Search within this section

Select a section below and enter your search term, or to search all click ASU 2018-09—Codification improvements

Favorited Content

Copyright © 2018 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government. |

Issue No. |

Codification Topic |

Subtopic |

Effective Date |

2 |

Earnings Per Share |

260-10 |

N/A |

5 |

Debt |

470-50 |

N/A 1

|

10 |

Income Taxes |

740-30 |

N/A 1

|

13 |

Derivatives and Hedging |

815-15 |

N/A |

15 |

Fair Value Measurement |

820-10 |

N/A |

17 |

Fair Value Measurement |

820-10 |

N/A |

18 |

Fair Value Measurement |

820-10 |

N/A |

20 |

Fair Value Measurement |

820-10 |

N/A |

21 |

Foreign Currency Matters |

830-10 |

N/A

|

23 |

Financial Services— Depository and Lending |

942-505 |

N/A |

24 |

Financial Services— Insurance |

944-30 |

N/A |

27 |

Not-for-Profit Entities |

958-325 |

N/A 1

|

28 |

Not-for-Profit Entities |

958-720 |

N/A |

29 |

Plan Accounting—Defined Contribution Pension Plans |

962-360 |

N/A |

Type of Transition |

||||||

Issue No. |

Codification Topic |

Subtopic |

Modified Retrospective |

Prospective |

Other |

Effective Date |

1 |

Income Statement—Reporting Comprehensive Income |

220-10 |

X |

Public Business Entities (PBE): 12/15/18 Others: 12/15/19 |

||

3 |

Investments—Debt and Equity Securities |

320-10 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

4 |

Debt |

470-50 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

6 |

Distinguishing Liabilities from Equity |

480-10 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

7 |

Compensation—Stock Compensation |

718-740 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

8 |

Other Expenses |

720-35 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

9 |

Income Taxes |

740-10 |

X |

PBE: 12/15/17 Others: 12/15/182 |

||

11 |

Business Combinations |

805-740 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

12 |

Derivatives and Hedging |

815-10 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

14 |

Fair Value Measurement |

820-10 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

16 |

Fair Value Measurement |

820-10 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

19 |

Fair Value Measurement |

820-10 |

X |

PBE: 12/15/17 Others: 12/15/18 (early adoption permitted as of 12/15/17)2 |

||

22 |

Financial Services—Brokers and Dealers |

940-405 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

25 |

Financial Services—Insurance |

944-310 |

X |

PBE: 12/15/17 Others: 12/15/18 (early adoption permitted as of 12/15/17)2 |

||

26 |

Financial Services—Insurance |

944-360 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

30 |

Plan Accounting—Defined Contribution Pension Plans |

962-325 |

X |

PBE: 12/15/18 Others: 12/15/19 |

||

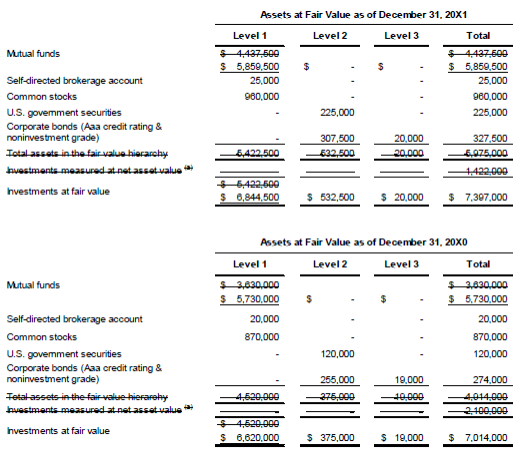

Level 1 |

Inputs to the valuation methodology are quoted prices (unadjusted) in active markets for identical assets or liabilities that the Plan can access at the measurement date. |

Level 2 |

Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly, such as:

If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability.

|

Level 3 |

Inputs that are unobservable inputs for the asset or liability |

Paragraph |

Action |

Accounting Standards Update |

Date |

FinancialStatements Are Available to Be Issued |

Added |

2018-09 |

07/16/2018 |

105-10-65-4 |

Added |

2018-09 |

07/16/2018 |

105-10-65-5 |

Added |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

220-10-45-10B |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

260-10-45-60B |

Amended |

2018-09 |

07/16/2018 |

260-10-55-62 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

320-10-50-1A |

Amended |

2018-09 |

07/16/2018 |

320-10-50-13 |

Superseded |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standard Update |

Date |

470-50-40-2A |

Added |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

480-10-55-55 |

Amended |

2018-09 |

07/16/2018 |

480-10-55-59 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

718-740-35-2 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

720-35-15-2 |

Amended |

2018-09 |

07/16/2018 |

720-35-15-5 |

Superseded |

2018-09 |

07/16/2018 |

720-35-25-1 |

Amended |

2018-09 |

07/16/2018 |

720-35-25-1A |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

740-10-25-53 |

Amended |

2018-09 |

07/16/2018 |

740-10-25-55 |

Superseded |

2018-09 |

07/16/2018 |

740-10-55-168 |

Amended |

2018-09 |

07/16/2018 |

740-10-55-203 |

Amended |

2018-09 |

07/16/2018 |

740-10-65-7 |

Added |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standard Update |

Date |

805-740-25-13 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-10-45-4 |

Superseded |

2018-09 |

07/16/2018 |

815-10-45-5 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-15-25-1 |

Amended |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

820-10-35-16D |

Amended |

2018-09 |

07/16/2018 |

820-10-35-18D through 35-18F |

Amended |

2018-09 |

07/16/2018 |

820-10-35-18H through 35-18L |

Amended |

2018-09 |

07/16/2018 |

820-10-35-24B |

Amended |

2018-09 |

07/16/2018 |

820-10-50-2 |

Amended |

2018-09 |

07/16/2018 |

820-10-50-2E |

Amended |

2018-09 |

07/16/2018 |

820-10-55-11 |

Amended |

2018-09 |

07/16/2018 |

820-10-55-33 |

Amended |

2018-09 |

07/16/2018 |

820-10-55-34 |

Amended |

2018-09 |

07/16/2018 |

820-10-55-100 |

Amended |

2018-09 |

07/16/2018 |

820-10-65-9 |

Superseded |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

825-10-65-4 |

Added |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

940-210-05-1 |

Added |

2018-09 |

07/16/2018 |

940-210-15-1 |

Added |

2018-09 |

07/16/2018 |

940-210-45-1 |

Added |

2018-09 |

07/16/2018 |

Paragraph |

Action |

Accounting Standards Update |

Date |

940-405-55-1 |

Superseded |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

942-210-45-3 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

942-505-50-1 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

944-30-25-1A |

Amended |

2018-09 |

07/16/2018 |

944-30-25-1DD |

Added |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

944-310-45-1 |

Amended |

2018-09 |

07/16/2018 |

944-310-45-2 |

Amended |

2018-09 |

07/16/2018 |

944-310-50-1 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

944-360-35-1 |

Amended |

2018-09 |

07/16/2018 |

944-360-45-3 |

Amended |

2018-09 |

07/16/2018 |

944-360-45-4 |

Amended |

2018-09 |

07/16/2018 |

944-360-50-1 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

958-720-45-15 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

962-205-45-5 |

Superseded |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

962-325-55-17 |

Amended |

2018-09 |

07/16/2018 |

Paragraph

|

Action

|

Accounting Standards Update |

Date

|

Defined Contribution Plan |

Added |

2018-09 |

07/16/2018 |

962-360-05-1 |

Added |

2018-09 |

07/16/2018 |

962-360-15-1 |

Added |

2018-09 |

07/16/2018 |

962-360-35-1 |

Added |

2018-09 |

07/16/2018 |

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

Select a section below and enter your search term, or to search all click ASU 2018-09—Codification improvements