design. However, the financing agreements required approval of any change to the contracting parties and would not permit termination of the original REC sale without a replacement. Furthermore, the REC sale absorbs risk from the entity. Therefore, PTE holds a variable interest. In addition, because M&H has an accounting policy that RECs are not output, there is no change to its conclusion that the arrangement with REG is a lease. There is no change to the evaluation of any of the other variable interests.

The following diagram summarizes SFP’s key contractual agreements and other arrangements:

Based on the above, there is no change to the primary beneficiary conclusion reached in Example 10-9 and M&H is still the primary beneficiary. Although the variable interest holders have changed, M&H is still the primary beneficiary because it is the only entity with the power to direct SFP’s significant activities.

EXAMPLE 10-13

Renewable energy project — prepaid power agreement

Assume the same facts as in Example 10-9; however, M&H Holding Company cannot identify an economic source of debt financing. Therefore, in lieu of the senior debt from Big Bank, M&H negotiates with Rosemary Electric & Gas Company (REG) to prepay a substantial portion of the power purchase agreement. In exchange, REG will receive a discount on the energy and REC purchases over the life of the agreement.

Who is the primary beneficiary?

Analysis

The change in financing does not change the conclusion that the contract is still a lease; however, the contract now also includes an additional embedded element, the initial payment. The initial payment represents a source of financing and is effectively a debt instrument. Therefore, the prepaid amount is a variable interest. However, as the powers to direct the significant activities of the entity have not changed, M&H would still be determined to be the primary beneficiary.