As discussed at

NP 9.3, NFPs (other than NFP HCOs) can elect fair value measurement of investments in a portfolio held for the objective of earning investment return (current income, capital appreciation, or both). This election is referred to as the portfolio-wide fair value option, or PWFVO. In our view, the PWFVO’s scope is limited to investments entered into for purposes of earning investment return; it should not be applied to investments made for purposes of carrying out the NFP’s operating mission.

When this approach is taken, the spectrum of accounting approaches for equity interests in Figure NP 9-3 (in

NP 9.5) is largely disregarded, and the model is highly simplified.

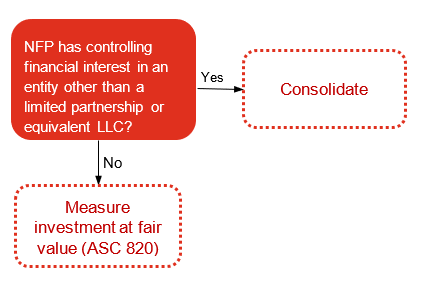

Figure NP 9-4 illustrates the accounting for equity interests in portfolios for which the PWFVO has been elected.

Figure NP 9-4

Decision tree—accounting for equity interests under the portfolio-wide fair value option

For equity interests in the form of shares of common stock, an NFP must evaluate whether consolidation is required (see

NP 9.7.1). If not, fair value measurement can be used. For equity interests in limited partnerships, fair value measurement is used regardless of the level of ownership or extent of control. For equity interests in limited liability companies, the ability to use fair value measurement depends on whether the LLC is the functional equivalent of a corporation or is more like a limited partnership, as discussed in

NP 9.9.1.

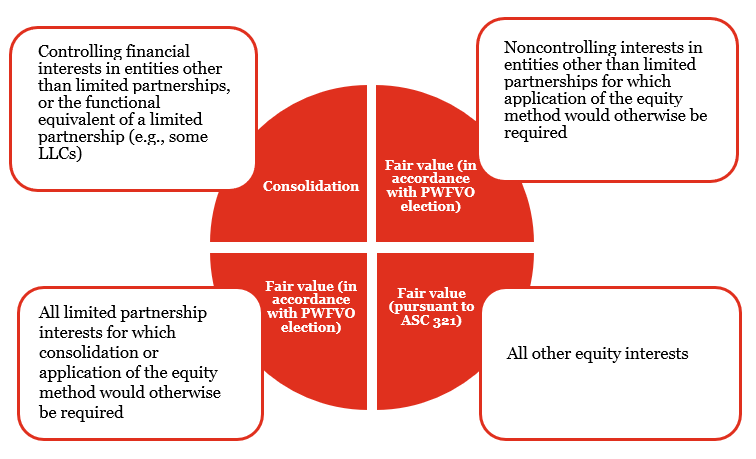

Figure NP 9-5 depicts the measurement of various equity interests within a portfolio subject to a PWFVO election.

Figure NP 9-5

Measurement approaches for investments in a portfolio subject to a PWFVO election

View image

View image

Equity interests measured at fair value under the PWFVO are generally reported at fair value on a recurring basis. Fair value is determined in accordance

ASC 820. However, for investments in funds that have the characteristics of an investment company (as specified in

ASC 946, such as hedge funds, private equity funds, and the like), the fair value of the investment can be measured by reference to the net asset value (NAV) reported by the investee, as long as certain disclosures regarding the investment’s nature and risk are provided by the investor. This “NAV practical expedient,” which is an accounting policy election, is described in

ASC 820-10-35-59.

FV 6.2.6 discusses the NAV practical expedient and the circumstances in which it can be elected.

ASC 321 provides a measurement alternative for equity investments within its scope that do not have readily determinable fair values and do not qualify for the NAV practical expedient. For those investments, if the measurement alternative is elected, an entity will measure the investment at cost, less any impairment, adjusted for changes (increases or decreases) in value based on observable transactions in an orderly market for the identical or a similar investment of the same issuer. For additional information on the measurement alternative, see

NP 9.7.3.

Example NP 9-1 illustrates the analysis for an NFP that wishes to use the

ASC 321 measurement alternative for qualifying investments within the portfolio.

EXAMPLE NP 9-1Using the

ASC 321 measurement alternative for an investment in a portfolio for which PWFVO has been elected

University has an endowment portfolio for which the

ASC 958-810 portfolio-wide fair value option has been elected. All of the portfolio’s investments are measured at fair value except for those that require consolidation (i.e., investments of common stock or functionally-equivalent LLC interests that represent a controlling financial interest). University wants to use the measurement alternative in

ASC 321 for qualifying investments.

University acquires the following investments for the portfolio:

- Common stock representing a 10% interest in the investee

- A general partner interest in a limited partnership in which no substantive rights are granted to the limited partners

- A limited partner interest in a real estate partnership that provides substantive kick-out rights, but the University holds less than a majority of the limited partner interests that have substantive kick-out rights

- A limited partner interest in a non-real estate partnership which provides no substantive rights to limited partners

For which of these investments can University consider using the measurement alternative in

ASC 321?

Analysis

The measurement alternative is only available for qualifying investments that are within the scope of

ASC 321 (see

NP 9.6). Even though University has elected the PWFVO, the analysis of whether the measurement alternative in

ASC 321 can be applied depends on the nature of the individual investment. University’s analysis of these four investments would likely conclude as follows.

- 10% common stock holding. Based on the guidance discussed in NP 9.5, neither consolidation nor application of the equity method would be required for this investment; thus, it is within the scope of ASC 321. If the stock meets the ASC 321 criteria for using the measurement alternative described in LI 2.3.2 (i.e., it does not have a readily-determinable fair value; it does not qualify for use of the NAV practical expedient; and the fair value option under ASC 825 was not elected), University would be permitted to measure this investment using the measurement alternative.

- General partner interest in limited partnership. Outside of the PWFVO, consolidation of a general partner interest would be required based on the guidance in ASC 958-810. Because the use of fair value measurement is based on the PWFVO in ASC 958-810 (and not ASC 321), we do not believe the measurement alternative would be available, consistent with our views on interests for which fair value measurement has been elected under the ASC 825-10 fair value option (see LI 2.3.2).

- Limited partner interest in real estate partnership. Outside of the PWFVO, this investment would be within the scope of ASC 321 neither consolidation nor equity method accounting is required, analyzed as follows:

- Although the limited partners hold substantive kick-out rights, the University does not own a majority of the limited partnership interests and therefore this interest would be noncontrolling (and thus, not require consolidation).

- To determine whether the equity method would otherwise apply, the key determination is whether the interest would be viewed as “more than minor” or “minor” under the requirements of ASC 958-810-15-4(d), which is discussed in NP 9.8.3. Judgment should be applied based on the specific facts and circumstances of the investment. If the interest is “more than minor,” application of the equity method would have otherwise been required. In that case, because the use of fair value measurement is based on the PWFVO election inASC 958-810, we do not believe the measurement alternative would be available. If the interest is “minor,” on the other hand, the investment would fall within the scope of ASC 321, and the measurement alternative would be available.

- Limited partner interest in non-real estate partnership. Outside of the PWFVO, this investment would be within the scope of ASC 321 if neither consolidation nor equity method accounting is required, analyzed as follows:

- Because University has no substantive kick-out rights in the partnership, its interest is noncontrolling (and thus, not require consolidation).

- Under the guidance for noncontrolling interests in limited partnerships other than real estate partnerships, the interest would be within the scope of ASC 321 and, therefore, eligible for use of the measurement alternative. For further information about the evaluation of this type of investment outside of the PWFVO, see NP 9.8.3.1.

Question NP 9-1 addresses whether NFPs need to segregate equity interests measured at fair value based on

ASC 321 from those for which fair value measurement is based on the PWFVO.

Question NP 9-1University A holds equity interests in its portfolio that are not required to be consolidated and has elected the PWFVO. For accounting purposes, must University A distinguish the equity interests in the portfolio that are within the scope of

ASC 321 from those that are not?

PwC response

From a practical perspective, the answer is no, unless University A wishes to apply the measurement alternative in

ASC 321. This is because the measurement alternative is not available for investments that are outside the scope of

ASC 321 (i.e., equity interests that would otherwise need to be consolidated or reported using the equity method if they were outside the portfolio subject to the PWFVO election). Under both

ASC 321 and the PWFVO in

ASC 958-810, investments are measured at fair value on a recurring basis in accordance with

ASC 820 and are subject to the same disclosure requirements.