Introduction

In the fourth quarter of 2021, President Biden signed the

Infrastructure Investment and Jobs Act, which signals a long-term federal commitment to secure and modernize existing infrastructures, and support a transition to a clean economy. While that legislation is now law, at press time, the fate of the

Build Back Better reconciliation bill is still unknown. We summarize the current state, including proposed tax law changes that could impact 2021 financial statements.

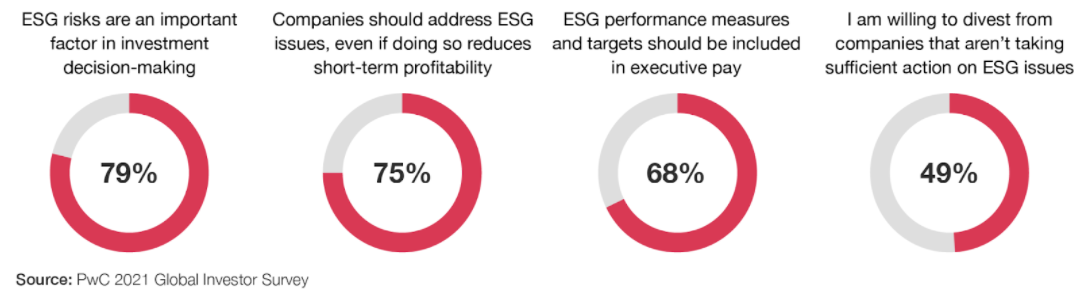

At the SEC, fourth quarter activity included announcing new PCAOB appointments and adopting rules requiring the use of universal proxy cards in contested board elections. The SEC staff also continues its focus on ESG, providing example comments registrants may receive related to their disclosures—or lack thereof—about climate change. We provide the details and other ESG updates, including key takeaways from our recent

ESG investor survey.

To help you prepare your year-end financial statements, we’ve compiled a list of

top five year-end reporting reminders. We also provide perspectives on the impacts of the current economic environment on your year-end reporting.

In standard-setting news, the FASB issued four new accounting standards, including changes to business combination accounting that companies may want to adopt this year. And, the feedback is in on the FASB’s future agenda. We reveal the topics that rose to the top of stakeholder’s lists.

In this edition of The quarter close, we highlight these and other relevant accounting and reporting topics you should consider as 2021 comes to a close.

Headlines - Fourth quarter 2021

Preparing for Build Back Better legislation

| |

The Build Back Better reconciliation bill was passed by the House in November, but at press time, the legislation continues to be debated within the Senate. As currently proposed, the bill’s spending provisions would largely be funded by:

|

- a new minimum tax on corporate profits,

- a 1% tax on corporate stock repurchases,

- international tax changes,

- increased taxes on high-income individuals, and

- increased IRS enforcement.

If the bill is signed into law before the end of the year, companies will be required to account for its tax impacts in 2021, the period of enactment. When tax reform was enacted shortly before year end in 2017, the SEC issued SAB 118, which permitted companies to record a reasonable estimate if they had not completed their accounting for tax reform. To date, the SEC has not indicated whether it would provide similar relief again; therefore, companies should be preparing now to account for the potential effects on their year-end financial statements.

Key accounting impacts

Many of the provisions within the bill would be effective for tax years beginning after December 31, 2022. However, the impact of enacted changes in tax law must be considered even if the effective date of those provisions is in a future period. For example, a number of provisions could impact valuation allowance assessments, such as additional limitations on the deductibility of interest, changes to the foreign tax credit regime, and modifications to the Base Erosion and Anti-Abuse Tax (BEAT), Foreign-Derived Intangible Income deduction (FDII), and Global Intangible Low-Tax Income (GILTI) inclusion.

Other key provisions of the Build Back Better bill include a new 15% minimum tax on adjusted financial statement income for large corporations and a country-by-country application of GILTI instead of the current worldwide aggregation model. Today, companies are permitted to make a policy election to either treat the impacts of GILTI as a period expense or consider the impacts in the measurement of deferred taxes. The proposed changes to GILTI have prompted discussions on whether the FASB will continue to allow the policy choice. Companies should stay tuned as additional guidance may be warranted in this area.

International developments

On the international front, the OECD continues to move forward with reforms to the international tax system, targeting 2023 for new guidelines to go into effect. As of October 2021, most of the member countries have signed on to the

two-pillar agreement, which has also been endorsed by the G-20.

Changes in leadership at the PCAOB

A new leadership team is now in place at the PCAOB with the

appointment of Erica Y. Williams as the new PCAOB chairperson and three new board members—Christina Ho, Kara M. Stein, and Anthony (Tony) C. Thompson. Duane DesParte will continue his service as a board member. While the PCAOB does not directly regulate companies, their policies and actions often have implications for all parties in the financial reporting ecosystem; therefore, companies may have an interest in tracking developments, including any announcements regarding the PCAOB’s future direction.

SEC adopts new rules for universal proxy cards and issues guidance on shareholder proxy proposals

[Today’s amendments] will put investors voting in person and by proxy on equal footing. This is an important aspect of shareholder democracy."

- Gary Gensler, SEC Chair, November 17, 2021

In November, the SEC

adopted final rules requiring parties in a contested director election to use universal proxy cards that include all director nominees presented for election at a shareholder meeting. The rule changes will give shareholders the ability to vote by proxy for their preferred combination of board candidates on a proxy card that would include all registrant and dissident nominees, similar to voting in person. The rules will apply to all non-exempt solicitations for contested elections other than those involving registered investment companies and business development companies. The new requirements will apply to any shareholder meetings involving contested director elections held after August 31, 2022.

In related news, the SEC staff issued a

new Staff Legal Bulletin (SLB No. 14L) outlining its views on the ordinary business exception and the economic relevance exception in Rule 14a-8 under the Securities Exchange Act of 1934. Rule 14a-8 details the process by which shareholders can present proposals for shareholders’ consideration in a company’s proxy statement. SLB No. 14L clarifies the standards the staff will apply when evaluating company requests for assurance that the staff will not recommend enforcement action if a shareholder proposal is omitted based on one of the exclusions outlined in Rule 14a-8 (“no-action relief”). Among other clarifications, the Staff Legal Bulletin indicates that the SEC staff will no longer focus on determining the nexus between a policy issue and the company, but will instead focus on the social policy significance of the issue that is the subject of the shareholder proposal.

SEC staff issues guidance on “spring-loaded” compensation awards

This quarter the SEC staff also released

Staff Accounting Bulletin No. 120, which provides the staff’s views on the accounting for share-based awards granted shortly before a release of material non-public information that is expected to result in a material increase in share price (commonly referred to as a spring-loaded award). In these situations, companies are expected to consider whether adjustments to the observable market price of the underlying share and estimates of expected volatility are necessary in order to determine the fair value of the awards. The guidance emphasizes the need for strong corporate governance and controls when granting awards, and details various disclosures that should be made when spring-loaded awards are granted. The guidance is effective immediately.

While the SEC continues to work on proposed climate disclosure rules for US public companies, the SEC’s Division of Corporation Finance

released example comments registrants may receive about their climate-related disclosures in the context of the existing disclosure framework. These examples include questions about the following, to the extent not currently addressed in disclosures:

- More expansive disclosure in the corporate social responsibility (CSR) report than provided in SEC filings

- Significant developments in legislation, regulation, and international accords regarding climate change

- Indirect consequences of climate-related regulation or business trends

- Physical effects of climate change on the company’s operations and results

Outside of the US, the IFRS Foundation

announced new actions on ESG, including a new International Sustainability Standards Board (ISSB), with the intent to consolidate leading investor-focused sustainability disclosure organizations into the ISSB by next summer. Meanwhile, the European Commission has proposed a directive intended to ensure adequate publicly available information about the risks that sustainability issues present for companies, which may impose disclosure requirements on European subsidiaries of US companies. Listen to our podcast,

Talking ESG: How new EU rules may impact your reporting, for more details.

Keep up with the latest on ESG by visiting our

ESG "hot topics" page, peruse our

Talking ESG podcast episodes, and watch replays of our

ESG accounting and reporting fall webcast series.

Inside scoop - Insights from the frontlines

Here are some of the technical accounting trends we’re seeing during the fourth quarter of 2021:

Year-end financial reporting reminders

We’ve compiled a top five list of year-end reporting reminders as you wrap up your 2021 reporting cycle.

- SEC modernization of Regulation S-K disclosure requirements

Amendments to Regulation S-K became effective in February 2021, which modernize, simplify, and enhance MD&A, streamline supplementary financial information, and eliminate the requirement to provide certain selected financial data. These changes impact many SEC filings, including 2021 Form 10-Ks for calendar year-end companies. For more details on the amendments, read our In depth, SEC amends MD&A and eliminates selected financial data.

- Income statement presentation

Recent SEC comments indicate a continued focus on compliance with the income statement presentation guidance in Rule 5-03 of Regulation S-X. For example, this guidance requires certain categories of revenue and cost of sales to be presented separately. SAB Topic 11B has further presentation requirements if cost of sales excludes depreciation and amortization. Companies should also consider disclosure of policies related to the presentation of costs in the income statement. Listen to our

Inventory and cost of sales: What’s trending in SEC comments podcast for more insights.

- Non-GAAP measures

Non-GAAP financial measures and their compliance with Item 10(e) of Regulation S-K and the related interpretations continues to be an area of frequent SEC comment, sometimes resulting in requests to remove or substantially modify non-GAAP metrics. Focus areas include reconciliation to the most comparable GAAP financial measure and the appropriateness of adjustments for items identified as non-recurring, infrequent, or unusual. Non-GAAP measures that are deemed misleading or a use of individually-tailored accounting principles are also not permitted. For more on this topic, listen to our podcast,

Non-GAAP financial measures: 5 things you need to know, and visit our

SEC Comment Letter trends: Non-GAAP measures page.

- Recently-issued accounting standards

Disclosures of the impact of accounting standards issued but not yet effective (SAB 74 disclosures) should consider recently-issued standards such as the new guidance on liabilities and equity (

ASU 2020-06). SAB 74 disclosures are generally expected to become more detailed in reporting periods closer to a standard’s adoption date. For a complete list of recently-issued accounting standards and effective dates, refer to our

Guidance effective for calendar year-end public companies page.

- Other disclosure reminders

In addition to

ESG, other areas where disclosure may be warranted include

LIBOR transition, cybersecurity risks and incidents, and impacts of COVID-19. Disclosures on these topics should continue to evolve based on company facts and circumstances.

Looking for more reminders by topical area? Check out our

podcast library, which includes our

Full disclosure series. Each episode covers financial statement presentation and disclosure requirements, from the top of the financials through the footnotes. Our new

What’s trending in SEC comments podcast series provides insights on areas of frequent SEC comment. Also visit our

SEC comment letter trends website, updated for observations through the third quarter.

Inflation, supply chain disruptions, and labor shortages: Potential financial reporting implications

Macroeconomic events often affect the financial statements—and this year is no exception. Although experts debate whether inflation is transitory or here for the long haul, it’s clear that certain costs are rising. In addition, supply chain disruptions are preventing some companies from sourcing raw materials to make their products while labor shortages may impact their ability to make, sell, and deliver their products, or at a minimum, drive increases in labor costs.

A company’s response to these macroeconomic events determines the impact, and in turn, the financial reporting implications. For example, has the company made other sourcing arrangements or been able to raise prices to offset the lost volume or rising costs? If the market will bear higher pricing, the impact of rising costs may be offset. If not, consider the impact to margins and how long those impacts may last.

A key consideration for public companies is the disclosure of these impacts within MD&A in their SEC filings. MD&A requires information that the company believes is necessary to explain its results, including known material events, trends, and uncertainties impacting the business.

One common disclosure that may be particularly relevant in the current environment is the relative impact of price and quantity on changes in revenue and margins. In addition, sourcing from new suppliers or shipping in new ways may make supply chain operations more complex and introduce new costs into the system, potentially reducing margins.

Lastly, companies significantly affected by these events should consider whether they should be disclosed as risk factors.

Other considerations include:

Non-GAAP measures: As with all non-GAAP financial measures, the identification of the adjustments that are attributable to any macroeconomic event or condition will require judgment to determine whether the amounts are truly attributable to the event, incremental to normal operations, actual not hypothetical, and quantifiable. Also, given the uncertainty in how long these conditions may last, it is important to consider the SEC requirement that an adjustment not be labeled as nonrecurring or infrequent if the measure excludes amounts related to an event that occurred in the last two years or is expected to occur again in the next two years.

Cash flow projections: Companies should revisit their assumptions in any areas of GAAP that rely on cash flow projections (e.g., impairments of long-lived assets and goodwill), interest rates (e.g., pension obligations), or future operating results more generally (e.g., realizability of deferred tax assets). Depending on the company’s facts and circumstances, the positive and negative cash flow impacts may offset in whole or in part, but it’s important to ensure assumptions being used reflect all current developments.

Revenue: Measures of progress for long-term contracts may need to be updated, for example due to supply chain delays or increased costs, and fixed price contracts should be reassessed for possible losses due to changes in costs.

Inventory: The net realizable value of inventory may be impacted if a company is committed to a source of supply but increased costs cannot be passed on to customers.

Hedging: To lock in costs, companies that seek to hedge purchases, sales, or future interest payments will need to ensure they have met the eligibility, effectiveness, and other documentation requirements, especially if they are new to hedge accounting. Those already using hedge accounting will need to consider whether forecasted purchases/sales or forecasted interest receipts/payments remain probable of occurring. This could impact eligibility for current and future hedges.

Debt: Changes in financial ratios may impact existing debt covenants that require certain ratios. Breaches of debt covenants may make debt puttable on demand, which could cause long-term debt to be classified as current.

Ask the National Office - Perspectives from our professionals

Equity method investments: a refresher on basis differences

| |

Jonathan Rhine

Director, PwC National Office

|

What should be top of mind at year end for equity method investments?

Jonathan: The first thing that comes to mind is Rule 3-09 of Regulation S-X. It requires registrants to present separate audited financial statements for equity method investments when certain significance tests are met. Those financial statements would need to include comparative periods even if the significance test is not met in those periods. At a lower significance level, disclosures may still be required under Rule 4-08g of Regulation S-X, either for individual investees or all investees in the aggregate.

So getting the significance test right is critical to determining the year-end reporting requirements. To do so, you will want to ensure you have included equity method earnings and the basis adjustments when calculating the income test. We frequently receive questions about that.

To level set, what are basis differences?

Jonathan: An investor’s initial carrying amount of an equity method investment reflects its cost to acquire the investment. An investee, however, carries the underlying assets and liabilities based on its historical application of GAAP.

Upon acquisition, an investor determines its cost basis in the individual assets and liabilities of an equity-method investee, including those not recorded in the investee’s books (e.g., unrecognized intangible assets). This is similar to how the acquisition method is applied in a business combination.The difference between the cost basis of the investment, and the investor’s share of the net assets in the investee’s books is commonly referred to as a basis difference. Basis differences are generally attributable to multiple assets and liabilities of the investee and are reflected in memo accounts of the investor.

What are some of the implications of basis differences?

Jonathan: Basis differences attributed to tangible and finite-lived intangible assets are depreciated or amortized as an adjustment to equity method earnings. On the other hand, differences attributed to goodwill or other indefinite- lived intangibles are not amortized.

If an investee disposes of an asset for which the investor has a basis difference, the investor should write off the basis difference as an adjustment to equity method earnings.

Impairments have also been a recent area of focus. What happens if an investee impairs an asset?

Jonathan: If an investee impairs its long-lived assets and the investor has a positive basis difference attributable to those assets, the investor would recognize an incremental impairment charge as an adjustment to equity method earnings.

Are there any other events that could create basis differences after the acquisition date?

Jonathan: Yes. An investor is required to impair an equity method investment when the decline in the value of the equity method investment below its carrying amount is other than temporary. An investor is required to attribute this impairment charge to the underlying equity method memo accounts of its investment. The attribution may create new basis differences or impact existing basis differences.

In transition - Practical reminders for new standards

Here are updates and insights on recently-issued standards as you prepare to adopt the new guidance:

FASB issues final guidance on acquired revenue contracts - early adoption permitted

The amendments in

ASU 2021-08 provide an exception to fair value measurement for contract assets and contract liabilities (i.e., deferred revenue) acquired in a business combination. Instead, they will be recognized and measured by the acquirer in accordance with

ASC 606,

Revenue from Contracts with Customers. Generally, this new guidance will result in the acquirer recognizing contract assets and contract liabilities at the same amounts recorded by the acquiree. This change is intended to improve consistency in revenue recognition in the post-acquisition period for acquired contracts as compared to contracts entered into after the business combination.

The standard is effective for public business entities in January 2023; all other entities have an additional year to adopt. Early adoption is permitted; however, if the new guidance is adopted in an interim period, it is required to be applied retrospectively to all business combinations within the year of adoption. For more details, read our In depth, Accounting for acquired contract assets and contract liabilities.

New disclosures about government assistance required beginning in 2022

ASU 2021-10 requires new disclosures about transactions with a government that are accounted for by applying a grant or contribution model by analogy, such as IFRS guidance on government grants in IAS 20 or the guidance on contributions for not-for-profit entities in

ASC 958-605. This could include various forms of government assistance (e.g., grants or other incentives), but excludes transactions in the scope of specific US GAAP, such as tax incentives accounted for under

ASC 740,

Income Taxes. Companies are required to provide information about the nature of the transaction, including significant terms and conditions, as well as the company’s accounting policy and the specific financial statement line items affected. The new guidance is effective for annual reporting periods beginning after December 15, 2021.

New standards provide expedients for nonpublic entities

Two new standards were issued in the fourth quarter that apply only to nonpublic entities:

- ASU 2021-07, a consensus of the Private Company Council, provides a practical expedient for nonpublic entities to determine the current price input of equity-classified share-based awards using a reasonable valuation method, such as one performed in accordance with Treasury Regulations US IRC Section 409A. The new guidance is effective for fiscal years beginning after December 15, 2021 and interim periods within the following fiscal year. Early adoption is permitted.

- ASU 2021-09 amends the leases guidance to allow lessees that are not public business entities to elect to use a risk-free rate as the discount rate by class of underlying asset, rather than at the entity-wide level. Entities will apply the new guidance when they adopt the leases standard (ASC 842), or if ASC 842 has already been adopted, the guidance is effective for fiscal years beginning after December 15, 2021 and interim periods within the following fiscal year. Early adoption is permitted.

On the horizon - Standard-setting developments

Here are standard-setting developments you need to know about as we make our way through 2021:

What’s next for standard setting: feedback is in on the FASB’s and IASB’s future agendas

The window for public comment on the FASB’s

invitation to comment on its future standard-setting agenda came to a close in September. A common theme from respondents was encouraging the FASB to address emerging areas even before they become pervasive issues. In particular, four topics stood out:

Internally-developed intangible assets

Costs related to internally-developed intangible assets are generally expensed as incurred, creating challenges when comparing companies that grow organically with those that grow through acquisitions. Respondents supported either reassessing the accounting model for intangible assets or considering additional disclosure.

| |

ESG-related transactions

Companies making ESG commitments, such as “net zero” pledges, often purchase offsets or credits to accomplish these goals. Given the lack of guidance in this area, respondents encouraged the FASB to address the accounting for these and other ESG-related transactions as they begin to become more prevalent.

|

|

Digital assets

Now that cryptocurrencies and similar assets are becoming more mainstream, the accounting for these assets is increasingly relevant. Respondents supported standard setting in this area as the current US GAAP guidance is not designed for intangible assets with an active market.

| |

Government grants

Government assistance programs are becoming more common, whether related to the COVID-19 pandemic or other government initiatives. As there is no guidance in US GAAP for grants issued to for-profit entities, most companies look to IFRS guidance by analogy. Respondents supported closing this gap.

|

Stakeholders responding to the

IASB’s request related to its agenda touched on many of the same themes, showing support for standard setting on intangibles, digital assets, and ESG. See the

IASB staff’s summary for more details.

Project spotlight: EITF adds project on investments in tax credit structures

In the fourth quarter, the EITF picked-up a new

project in response to the increasing number of investments in tax credit structures. The EITF will consider whether to expand the use of the proportional amortization method of accounting--currently allowed only for investments in the low-income housing tax credit--to other programs, such as the New Markets Tax Credit and Renewable Energy Tax Credit. The proportional amortization method results in the tax credit investment being amortized in proportion to the allocation of tax credits in each period, and also allows the investment amortization and tax credits to be presented on a net basis within the income tax line item. Impacted companies should stay tuned as the EITF discusses this issue further in 2022.

Looking for a complete list of active standard-setting projects? Refer to the FASB’s

Technical Agenda.

PwC Reference library

PwC’s accounting podcasts

PwC's accounting podcast series includes a library of podcasts covering today’s most compelling accounting, reporting, and business issues. Subscribe to our podcast feed on your platform of choice.

In our Talking ESG podcast series, we give an end-to-end look at what it takes to build effective ESG reporting in today’s environment. From investor to stakeholder expectations, from global frameworks to data, process, and controls—there’s something in it for everyone.

Some of the most popular podcasts from this quarter:

Accounting and reporting webcasts

Some of our other recent webcasts:

ESG accounting and reporting fall webcast series

ESG: What finance teams need to know (CPE-eligible webcast replay)

Lease accounting - Springing forward (CPE-eligible webcast replay)

Rebuilding revenue - Accounting and reporting trends in revenue (CPE-eligible webcast replay)

In depth

Infrastructure legislation: Clean power provisions

Accounting and disclosure implications of natural disasters

Accounting for acquired contract assets and contract liabilities

In brief

In the loop

Making sense of ESG

Governance insights

Subscribe to our weekly accounting newsletter

Interested in staying current on newly released PwC accounting, financial reporting, and business content, in addition to highlights from regulators and standard setters?

Subscribe to PwC's weekly accounting newsletter and have our newsletter delivered to your inbox every Friday.