As discussed in

UP 2.2.3, the right to control the use of an identified asset is conveyed if the customer (1) has the right to obtain substantially all the economic benefits from use of the identified asset and (2) has the right to direct the use of the identified asset.

The economic benefits produced by a renewable generation facility (i.e., energy, RECs) differ from those produced by a storage asset (i.e., storage capacity). Similarly, the relevant decisions that impact the use of a generation facility are different from the significant decisions impacting an energy storage asset. As such, proper identification of the unit(s) of account is critical in determining whether a storage arrangement contains a lease.

Right to obtain substantially all the economic benefits

The reporting entity should consider whether it has a right to substantially all of the economic benefits from the storage system. The off-taker’s ability to use the storage and related dispatched energy is a strong indicator that it has a right to substantially all of its economic benefits from the storage system. If the customer has the option to consume all of the output of the battery before it is dispatched to the grid or can prevent others from consuming the output (right of first refusal), the arrangement likely meets this criterion.

Right to direct the use of the identified asset

Determining whether the off-taker has the right to use the identified asset requires an evaluation of the decision-making rights within the arrangement that directly impact the timing, occurrence, and quantity of economic benefits from using the storage system. Relevant decisions occurring during the term of a contract for a storage system generally include the following:

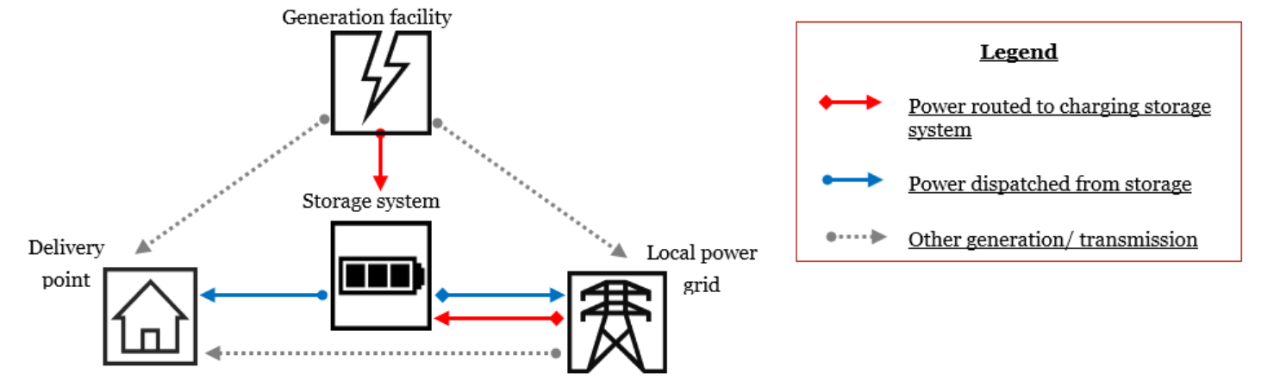

- Source of charging the system (e.g., is a battery charged from the generation facility or the power grid)

- When the storage system is charged

- When and to where stored energy is dispatched from the system

- Where the storage system is located (and if it can be easily moved)

Evaluating whether a contract conveys the right to direct the use of an identified asset focuses only on decisions that can be made during the period of use of the asset. In some cases, some or all the decisions about how and for what purpose the storage system is used may be predetermined. For example, if a battery system connected to a solar facility is automatically fully charged before generated power is dispatched to the grid, some of the decisions around charging may be predetermined. However, other decisions (such as whether power from the grid will be stored by the off-taker or when stored power is dispatched) are still relevant and should be evaluated to determine who holds those rights.

In addition to the relevant decisions noted above, a hybrid storage project will typically require that some operational activities (e.g., maintenance, scheduling, metering, communications management) to occur throughout the contract term. Operation of the system does not generally constitute a “relevant decision” under

ASC 842 as it typically relates to implementing (rather than directing) decisions that impact the asset’s economic productivity.

Question UP 2-11

Do automated charging and dispatching processes preclude a customer from having the right to control the use of a storage system?

Not necessarily. Software can be used to automate charging and dispatch for a storage system. For example, a storage system may be configured to automatically charge using power from a renewable generation facility during periods when demand is below a certain threshold and to dispatch power to a specified delivery point during peak hours. This configuration may be contemplated in the design of the hybrid storage and outlined in the agreements. In these situations, reporting entities must determine whether there are other relevant decisions impacting how and for what purpose the storage system is used (e.g., whether the automated orders can be overridden and/or changed during the period of use) then evaluate who holds those rights. If the customer can override or change any predetermined or automated settings, it will generally have the ability to control the use of the storage system. Furthermore, if the supplier is contractually required to dispatch the energy from the storage system at the customer’s direction or in response to the customer’s demand, the customer would typically have the right to direct the use of the storage system even if the dispatch process is automated.

Example UP 2-9 illustrates the evaluation of whether a hybrid power purchase and storage agreement contains a lease.

EXAMPLE UP 2-9

Battery storage system linked to renewable generation facility

Sunflower Power Company (SPC) owns and operates a 100 MW hybrid renewable battery storage project, SunGen. Rosemary Electric & Gas Company (REG) enters into a contract with SPC to purchase all of the capacity, electricity, and environmental attributes produced by the solar facility as well as all of the storage capacity of the attached battery system for use during a 10-year term. The contract specifies that the SunGen assets (a solar generation facility and an attached battery system) will be used to fulfill the contract. SPC does not have substantive substitution rights and cannot use the project for any other purpose or customer during the contract term.

REG was not involved in designing the project before it was constructed. SPC is responsible for operating and maintaining the project’s solar generation and battery system to satisfy minimum technical requirements. There are no decisions to be made about whether, when, or how much electricity will be produced from the solar generation facility due to the nature of the facility.

The battery system can be charged using power generated by the attached solar facility or from the grid. The contract authorizes REG to determine when the battery is charged, whether it is charged using grid power or by the SunGen solar facilities, and when any stored power is dispatched, subject to any operational limitations and dispatch parameters. REG pays SPC an energy charge for the power, RECs, and capacity from the solar facility, as well as a fixed capacity payment for use of the attached battery system.

Because the battery system and solar facility may be operated independently, the parties conclude that the use of the solar facility and the battery system are two identified assets. Does the hybrid power purchase agreement contain one or more leases?

Analysis

As the hybrid power purchase agreement contains two identified assets, REG would separately evaluate whether the hybrid power purchase agreement contains an embedded lease of either (or both) the solar generation facility and the battery system.

SunGen, solar generation facility

REG’s agreement to purchase the capacity, electricity, and environmental attributes from SPC does not meet the definition of a lease. The contract involves an identified asset (because the SunGen solar facility is explicitly specified in the contract and SPC has no substitution rights), and REG has the right to obtain substantially all of the economic benefits from use of the identified asset over the 10-year period of use. REG does not, however, have the right to control the use of the facility because it does not have the right to direct its use because (1) the decisions about how and for what purpose the plant will be used during the period of use are predetermined, (2) REG was not involved in the design (e.g., did not have input into the location and specifications of the facility that determine its output) and, (3) REG does not operate the facility.

SunGen, battery system

REG’s agreement to use the battery system does meet the definition of a lease. The contract involves an identified asset (because the SunGen battery system is explicitly specified in the contract and SPC has no substitution rights). Further, REG has the right to control the use of the battery system throughout the 10-year term:

- Economic benefits — REG has exclusive use of the battery through its contractual right to all the battery system’s storage capacity and thus has the right to obtain all of the economic benefits from the use of the battery system over the 10-year term of the agreement.

- Right to direct the use of the battery system — The relevant decisions about how and for what purpose the battery system is used include (1) the determination of when the battery is charged; (2) the determination of how the battery is charged (whether from the grid or the solar facility); and (3) when power is dispatched from the system. REG has the contractual right to make all of these decisions. Although SPC operates and maintains the battery storage system, these decisions are not relevant as they are following REG’s direction. Because SPC is prevented from using the battery system for another purpose, REG’s decision making ability, in effect, determines when and whether the storage capacity is used.

As a result, REG would conclude that it has a purchase agreement for the energy received from the facility and a lease of the storage facility.

EXAMPLE UP 2-10

Right to control – energy storage tolling arrangement

Rosemary Electric & Gas Company (REG) enters a contract to purchase all of the storage capacity from one of SunFlower Power’s standalone battery projects over a five-year term. SPC owns and operates five standalone battery systems in Iowa with grid connections. The contract specifies the battery system to be used to fulfill the contract with REG, including its unique specifications and location. Per the terms of the contract with SPC, REG can purchase power from the grid to charge the battery system during the term of the agreement. SPC is responsible for operating and maintaining the battery system to satisfy minimum technical requirements.

The contract authorizes REG to determine when the battery is charged and when any stored power is dispatched, subject to operational limitations and dispatch parameters. REG pays SPC a fixed monthly capacity charge and a variable payment associated with charging and dispatching power from the battery.

Which party has the right to control the use of the identified asset during the period of use?

Analysis

REG has the right to control the use of the identified battery system during the period of use. Although SPC operates and maintains the battery storage system, these are not rights to direct how and for what purpose the storage system is used, as discussed in

ASC 842-10-15-26.

REG decides when the battery system will be charged and discharged, thus determining how and for what purpose the battery system will be used. REG also has the right to obtain substantially all of the economic benefits from the battery system identified in the contract.

View image

View image