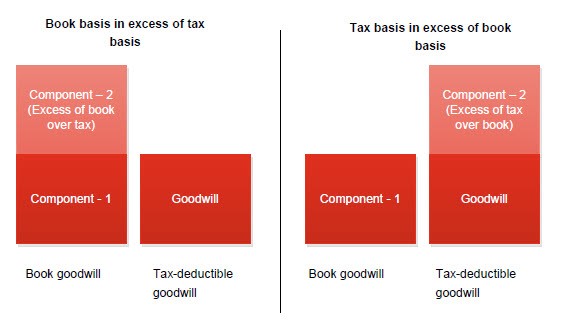

In many jurisdictions, tax goodwill is associated with the stock of a specific legal entity, whereas for book purposes, goodwill is associated with a reporting unit. The reporting unit may include several legal entities or be limited to a portion of a legal entity. This can result in differences between the book and tax accounting for goodwill upon the disposal of a business.

If the disposed business is a legal entity, any tax-deductible goodwill associated with that entity would be included in the determination of the taxable gain or loss. If the disposed operations are a business,

ASC 350-20-40-3 requires the allocation of a reporting unit’s goodwill to (1) the business that was disposed of and (2) the remaining parts of the reporting unit, based on their relative fair values on the date of disposal. Once goodwill is characterized as component-1 or component-2, it retains this characterization as long as a reporting entity retains that goodwill. Therefore, upon disposal of a business that includes some or all of a reporting entity’s goodwill, a deferred tax adjustment would generally be required for disposal of component-1, but not for disposal of component-2 goodwill. Example TX 10-19 and Example TX 10-20 illustrate the disposal of a business, including a portion of component-1 goodwill, resulting in a deferred tax adjustment to the reporting entity.

Example TX 10-21 illustrates the disposal of a business, including a portion of component-2 goodwill, resulting in no deferred tax adjustment to the reporting entity.

EXAMPLE TX 10-19

Disposal of tax-deductible goodwill with retention of book goodwill

Entity A acquired Entity B in a taxable business combination (i.e., Entity A treated the purchase as an asset acquisition for tax purposes), which gave rise to book and tax-deductible goodwill in equal amounts of $100. The business of Entity B and the associated goodwill are fully integrated into one of Entity A’s reporting units.

In a later period, Entity A decides to dispose of the shares of Entity B, including Entity B’s operations. For tax purposes, the entire remaining tax-deductible goodwill of $70 ($100 initial basis less assumed tax amortization of $30) is included in the disposal. For book purposes, assume goodwill of $20 should be allocated to the disposed operation on a relative fair value basis. As a result, $80 of the book goodwill is retained by the surviving reporting unit within Entity A ($100 initial value less $20 included in the disposed operation).

What is the deferred tax effect of a disposal of tax-deductible goodwill with a retention of book goodwill?

Analysis

The disposal would result in a basis difference in the goodwill retained by Entity A, with book goodwill exceeding tax-deductible goodwill by $80. This would give rise to a deferred tax liability for the entire $80 taxable basis difference (i.e., Entity A would compare nil tax-deductible goodwill to book goodwill of $80) because book goodwill remains component-1 goodwill consistent with the initial determination made at the acquisition date.

EXAMPLE TX 10-20

Disposal of book goodwill with retention of tax-deductible goodwill

Entity A acquired Entity B in a taxable business combination (i.e., Entity A treated the purchase as an asset acquisition for tax purposes), which gave rise to book and tax-deductible goodwill in equal amounts of $100. The business of Entity B and the associated goodwill are fully integrated into one of Entity A’s reporting units.

In a later period, Entity A decides to dispose of a significant portion of its operations but not its shares in Entity B. For tax purposes, there is $70 of tax-deductible goodwill remaining ($100 initial basis less assumed tax amortization of $30). The tax-deductible goodwill associated with the shares of Entity B would remain with Entity A. For book purposes, assume $80 of goodwill is allocated to the disposed operations on a relative fair value basis and included in the determination of the disposal gain or loss. Book goodwill of $20 remains in the reporting unit.

What is the deferred tax effect of a disposal of book goodwill with a retention of tax-deductible goodwill?

Analysis

The disposal of component-1 goodwill will result in a basis difference in goodwill retained by Entity A, consisting of the remaining tax goodwill ($70) exceeding book goodwill ($20) by $50, which will give rise to a deferred tax asset (subject to the measurement criteria of

ASC 740). This is a result of book goodwill remaining component-1 goodwill consistent with the initial determination made at the acquisition date.

EXAMPLE TX 10-21

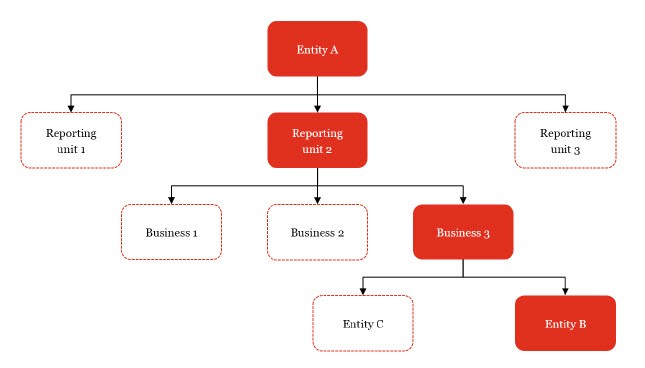

Evaluating deferred tax assets for temporary differences on component-2 goodwill after disposition of the entity that generated the goodwill

Entity A acquired Entity B in a nontaxable business combination. For tax purposes, the transaction resulted in a carryover basis in Entity B’s assets and liabilities. Because the tax basis carried over and Entity B’s assets for tax purposes did not contain any tax-deductible goodwill, all of the goodwill recorded in acquisition accounting ($500) was component-2 book goodwill (as defined in

ASC 805-740-25-9).

Entity A has three reporting units. Entity A’s reporting unit composition is as follows:

The component-2 goodwill from the acquisition of Entity B was all allocated to Reporting Unit 2.

In the current year, Entity A sold Business 3, which includes Entity B. The goodwill in Reporting Unit 2 was allocated to Business 3, based on the relative fair value of Business 3 and the retained operations of Reporting Unit 2, pursuant to

ASC 350-20-40-3. This resulted in only $100 of book goodwill being allocated to the business sold (Business 3).

Should Entity A record a deferred tax liability on the book to tax difference of $400 associated with the remaining book goodwill of Entity B in Reporting Unit 2 subsequent to the sale of Entity B?

Analysis

No deferred tax liability should be recognized in this instance. On the date Entity A acquired Entity B, the entire amount of book goodwill would have been classified as component-2 goodwill as there was no tax goodwill in the transaction, and no deferred tax liability was recorded pursuant to

ASC 740-10-25-3(d). The fact that only a portion of that goodwill was subsequently attributed to Entity B when it was disposed of does not change that component-2 characterization. Thus, the goodwill remaining in Reporting Unit 2 after the sale of Entity B would continue to be component-2 goodwill, for which no deferred tax liability would be recorded.